Investor Q&A: The Follow-Up Questions That Kill Funding (And How to Prepare for Them)

Most investor presentations don’t collapse on the first question. They collapse on the second one.

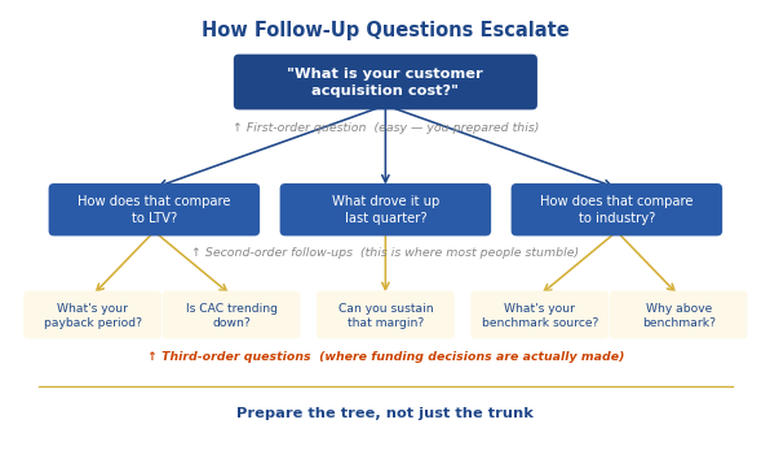

The founder answers the opening question confidently — “what’s your customer acquisition cost?” — with a specific number and a clear explanation. Then the investor asks: “And how does that break down by channel?” Pause. Then: “What’s the trend over the last four quarters?” Another pause. Then: “What’s driving the increase in Q3?” By the fourth question, the founder is visibly reaching for data they don’t have immediately available. By the fifth, the room has reached a conclusion about how well the business is understood.

The first answer wasn’t wrong. The follow-ups revealed the boundaries of preparation. That’s where investor Q&A funding conversations are actually decided — not on whether you can answer the initial question, but on how far into the second order your preparation extends.

Quick answer: Investor Q&A follow-up questions follow predictable patterns. Every first-order question about metrics, strategy, or competitive positioning has three or four second-order follow-ups that experienced investors use to test the depth of understanding behind the initial answer. Preparing for the follow-ups — not just the opening questions — is what separates funded founders and executives from those who present well but leave investors uncertain. The preparation method is systematic: map each expected question, then generate the three most likely follow-ups for each, and prepare answers to all of them.

📋 Preparing for an investor Q&A this week? The Executive Q&A Handling System (£39) includes the investor Q&A framework with the second-order question map, preparation templates, and exact language for handling the questions most people aren’t ready for.

Jump to:

- Why Follow-Up Questions Are Where Funding Is Decided

- The Follow-Up Map: Metrics Questions

- The Follow-Up Map: Strategy Questions

- The Follow-Up Map: Competitive Questions

- The Follow-Up Map: Risk Questions

- The Preparation System That Covers Second-Order Questions

- Is This Right For You?

- Frequently Asked Questions

I spent 24 years in corporate banking at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank. I have been in rooms where capital decisions were made — and in rooms where they weren’t, despite a strong headline pitch. The difference between those outcomes was rarely the first question and almost always what happened in the third and fourth.

Experienced investors are not trying to catch you out with follow-up questions. They’re trying to assess something specific: how deeply you understand your own business, and whether the answers you gave to the opening questions were genuinely grounded or were polished responses built for presentation rather than for interrogation.

The preparation framework that works isn’t “know your numbers.” Every funded founder knows their headline numbers. It’s “know the story behind every number, the story behind that story, and where the story breaks down.” That’s three levels deep. Most preparation stops at the first.

Why Follow-Up Questions Are Where Funding Is Decided

An investor who asks a follow-up question is not being difficult. They’re doing exactly what their role requires: assessing whether the person in front of them has the depth of understanding to manage the capital they’re being asked to commit.

The follow-up question serves a diagnostic function. If the first answer was memorised or prepared for the pitch, the follow-up will surface that. If the first answer was grounded in genuine understanding, the follow-up is easy — because the same understanding that produced the first answer produces the second one naturally, without additional preparation.

This is why investor Q&A preparation that only covers anticipated first-order questions consistently fails. Founders spend hours preparing answers to “what’s your CAC?” and “who are your main competitors?” and “what’s your burn rate?” — and are then derailed by “how does CAC vary by segment?” or “what’s your win rate against that competitor specifically?” or “at current burn, what’s your runway if the next round takes six months longer than expected?”

The follow-up isn’t harder to answer than the original question. It’s harder only if the answer to the original question was a prepared surface response rather than an expression of genuine understanding. The diagnostic function of the follow-up is precise: it distinguishes one from the other.

Today’s sister article on the investor relations presentation format covers how to structure the deck itself to prevent questions before they’re asked. This article covers the Q&A that follows — and specifically the follow-ups that most preparation misses.

📋 The Investor Q&A Framework That Prepares You Three Questions Deep

The Executive Q&A Handling System includes the investor Q&A preparation framework — the second-order question map, the preparation templates, and the exact language for handling follow-ups on metrics, strategy, competition, and risk:

- The investor follow-up question map for each major Q&A category — what experienced investors ask second, third, and fourth

- Preparation template: map your first-order answers and generate second-order questions systematically before the meeting

- Language for handling questions where the honest answer isn’t the one you planned — without losing credibility

- The bridging technique for redirecting follow-ups that are moving into territory you want to control

- How to answer “I don’t know” in a way that builds rather than erodes investor confidence

Get the Executive Q&A Handling System → £39

Built from 24 years in corporate banking and executive Q&A preparation at JPMorgan Chase, PwC, and RBS — including preparing executives for investor presentations and funding rounds.

The Follow-Up Map: Metrics Questions

Every metric question an investor asks has a predictable set of follow-ups. Here are the most common, across the metrics categories that matter most in investor conversations.

Customer acquisition cost (CAC). First order: “What’s your CAC?” The follow-ups investors actually use: “How does that break down by channel?” “What’s the trend over the last four quarters?” “What’s driving the change?” “How does that compare to your LTV at different customer segments?” Preparation means knowing the channel breakdown, the trend, the driver, and the LTV-to-CAC ratio by segment — not just the headline CAC number.

Revenue growth. First order: “What’s your revenue growth rate?” Follow-ups: “New versus expansion revenue?” “Churn rate?” “Net revenue retention?” “What’s the growth rate of your top 10 accounts?” Most founders prepare the growth rate headline. Experienced investors are trying to understand whether that growth is healthy or fragile — new customer acquisition masking significant churn, or a stable expanding base. The follow-ups diagnose which.

Burn rate and runway. First order: “What’s your current burn?” Follow-ups: “How does that compare to six months ago?” “What are the main drivers of burn?” “What happens to burn if you hit your growth targets?” “What levers do you have if you need to extend runway?” Prepare the drivers, the sensitivity, and the optionality. Investors are stress-testing your understanding of the cash dynamics, not just the headline number.

Preparing for an investor meeting? The Executive Q&A Handling System (£39) includes the full investor follow-up question map across metrics, strategy, competitive, and risk categories.

The Follow-Up Map: Strategy Questions

Go-to-market strategy. First order: “What’s your GTM strategy?” Follow-ups: “What’s working best right now and why?” “What have you tried that hasn’t worked?” “What does the unit economics look like at scale?” “How does your GTM need to change when you move upmarket?” Most prepared answers describe the intended strategy. Investors want to know whether you’ve run it, what you’ve learned from running it, and whether your unit economics work beyond the current stage.

Pricing strategy. First order: “How did you arrive at that pricing?” Follow-ups: “Have you tested higher price points?” “Where do you lose deals on price?” “What’s the average contract value trend?” “How does your pricing compare to your top competitor in a head-to-head?” The follow-up questions are probing your pricing confidence — whether it’s based on customer research and competitive intelligence, or on a number that felt reasonable when you set it.

Expansion strategy. First order: “What’s your expansion plan?” Follow-ups: “What are the three biggest risks to the expansion timeline?” “What milestones do you need to hit before you can expand?” “Who else has expanded into that market and what happened to them?” “What does the team composition need to look like to execute?” Investors are looking for realistic planning versus aspirational planning. The follow-ups test whether you’ve worked the plan backwards from the risks.

The Follow-Up Map: Competitive Questions

Competitive positioning. First order: “Who are your main competitors?” The follow-ups: “What do customers choose them over you for?” “What’s your win rate against [specific competitor]?” “What would need to change for a customer to switch back to them?” “What are they doing now that concerns you?” Most competitive answers describe why you’re better. Investors want to understand whether you have accurate intelligence on your competitors’ strengths — not just their weaknesses.

Defensibility. First order: “What’s your competitive moat?” Follow-ups: “How long would it take a well-resourced competitor to replicate your key advantage?” “What assumptions is your moat argument dependent on?” “What happened to the last company that had this advantage?” The defensibility follow-up is almost always about identifying which assumptions the moat depends on. Prepare your moat argument and then prepare the honest answer to “what would need to be true for this advantage to erode?”

⚠️ Stop Being Derailed by the Questions You Didn’t Prepare For

Most investor Q&A preparation covers the opening questions. The Executive Q&A Handling System (£39) includes the follow-up question maps that prepare you three levels deep — so you know exactly how to answer what comes after the first answer.

Get the Executive Q&A Handling System → £39

Used by executives and founders preparing for investor presentations, board meetings, and high-stakes funding conversations.

The Follow-Up Map: Risk Questions

Key person risk. First order: “What happens if you leave?” Follow-ups: “Who on your team could step up?” “What’s been documented so far?” “What would a succession plan look like?” “What would make you leave?” The key person question is expected. The follow-ups are probing whether you’ve actually thought about business continuity or whether “we’re building the team” is a placeholder answer.

Regulatory and legal risk. First order: “What are your main regulatory risks?” Follow-ups: “Have you had any regulatory interaction to date?” “What’s your current legal spend and what’s it for?” “What happens to your business model if [specific regulation] changes?” Prepare the honest answer to the regulatory question, then prepare the follow-up on what you’ve done about it, not just what the risk is.

Technology or execution risk. First order: “What’s the biggest technical risk to delivery?” Follow-ups: “What’s the fallback if that risk materialises?” “Have you had any incidents so far and how did you handle them?” “What does your testing and validation process look like?” Investors are testing whether you have realistic risk management or optimistic risk assessment. The follow-ups are designed to find out.

The CFO presentation framework uses the same principle: financial decision-makers always have prepared follow-ups for every first-order answer, and the presenter who knows what those follow-ups are enters the conversation at a significant advantage.

The Preparation System That Covers Second-Order Questions

The preparation method is straightforward once you understand what it’s for. It has four steps.

Step 1: List every question you expect. Not the questions you hope to get — every question that could reasonably arise across metrics, strategy, competitive positioning, team, and risk. This is your first-order question bank. Most founders have this. Most stop here.

Step 2: For each first-order question, generate three follow-ups. Ask yourself: if I give my planned answer to this question, what’s the next question an experienced investor would logically ask? Then ask it again: and if I answer that, what’s the next one? Three levels. Some questions will only have one or two logical follow-ups. Others will have five. The discipline of generating three forces you to think past your prepared surface answer.

Step 3: Prepare honest answers to the difficult follow-ups. Some of the follow-ups will surface genuine gaps — numbers you don’t know, assumptions you haven’t tested, risks you haven’t fully modelled. This is the most valuable part of the exercise: discovering your preparation gaps before the investor does. Where you have gaps, fill them. Where they can’t be filled before the meeting, prepare an honest, credible answer to “I don’t have that to hand, but here’s what I do know.”

Step 4: Run the preparation with a colleague who hasn’t seen it. The preparation that stays in your head isn’t tested. Having someone else ask you the first-order questions — then follow up unprompted — reveals whether your preparation is actually solid or whether it still has surface areas that look prepared but break down three questions in. The executive presentation structure that works in investor contexts is built to handle Q&A, not just delivery — and practising the Q&A is as important as rehearsing the deck.

Also published today: The Investor Relations Update Format That Prevents Awkward Questions — how to structure the deck itself so that many Q&A questions never need to be asked.

Common Questions About Investor Q&A Preparation

How many investor questions should I prepare for?

Prepare for every question you can anticipate, but the preparation that matters is the second-order follow-ups — not just additional questions. A bank of 40 first-order questions with no follow-up preparation is less valuable than 15 first-order questions, each with three follow-ups you’ve genuinely worked through. Quality of preparation depth matters more than quantity of questions covered.

What should I do when an investor asks a question I genuinely don’t know the answer to?

The honest answer is nearly always more effective than a deflection. The specific phrasing matters: “I don’t have that number with me, but I can tell you that [related thing you do know] — I’ll get you the exact figure after this meeting.” That response demonstrates honesty, demonstrates that related knowledge is solid, and demonstrates that you’ll follow through. What damages credibility is the visible search for an answer that isn’t there, or an answer that clearly isn’t what was asked.

How do investors use follow-up questions differently from opening questions?

Opening questions often probe what you know. Follow-up questions probe how you know it and how deeply. “What’s your CAC?” tests whether you have the number. “What’s driving the increase in Q3?” tests whether you understand why the number is what it is. Investors are assessing both layers simultaneously — but the follow-up is where the second layer is actually examined.

Is This Right For You?

✅ This is for you if:

- You’re preparing for an investor presentation, board meeting, or funding conversation where Q&A is a significant part of the session

- You’ve been caught out by follow-up questions in previous investor meetings and want to close those preparation gaps

- You want a systematic method for preparing Q&A, not just a list of questions to memorise

❌ This is NOT for you if:

- You’re preparing for an internal Q&A with colleagues rather than external investor scrutiny (the stakes and preparation depth differ)

- You’re looking for guidance on the deck structure itself rather than the Q&A — that’s covered in the IR update format article published today

🏛️ The Q&A System Built From 24 Years of Watching What Investors Actually Test

The Executive Q&A Handling System is built on a simple premise: the questions that kill funding are not the ones you’ve prepared for. They’re the follow-ups that expose whether the prepared answers were grounded or polished:

- The investor follow-up question map across metrics, strategy, competitive, and risk categories

- The four-step preparation system for generating and answering second-order questions before the meeting

- Language for handling difficult follow-ups — including the honest “I don’t know” that builds credibility rather than eroding it

- The bridging technique for redirecting follow-ups into the territory you’ve prepared without appearing to deflect

- Q&A preparation templates for the eight most common investor meeting formats

Get the Executive Q&A Handling System → £39

Built from 24 years in corporate banking at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank — including preparing executives for investor Q&A, board scrutiny, and high-stakes funding conversations.

Frequently Asked Questions

How do follow-up questions in investor Q&A differ from those in a board presentation?

Board Q&A follow-ups are typically aimed at governance, accountability, and strategic direction — boards are testing whether management understands the decision they’re being asked to approve. Investor follow-ups are more specifically financial and risk-focused — investors are assessing whether the business model and management team warrant the capital commitment. The preparation principles are similar (prepare three levels deep, know the story behind every number), but the territory of the follow-ups is different. The investor Q&A preparation described in this article is specific to investor and fundraising contexts; for board Q&A preparation, the approach is adapted but the underlying method is the same.

What if an investor keeps following up with increasingly detailed questions I can’t fully answer?

The most effective response is to draw a clear line honestly: “That level of detail is in the data room rather than in my head — I’d rather give you accurate numbers than approximate ones. Can I get that to you by end of week?” This response is more credible than an attempted answer that turns out to be imprecise. Experienced investors understand that not every figure is memorised; what they’re assessing is whether the response to uncertainty is honest and organised, or defensive and evasive. The former is reassuring. The latter is not.

How long before a funding meeting should I start Q&A preparation?

The second-order question preparation is most effective when done at least five days before the meeting — not because the content changes, but because the follow-up mapping exercise surfaces preparation gaps that take time to close. If you identify a gap the day before the meeting, you may not be able to fill it; if you identify it a week out, you can get the number, build the analysis, or at least form a credible bridging response. The preparation itself takes three to four hours for a thorough investor meeting. The rehearsal — having a colleague ask first-order questions and follow up unprompted — needs a separate two-hour session.

Should I prepare differently for angel investors versus institutional VCs?

The depth of preparation required is broadly similar, but the territory of follow-up questions differs. Angel investors often focus heavily on founder background, motivation, and resilience — the follow-ups to “what’s your exit strategy?” or “why are you the right person to build this?” tend to be character and commitment-based. Institutional VCs are more likely to pursue financial model follow-ups, comparable transactions, and market sizing logic in detail. Preparing for both audiences requires the same systematic mapping approach, but with different follow-up question banks for each.

The Winning Edge — weekly insight on Q&A handling, executive presentations, and investor communication. Subscribe free →

Want everything in one place? The Complete Presenter Bundle (£99) includes the Executive Q&A Handling System, the Executive Slide System, Conquer Speaking Fear, and four additional products.

About the Author

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she has delivered high-stakes presentations in boardrooms across three continents.

A qualified clinical hypnotherapist and NLP practitioner, Mary Beth combines executive communication expertise with evidence-based techniques for managing presentation anxiety. She has trained thousands of executives and supported high-stakes funding rounds and approvals.