Quick answer: When a senior executive cuts in with “what’s your recommendation?” and you were briefed only to present options, do not invent one and do not apologise for not having one. Use a four-part response: acknowledge the question directly, name the decision criteria you would use, indicate the option that scores highest against those criteria as a working view, and offer the timeframe in which you can return with a fully-formed recommendation. This holds authority without inventing certainty you do not have, and gives the executive committee something concrete to work with in the room.

Jump to

Saoirse Blackwood runs corporate strategy at a UK-listed industrial group. Last autumn she presented three market-entry options to the executive committee — Germany, Poland, the Netherlands — comparing cost, timeline, regulatory complexity, and commercial yield. Her brief from the CEO had been explicit: present the options, walk through the trade-offs, do not pre-empt the committee’s decision. Three slides per option. A clean comparison matrix. No recommendation slide.

She got through option one. She got through option two. As she opened option three, the CEO leaned forward and cut across her: “Saoirse, yes, but what’s YOUR recommendation?” She froze. The brief had told her not to recommend. The CEO was now asking her to. She heard herself say, “I, ah, I think — well, the brief was to present the options, so I haven’t formally —” and watched the CFO’s face shift. The room cooled. She recovered in the second half of Q&A, but the hesitation cost her credibility she spent the next two committee cycles rebuilding.

The lesson Saoirse took from that meeting was not “always have a recommendation ready.” It was that the question is not really about the recommendation — it is about whether you can hold authority when the brief and the room have diverged. There is a structured response that works in this exact situation.

The structured framework for handling hard executive Q&A — including the “what’s your recommendation?” trap.

The Executive Q&A Handling System is the self-paced framework for senior professionals who need to answer tough committee questions with calm authority and decision-safe responses, in 45 seconds or less. Self-study, instant access. Built around the structured patterns presenters use to recover from exactly this kind of mid-presentation pivot.

Why this question is the one senior leaders dread

“What’s your recommendation?” is not a hostile question. From the executive’s seat, it is the most natural question in the world: you have spent twenty minutes presenting analysis, you have clearly thought about it more than anyone else in the room, and the committee’s job is to make decisions. Asking for your view is efficient.

What makes it dreaded is the gap between brief and room. Your brief — often from the same CEO who is now asking — was to present options, not lead the committee toward a conclusion. So you arrive with a balanced presentation, and partway through the same person who briefed you for balance asks for the unbalanced view. The question collides with the instruction. The presenter is left holding both, and the room watches to see which way they fall. The question almost always comes from the most senior person present, often mid-flow. The freeze is rational — the cognitive load of reconciling brief, audience, and personal credibility in three seconds is genuinely high. It is also recoverable, with structure.

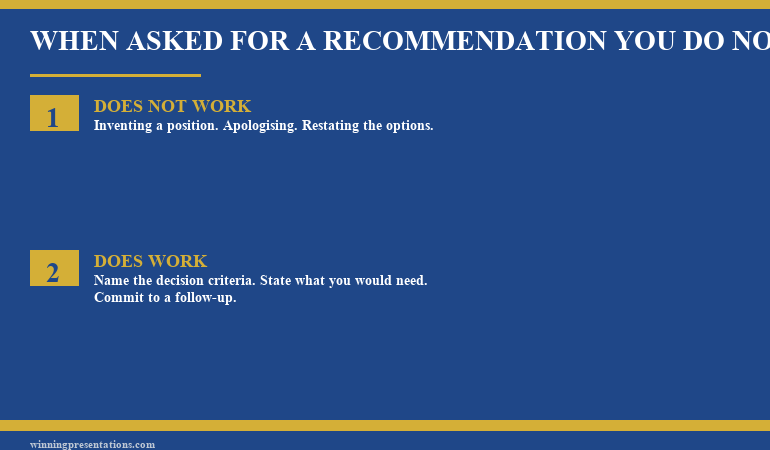

The two traps: inventing and indecision

Two responses to the executive recommendation question consistently damage credibility, and both feel reasonable in the moment.

The first trap is inventing a recommendation. Under pressure, the presenter blurts a preference — usually the option they personally find most interesting, or the one the CEO seemed to lean toward in an earlier conversation. The recommendation is not grounded in the analysis the committee just heard, because that analysis was structured for comparison, not for a single conclusion. Senior listeners notice immediately. The CFO probes a number the presenter has not stress-tested. The COO surfaces an operational risk the presenter has not weighed. Within ninety seconds, the invented recommendation is being dismantled. The presenter is now defending a view they invented under pressure, with material prepared for a different argument. This is the worst place a senior presenter can be.

The second trap is the appearance of indecision. The presenter, knowing the recommendation is not yet rigorous, retreats into deferral language. “Well, that’s really for the committee to decide.” “I’d want to do more analysis before I committed.” “There are arguments both ways.” Each individual sentence is defensible. The cumulative effect is fatal. The committee does not hear humility. They hear a senior person who has spent twenty minutes on this material and still cannot tell them what they think. The judgement that follows is rarely about the analysis — it is about whether this presenter is ready for the next level of responsibility.

Both traps come from the same source: trying to answer the question as asked, when the question itself is the wrong frame. The structured response reframes it into one you can answer with authority — without faking certainty and without appearing unable to form a view.

The four-part response that holds authority

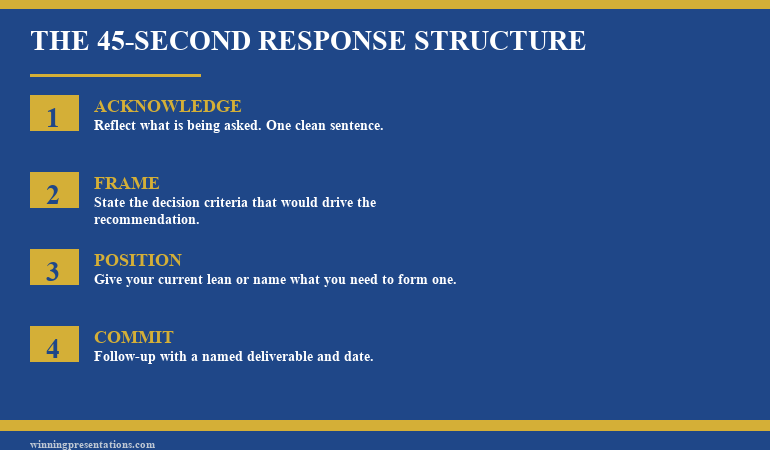

The structured response has four parts. Each part takes ten to fifteen seconds. The whole answer fits inside forty-five to sixty seconds, which is the upper limit of executive attention for a single Q&A response.

Part one: acknowledge directly. One sentence, no apology. “That is the right question to ask, and I want to give you a useful answer rather than a polished one.” This validates the executive’s intervention, signals you are about to answer rather than deflect, and telegraphs the kind of answer that is coming — substantive rather than rehearsed. The room is now expecting candour, not certainty.

Part two: name the decision criteria. “If I were to make a recommendation today, the criteria I would weight most heavily are X, Y, and Z.” Three criteria, no more. This is the single most credibility-protective move in the response. By naming the criteria explicitly, you demonstrate that you have thought about the decision structurally, even if you have not landed on a single answer. The committee sees your reasoning architecture. Senior listeners are far more reassured by a presenter who can articulate the framework than by one who states a conclusion without one.

Part three: state a working view. “On those criteria, the option that scores highest is option two — the Polish market entry — primarily because of the regulatory tailwind in 2027 and the lower capital requirement in year one. That is a working view, not a final recommendation, because I have not yet stress-tested the operational ramp-up assumptions with the regional team.” You are giving them a view. The view is bounded — you have specified what makes it provisional — but it is a view. The committee has something concrete to work with, and you have not invented a position you cannot defend.

Part four: offer a timeframe. “I can return to the committee within ten working days with a formal recommendation that includes the operational stress-test.” A specific date, scope, and deliverable. This closes the loop and re-establishes you as the person driving the decision. It also gives the committee a productive next step, which is what executive committees prefer over open questions.

The four parts work together. Acknowledgement lowers the temperature. Criteria demonstrate structure. Working view shows judgement. Timeframe restores ownership. The broader patterns for handling tough questions sit on the same structural foundation.

The complete framework for handling hard executive Q&A under pressure

The Executive Q&A Handling System is the self-paced framework for senior professionals who need to answer tough committee questions with calm authority and decision-safe responses in 45 seconds — including the recommendation question, the credibility challenge, the hostile probe, and the question you genuinely do not yet have a full answer to. £39, instant access.

- Structured response patterns for the questions senior presenters dread most

- The 45-second framework for calm, decision-safe answers under pressure

- Self-study, work through it at your own pace

- Instant download — start using it in your next committee meeting

- Designed for executive, board, and investment committee Q&A

Explore the Q&A Handling System →

Built around the structured patterns presenters use to recover authority when the brief and the room diverge mid-presentation.

A worked example: the market-entry committee

Take Saoirse’s situation, run forward as if she had used the structured response. The CEO has just cut in: “Saoirse, yes, but what’s YOUR recommendation?”

Part one — acknowledge: “That is the right question to ask, and I want to give you a useful answer rather than a polished one.” Eight seconds. The CEO leans back. The CFO’s pen pauses. The room is now waiting for substance.

Part two — criteria: “If I were to make a recommendation today, I would weight three criteria most heavily — capital efficiency in year one, regulatory tailwind from 2027 onwards, and our existing operational footprint within four hundred kilometres of the target market.” Twelve seconds. The CFO recognises capital efficiency as her language. The COO recognises operational footprint as his. The CEO recognises regulatory tailwind from the strategy review last quarter. Three criteria, three nods.

Part three — working view: “On those criteria, the option that scores highest is option two — the Polish market entry — primarily because of the lower capital requirement in year one and the regulatory tailwind we already track. That is a working view, not a final recommendation, because I have not yet stress-tested the operational ramp-up with the regional team in Frankfurt.” Eighteen seconds. She has named an option, stated her reasoning, and bounded the certainty by specifying what is missing.

Part four — timeframe: “I can return to the committee within ten working days with a formal recommendation that includes the operational stress-test.” Six seconds. The CEO checks his diary, says “good, put it on the agenda for the twentieth”, and Q&A moves on. Saoirse has held the room. Total time from cut-in to resolution: forty-four seconds.

The same structural pattern works in procurement reviews, succession decisions, capital allocation, and strategic hiring. The criteria change; the architecture does not. Senior presenters who have worked through the structured Q&A framework are markedly less likely to freeze when the recommendation question lands, because the architecture has already been internalised before the meeting starts.

What not to say in the moment

Three sentences in particular do disproportionate damage when the recommendation question lands. They feel safe to say. They are not.

“I haven’t been asked to recommend.” The CEO has just asked you. Saying you have not been asked is a contradiction with the room, and it positions you as someone whose understanding of the meeting is out of date.

“There are arguments both ways.” The indecision trap in seven words. The committee can see there are arguments both ways from your slides; they are asking which way you lean. Refusing to lean is the failure mode the question is testing for.

“I’d need to do more analysis.” Sounds rigorous, lands as dismissive. The committee is not asking for a final position; they are asking how you currently see it. If you genuinely need more analysis, the structured response builds that into part four — without leading with it.

The instinct to use any of these comes from wanting to protect the analysis. The structured response protects the analysis better, by giving the committee a working view and a timeline rather than a refusal. The same care for tone shows up in how presenters reset when the body’s stress response interrupts the voice — both situations need a structural recovery, not a content recovery.

Want the full framework before your next committee meeting?

The Executive Q&A Handling System gives you the complete library of structured response patterns for the questions senior presenters dread — calm authority, decision-safe answers, in 45 seconds. Instant download, full system, no waiting.

The preparation discipline that prevents the freeze

The four-part response works in the moment. The discipline that prevents the freeze in the first place sits in the preparation, and it is short enough to fit into any executive deck rehearsal.

Before any presentation where you are showing options rather than recommending, write three sentences for yourself in your speaker notes. One: “If I were forced to recommend right now, I would lean toward [option] because [criterion one] and [criterion two].” Two: “The single thing I have not yet stress-tested is [the missing analysis].” Three: “The realistic timeline to a formal recommendation is [number] working days, including [specific next step].”

Three sentences. Five minutes of work. If the question lands — which on any cross-option presentation to a senior committee, it usually does — your answer is already drafted. You are not improvising. You are reading from a position you thought through when you were not stressed. The structured response becomes a delivery mechanism for thinking you have already done.

This is also the discipline that handles the secondary versions — “what would you do if it were your money?”, “if you had to pick one tomorrow, which would it be?”, “what’s your gut here?”. All three are the recommendation question wearing different clothes. The same four-part response works for all of them. The presenter who has done the preparation walks into the room with a quiet confidence the committee can feel — the same confidence that lets them handle the credibility-of-numbers question without flinching when it arrives.

Stop dreading the questions you cannot predict.

If the recommendation question is the one you dread, it is rarely the only one. Most senior presenters carry three or four committee questions that consistently knock them off-balance — the credibility probe, the cost challenge, the timeline squeeze, the “what could go wrong?” pivot. The Executive Q&A Handling System gives you the structured patterns for all of them, so you stop walking into committee meetings rehearsing answers in your head on the way in. £39, instant access, self-study.

FAQ

What if the CEO genuinely wanted me NOT to recommend, and I have now given a working view?

The structured response is designed for this tension. By framing your answer as “a working view, not a final recommendation, because I have not yet stress-tested X”, you preserve the boundary the original brief set. You have given the committee enough to engage with without pre-empting the formal recommendation process. If the CEO afterwards says “I asked you not to recommend”, the reply is straightforward: “You asked me not to pre-empt the formal recommendation. I did not — I gave a working view, named it as such, and confirmed the timeline for the formal piece.” Most CEOs are content with this.

How long should the whole response actually take?

Forty-five to sixty seconds is the target. Senior listeners switch off after about a minute on a single Q&A response. The four parts are deliberately short — eight, twelve, eighteen, six seconds in the worked example — to fit inside that attention window. If you run over, the part that usually needs trimming is part three. Limit yourself to one option, two reasons, one boundary.

What if I genuinely have no view yet because the analysis is too early?

Then parts one, two, and four stay the same; part three becomes “I do not yet have a working view, because the analysis on [specific criterion] is the one that will most likely move the answer, and that work is in progress.” This is different from indecision because it names the specific piece of analysis that is missing. The committee learns that you have a structure for forming the view, you just have not arrived at it yet — a defensible position, provided part four still gives them a date.

The Winning Edge — Thursday newsletter

Every Thursday, The Winning Edge delivers one structural insight for executives presenting to boards, investment committees, and senior stakeholders. No general tips. No motivational framing. One specific technique, one executive scenario, one action. Subscribe to The Winning Edge →

Not ready for the full system? Start here instead: download the free 7 Presentation Frameworks Quick Reference Card — a single-page reference to the structural patterns most senior presenters return to most often.

Next step: pull up the next options-style presentation on your calendar — procurement review, market analysis, hiring panel, capital allocation — and write the three sentences of preparation in your speaker notes before you next rehearse it. If the recommendation question lands, you have an answer drafted. If it does not, the work has cost you five minutes.

Related reading: how to handle tough questions in presentations — the structural patterns that hold authority, and why should we believe your numbers? — handling the credibility challenge from a senior committee.

About the author. Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd, founded in 1990. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, approvals, and board-level decisions.