Quick Answer

A budget resubmission presentation should not simply re-present the original proposal with adjusted numbers. Finance committees that rejected your initial submission are looking for evidence that you understood why it was rejected, that you have addressed the underlying concerns, and that you can defend the revised case under scrutiny. The structure of the resubmission matters as much as the revised figures.

In This Article

- Why budgets are rejected and what finance actually needs

- The first move after rejection

- What to change — and what not to touch

- Structuring the resubmission presentation

- The three objections to address before they raise them

- Presenting the revision without looking defensive

- Frequently asked questions

Kenji had been Head of Technology at a retail banking group for two years when his infrastructure modernisation budget was rejected at the April finance committee. The committee’s feedback was brief: the proposal lacked sufficient evidence of ROI, and the timeline was considered optimistic given the organisation’s recent delivery record on technology projects.

His initial response was to rebuild the financial model. He spent three weeks tightening the numbers, adding sensitivity analyses, and extending the timeline by six months. When he presented the revised proposal in June, the committee rejected it again. This time the feedback was different: the committee was not confident the business case addressed the fundamental question of why this investment was necessary now rather than in the next financial year.

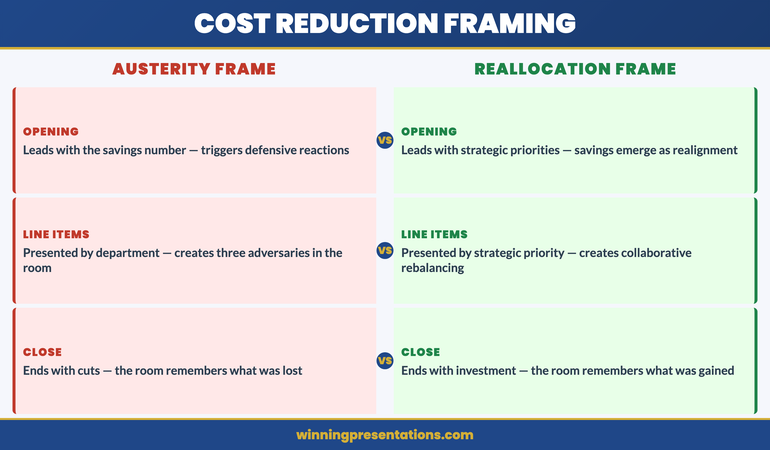

The financial model had never been the problem. The problem was that Kenji’s original presentation had led with capability and features — what the infrastructure would be able to do — rather than with risk and consequence — what would happen if the current infrastructure was not replaced. The committee had rejected the framing of the proposal, not just the numbers. Until the resubmission addressed that framing, no amount of revised modelling would produce a different outcome.

Preparing a budget resubmission?

Before you rebuild the model, check whether your slide structure addresses what the committee actually rejected. The Executive Slide System includes financial presentation frameworks designed for approval meetings, including resubmissions after rejection. Explore the System →

Why Budgets Are Rejected and What Finance Actually Needs

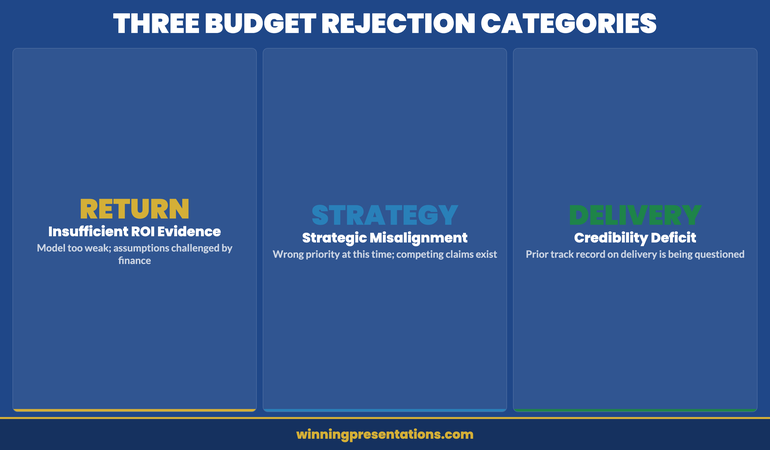

Budget rejections fall into three categories, and only one of them is actually about the numbers. Understanding which category your rejection belongs to determines what the resubmission needs to address.

The first category is insufficient evidence of return. The committee cannot see a credible path from the investment to a measurable outcome. This is a modelling and assumptions problem — and it is the only category where revising the financial model alone will resolve the issue. If you can provide tighter assumptions, stronger benchmarks, or a clearer articulation of how return will be measured and when, the resubmission has a direct path to approval.

The second category is strategic misalignment. The committee does not believe this investment is the right priority at this time, relative to other competing claims on the budget. No amount of modelling resolves this. The resubmission needs to demonstrate how this investment connects to the organisation’s current strategic priorities, and specifically why deferring it creates a worse outcome than approving it now.

The third category — the most common and the hardest to diagnose — is a credibility deficit. The committee is not confident that the presenter or their team can deliver what is being proposed. This is particularly acute when the organisation has a history of late or over-budget technology or infrastructure projects, which is a reason Kenji’s second submission failed. A resubmission that does not directly address the delivery confidence problem will not succeed, regardless of the quality of the financial model.

Most rejected budgets contain elements of all three. The task before the resubmission is to identify which is the dominant concern, because that determines the entire structure of the revised presentation.

The First Move After Rejection

The first thing to do after a budget rejection is not to revise the proposal. It is to understand precisely what was rejected and why. This sounds obvious, but most post-rejection conversations focus on what the presenter thinks the committee meant, rather than on getting the committee’s actual concerns on record.

Request a debrief, ideally with the finance director or the committee chair, within a week of the decision. The question to ask is not “what would it take to get this approved?” — which puts the committee in the position of designing your resubmission — but rather “what specific concerns were unresolved at the point of decision?” This frames the conversation as a diagnostic rather than a negotiation, and experienced finance directors will give you considerably more useful feedback if they feel they are being asked to help you understand rather than being pressured to change their minds.

Document the feedback carefully. When the resubmission is eventually presented, the committee will compare what they said to what you addressed. If the resubmission does not map directly to the documented concerns, it signals that you either did not understand the feedback or chose to work around it — neither of which builds confidence.

What to Change — and What Not to Touch

There is a common instinct to make the resubmission significantly different from the original — to demonstrate responsiveness and effort. This instinct is partially right and partially dangerous. Substantial changes that address the committee’s documented concerns signal that you listened and acted. Substantial changes that go beyond what was asked signal either that you had doubts about the original proposal that you did not disclose, or that you are making changes to appear responsive rather than because they are substantively right.

Change the structure of the case if the rejection was about framing. If the committee rejected the proposal because the rationale was wrong — capability-led rather than risk-led, for example — restructure the argument, not just the slides. The committee will recognise a slide reshuffle; they will not recognise a genuinely different argument unless it is genuinely different.

Change the financial assumptions if they were specifically challenged. If the committee requested more conservative growth projections or questioned the cost assumptions, revise them with explicit references to what changed and why. Do not quietly update figures without acknowledging the change — the committee will notice the difference and will want to know why the original numbers were presented if these more cautious assumptions were available.

Do not change anything that was not the subject of feedback. Altering elements of the proposal that the committee did not question suggests uncertainty about the original position, and invites new questions about material that was previously settled.

For guidance on structuring the financial argument itself, the approach in zero-based budget presentations is directly applicable to resubmissions where the original proposal was rejected on return-evidence grounds — the discipline of justifying each line from first principles removes the assumption problem that often underlies the “insufficient ROI” rejection.

Executive Slide System

Build Financial Presentations That Get Budget Approval

The Executive Slide System provides structured frameworks for financial and budget presentations, including resubmissions after rejection. It includes slide templates for finance committee meetings, AI prompt cards to build the case quickly, and scenario guides for challenging approval environments.

- Slide templates for budget and financial approval presentations

- AI prompt cards to structure the resubmission argument

- Framework guides for risk-led and return-led financial cases

- Scenario playbooks for budget, capex, and resource allocation items

Get the Executive Slide System — £39

Designed for budget and financial presentations in regulated and corporate environments.

Structuring the Resubmission Presentation

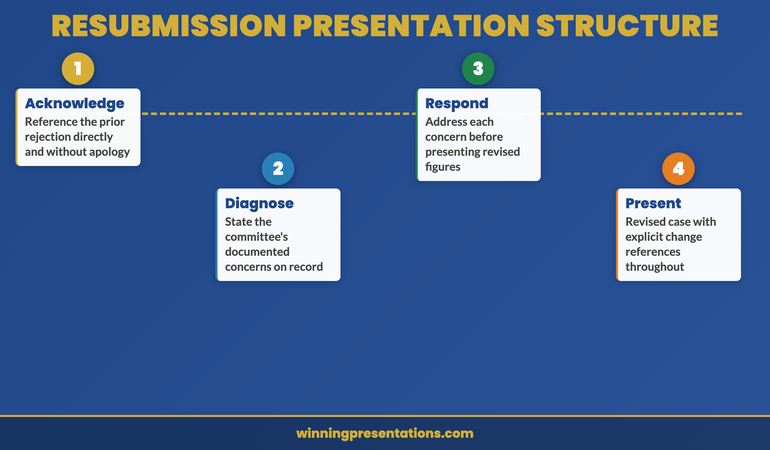

A budget resubmission presentation has a structural requirement that the original proposal does not: it must acknowledge the previous rejection before making the case. Presenting a revised budget as if the original was never rejected — simply updating the figures and re-presenting the slides — is the single most common structural error in resubmissions, and it consistently produces a worse reception than the original.

The committee knows this is a resubmission. Pretending otherwise reads as either oblivious or evasive. The structure that works is: acknowledgement, diagnosis, response, revised case.

Acknowledgement: Open with a brief, direct reference to the previous submission and its outcome. “This is a revised proposal for [project], following the committee’s decision in April. The original submission was rejected on two grounds, which I will address directly.” This signals that you are aware of the history, you are not defensive about it, and the resubmission is designed to resolve the specific concerns raised.

Diagnosis: State what you understood the committee’s concerns to be. If you had a debrief conversation, reference it. “Based on the feedback received from [name/role], the committee’s primary concerns were: [specific concerns].” This gives the committee the opportunity to confirm or correct your understanding before the revised case is presented, and it demonstrates that you conducted a genuine post-rejection diagnostic rather than simply revising the slides.

Response: Address each concern directly, in the order it was raised. Not buried in the appendix, not woven into the financial model — directly, as a standalone section that the committee can evaluate before the revised figures are presented. This is the part of the resubmission that most commonly gets cut for time, which is almost always a mistake. The committee’s concerns are the test the resubmission must pass; address them before asking for approval.

Revised case: Present the updated financial proposal, incorporating the changes made in response to the committee’s feedback, with explicit references to what changed and why.

For reference on how resource and financial proposals are typically structured for contested approval environments, the resource allocation presentation framework covers the argumentation approach that works when budgets are under direct competitive pressure.

The Three Objections to Address Before They Raise Them

In a resubmission, there are typically three objections that the committee will raise regardless of how comprehensively the original concerns were addressed. Addressing these proactively — before they are raised as questions — materially reduces the risk of a second rejection.

The first is: “Why should we approve this now rather than defer it to next year’s cycle?” This objection is almost always present when a budget was rejected once already. The committee may have approved an alternative proposal in the interim, making this one appear less urgent than it did six months ago. The resubmission needs a current-state argument: what has changed since the original submission, and how does that change affect the cost or risk of waiting a further twelve months?

The second is: “What gives us confidence the delivery will be successful?” This is particularly acute when the organisation has a track record of project overruns, or when the project scope has changed between the original and revised submissions. A resubmission that does not include a delivery confidence section — covering governance arrangements, milestone structure, and how delivery risk will be managed — will encounter this objection in the room.

The third is: “Is this the right amount?” After a rejection, committees are sensitive to whether the revised budget is genuinely right-sized or has simply been reduced to secure approval, with the expectation that a supplementary request will follow. If the budget has been reduced from the original, explain specifically what scope was removed to achieve the reduction, not just that the figure is lower.

Presenting the Revision Without Looking Defensive

The psychological challenge of a resubmission is presenting a revised case with full conviction when you know the committee has already said no once. The temptation is to over-qualify — to hedge the revised figures, acknowledge every uncertainty, and soften the recommendation. This reads as lack of confidence in the revised case, which is the last impression a resubmission needs to create.

The discipline is to hold the distinction between acknowledging the rejection and diminishing the recommendation. You can acknowledge the previous decision with directness and without apology, and then present the revised case with exactly the same conviction you would bring to a first submission. The rejection was of the previous case; this is a different case. It deserves to be presented as such.

Avoid two common tone errors. The first is apologetic framing — “I know you have concerns about this, and I hope this revised version addresses them” — which positions the presenter as petitioner rather than professional making a considered case. The second is over-confident dismissal — “I believe we have now resolved all the concerns raised” — which can read as arrogant and tends to provoke the committee into finding new concerns. The right tone is direct and measured: “The revised proposal addresses the specific concerns raised in April. Here is how.”

If the capital expenditure case involves significant infrastructure investment, the guidance in capital expenditure presentations covers how to frame large investment proposals in a way that holds up under scrutiny — including how to address delivery risk in the financial narrative itself rather than in a separate risk register that committees rarely read.

If your budget proposal has been rejected once and you are preparing the resubmission, the Executive Slide System includes financial presentation frameworks that address the structural requirements of a second-attempt approval, including how to lead with the committee’s previous concerns.

Executive Slide System

Slide Templates for Budget and Financial Approval Meetings

Structure your resubmission using frameworks designed for contested financial approvals — from the opening acknowledgement to the revised recommendation and delivery confidence section.

Get the Executive Slide System — £39

Designed for financial and budget presentations in corporate and regulated environments.

Frequently Asked Questions

How long should a budget resubmission presentation be?

A resubmission should typically be shorter than the original proposal, not longer. If the original was rejected because the case was unclear, adding more slides rarely resolves the problem — it usually compounds it. The acknowledgement-diagnosis-response-revised case structure can typically be delivered in eight to twelve slides, with supporting detail in the appendix. The committee has already read a version of this proposal; they do not need the full context again. They need to see that their specific concerns have been addressed and that the revised figures are sound.

Should you request a meeting with the finance director before the formal resubmission?

Yes, where possible. A pre-meeting with the finance director or a relevant committee member before the formal resubmission gives you the opportunity to test whether your revised case addresses their concerns before the formal meeting, and it signals engagement with the feedback process rather than a determination to push the proposal through regardless. It is not appropriate to use this meeting to lobby for approval — it is a diagnostic conversation, not a pre-vote. The question to ask is whether your diagnosis of the rejection matches their recollection of the discussion.

What should you do if the budget is rejected a second time?

Request a direct conversation with the committee chair or finance director to understand whether the objection is to this proposal specifically or to the priority of the investment in the current environment. If the committee has a fundamental view that the investment should not happen now — regardless of the quality of the case — no amount of revised modelling will change the outcome. The more productive path is to understand what conditions would need to change for the proposal to succeed, and to determine whether those conditions are likely to be met within a timeframe that makes the investment still relevant.

The Winning Edge — Weekly Newsletter

Each Thursday: one executive presentation insight, one structure, one practical tool. Read by executives across financial services, healthcare, technology, and infrastructure.

Preparing a budget or financial approval presentation? The Executive Presentation Checklist is a free download covering structure, language, and approval-readiness for finance committee and board presentations.

About the Author

Mary Beth Hazeldine is Owner and Managing Director of Winning Presentations. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and governance reviews. View services | Book a discovery call