Quick Answer

Presentation Q&A preparation moves from reactive to systematic when you pressure-test your answers before entering the room. This means categorising the questions you are likely to face, identifying the gaps your data does not cover, rehearsing with an adversarial questioner, and building a response framework for the questions you cannot fully answer. Rehearsing answers you already know is not preparation — it is confirmation. Real preparation stress-tests the limits of what you know.

In this article:

- Why rehearsing your answers is not enough

- The four categories of pressure question every executive faces

- The stress-test method: how to run an adversarial Q&A

- Pressure-testing your data and the numbers behind your slides

- Building a framework for questions you cannot fully answer

- When pressure-testing reveals a real gap

- Frequently asked questions

Kwame had run the numbers six times. As CFO of a mid-size logistics company, he had presented budget proposals to the board before — but this one was different. The proposal involved a £4.2 million capital commitment to upgrade a fleet management system, and the board had already pushed back twice on discretionary spending. He had built what he believed was an airtight case.

The presentation itself went well. The slides were clear, the narrative was coherent, and the ROI model was thorough. Then, at the twelve-minute mark, the Chairman asked a question Kwame had not seen coming: “Before we go further, Kwame — what assumptions are you making about fuel price movements over the implementation period, and have you stress-tested the ROI against a thirty per cent increase?”

Kwame knew the answer in principle. But he had not built that specific scenario into the model. He hedged. He said he could run those numbers after the meeting. The Chairman nodded, but the energy in the room shifted. Two other board members asked follow-up questions he handled less confidently than the main presentation had suggested he would. The proposal was deferred for a second meeting.

Afterwards, the CFO of the parent company — who had been in the room as an observer — pulled Kwame aside: “The proposal was solid. But you walked in having rehearsed what you know and hoping they wouldn’t ask what you don’t. That’s not preparation. That’s optimism.”

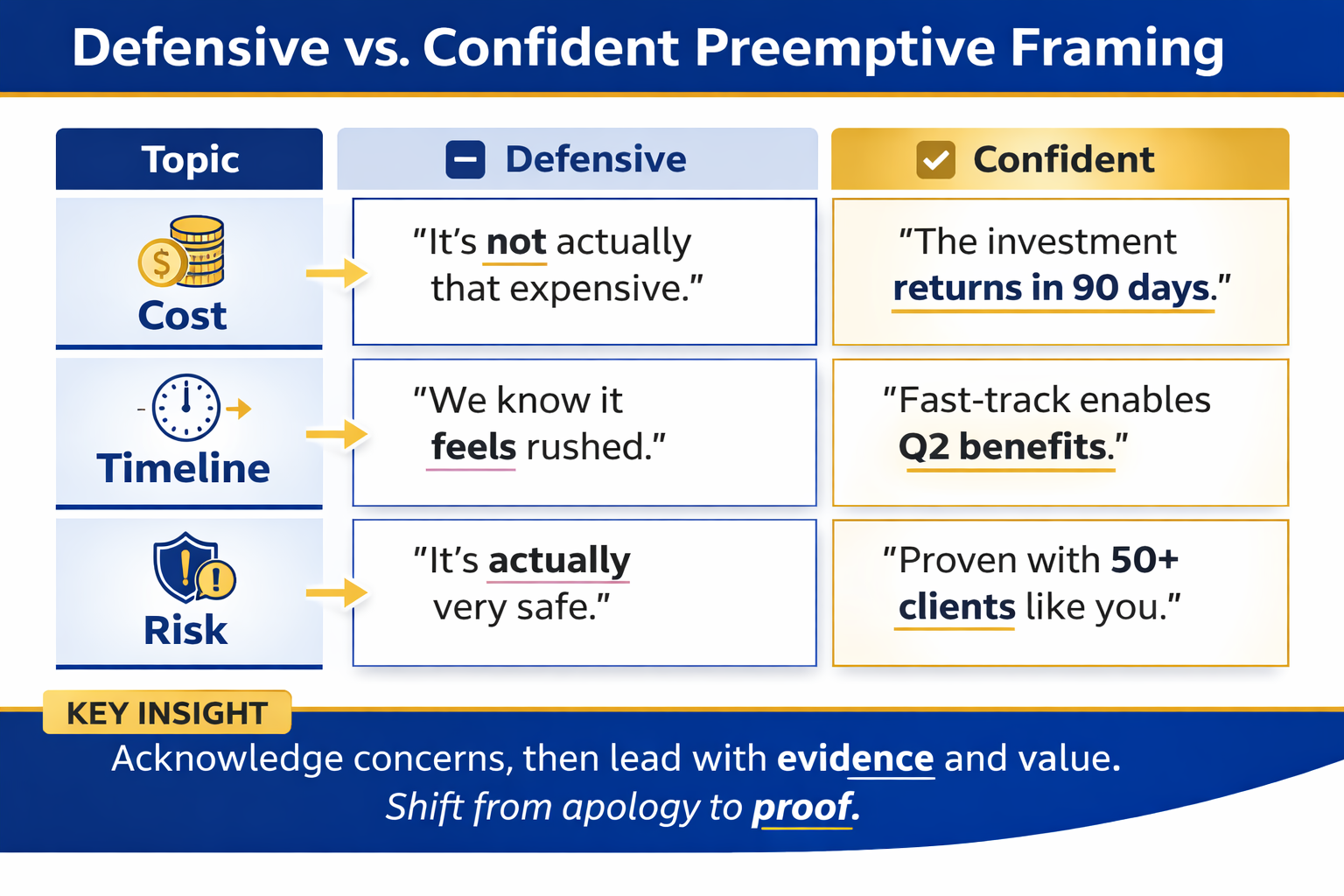

Systematic presentation Q&A preparation is not about practising the answers you already have. It is about identifying the assumptions embedded in your case, finding the weakest points in your data, and constructing a response framework that holds up even when the question lands outside your prepared territory.

Need a systematic Q&A preparation framework?

The Executive Q&A Handling System gives you a structured method for anticipating, categorising, and preparing responses to the questions that derail executive presentations — before you walk into the room. Explore the System →

Why rehearsing your answers is not enough

Most executives who prepare for Q&A do so by thinking through the questions they expect to receive and running through their answers mentally or verbally. This is better than no preparation. But it has a fundamental limitation: you are rehearsing a conversation you have already imagined, which means you are only testing your ability to deliver answers you have already constructed.

Real Q&A pressure does not come from the questions you expected. It comes from the question you did not see coming — the one that probes an assumption you made but did not flag, the one that connects two data points in a way that reveals a tension in your model, or the one that is framed in a way that makes any direct answer politically difficult. Rehearsing expected questions builds fluency in territory you already control. It does not build resilience in territory you do not.

The distinction matters most in the moments after a difficult question lands. An executive who has only rehearsed their prepared answers will feel a spike of alarm when the unexpected question arrives, because it signals that they are outside the plan. That alarm shows — in the hesitation before they speak, in the way their answer trails off rather than concluding, in the eye contact that breaks rather than holds. An executive who has actively pressure-tested the limits of their case approaches the unexpected question differently: they know the shape of their uncertainty, which means they can navigate it without being surprised by it.

For a related approach to handling the most confrontational form of unexpected question, see how to handle a hostile question in a board meeting without losing the room.

The four categories of pressure question every executive faces

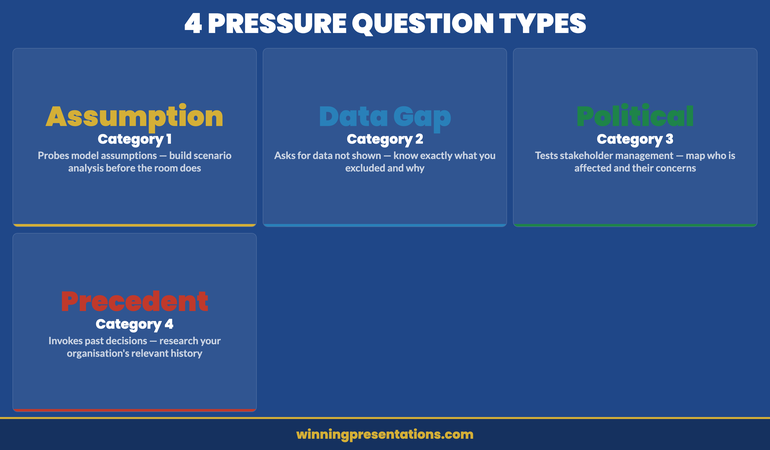

Pressure questions in executive presentations fall into four distinct categories. Understanding which category a question belongs to is the first step in building a preparation method that covers all of them.

Category 1: Assumption challenge questions. These questions probe the assumptions embedded in your model, forecast, or recommendation. “What are you assuming about interest rates over that period?” “Have you modelled the downside scenario?” “What happens to the ROI if adoption is slower than forecast?” These questions are often the most embarrassing to be caught unprepared for, because the assumptions are visible to anyone who looks closely at your analysis — which suggests you have not looked closely enough yourself.

Preparation method: For every key number in your presentation, write down the two or three assumptions that number depends on. Then build a simple scenario: what does the model look like if each assumption is twenty per cent worse than your base case? You do not need to present these scenarios — you need to know the answers so you can give them when asked.

Category 2: Data gap questions. These questions ask about data you have not included, either because you chose not to or because you did not have it. “Do you have a comparable from another division?” “What does the competitor analysis show?” “Have you validated this with the operational team?” These questions can reveal either that your analysis is incomplete or that you have made a deliberate choice not to include something — and the audience will wonder why.

Preparation method: Before finalising your deck, ask yourself what data an informed sceptic would expect to see but cannot find in your slides. Either include it or prepare a clear explanation of why you have not.

Category 3: Political implication questions. These questions are not really about your analysis — they are about the politics of the decision. “How does this affect the northern division?” “Has this been discussed with the operations board?” “Who owns the implementation risk?” These questions signal that the questioner has a stakeholder interest in the outcome and is testing whether you have addressed it. They can feel like hostile questions but are usually legitimate governance concerns.

Preparation method: Map the stakeholders who will be affected by your recommendation and anticipate the concern each one would raise. Prepare a one-sentence response to each concern that acknowledges it and names how it is being managed.

Category 4: Precedent questions. These questions invoke a previous decision or a comparable situation to test the consistency of your current recommendation. “When we approved a similar programme in 2023 it took twice as long as the forecast — why will this be different?” “We had a similar analysis for the IT project and it underestimated the integration costs. Have you accounted for that?” These questions require specific knowledge of the precedent being cited and a clear, factual explanation of what is different this time.

Preparation method: Research your organisation’s relevant history before the presentation. If there are obvious precedents the audience will raise, address them proactively in the deck rather than waiting for the question.

Executive Q&A Handling System

Anticipate, Prepare, and Handle Every Pressure Question

The Executive Q&A Handling System — £39, instant access — gives you a structured system for predicting the questions your specific audience is likely to ask, building response frameworks for each category of pressure question, and managing the Q&A process so that difficult questions strengthen rather than undermine your credibility.

- System for predicting and categorising executive Q&A questions

- Response frameworks for assumption challenges, data gaps, and political questions

- Adversarial rehearsal guides for high-stakes presentation settings

- Recovery strategies for questions that expose genuine gaps in your analysis

Get the Executive Q&A Handling System →

Designed for executives who face high-stakes Q&A in board, committee, and investor settings.

The stress-test method: how to run an adversarial Q&A

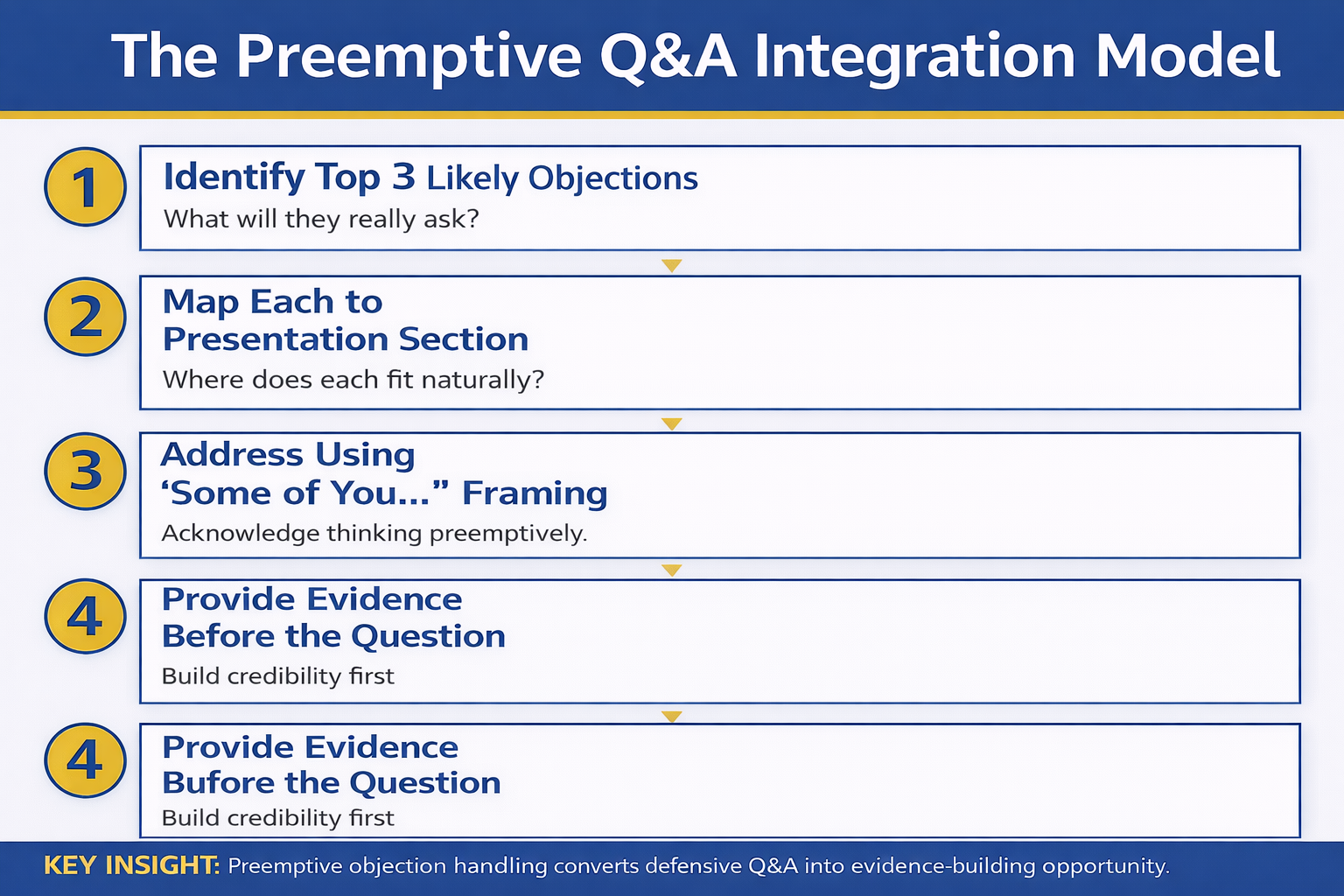

The most effective Q&A preparation method is the adversarial rehearsal — a structured session in which a trusted colleague, mentor, or adviser tries to find the weaknesses in your case by asking the most difficult questions they can generate. This is fundamentally different from a practice run, where the colleague asks supportive clarifying questions and you deliver your prepared answers. An adversarial rehearsal has a specific goal: to find the questions that you cannot answer well and identify what that reveals about your preparation.

The setup matters. Give your adversarial questioner the following brief before the session: “Your job is not to help me practise. Your job is to find the weakest point in my case and keep pushing until I either give you a satisfying answer or we identify a genuine gap. Ask the same question differently if I give you a vague answer. Escalate if I give you a deflection. I need to know where my preparation is thin.”

During the adversarial rehearsal, track the questions you struggle with in three categories. Questions you struggled with because you do not know the answer are a preparation gap — you need to either find the answer or prepare an explicit response to not knowing it. Questions you struggled with because the answer reveals a tension in your case are a content gap — you may need to adjust the recommendation or explicitly acknowledge the tension in the presentation. Questions you struggled with because the framing caught you off-guard are a rehearsal gap — you need to practise responding to the same content delivered in different, more challenging framings.

One session of genuine adversarial questioning will reveal more about the vulnerabilities in your Q&A preparation than ten sessions of practising your prepared answers.

Pressure-testing your data and the numbers behind your slides

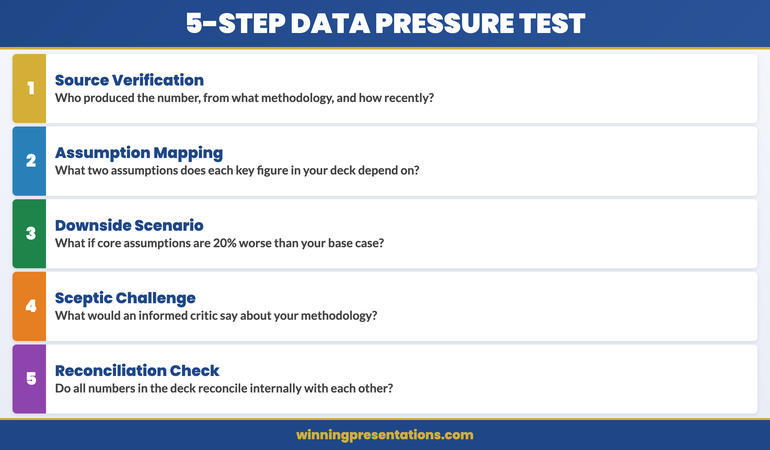

Every number that appears on a slide in a high-stakes executive presentation will be interrogated by at least one person in the room. The question is whether that interrogation will happen before or after you walk in. Pressure-testing your data means asking, for every significant number: what is the source, what are the assumptions, what happens if the assumptions are wrong, and what would a sceptic say about the methodology?

The source question is the most basic and the most frequently neglected. If you are presenting a market size figure, a cost estimate, or a timeline, you should be able to state immediately who produced that number and how recently. A number from a report published two years ago presented as current market data is a vulnerability. An estimate produced internally without external validation is a vulnerability. Neither of these need prevent you from using the number — but you need to know they are vulnerabilities before someone else identifies them.

The reconciliation check is particularly important in financial presentations. Every number in your deck should reconcile with every other related number. If your cost estimate on slide four implies a certain unit cost, and your volume forecast on slide seven implies a different unit cost, a sharp analyst in the room will find the inconsistency. Running a systematic reconciliation across your slides — not just checking individual numbers but checking that the numbers are internally consistent — is a discipline that most presenters skip and most experienced audiences notice the absence of.

For a structured approach to buying time when a data question catches you short, see buying time in Q&A: techniques for managing questions you need a moment to answer.

If you want a structured system for building and running this kind of adversarial Q&A preparation before high-stakes presentations, the Executive Q&A Handling System includes question prediction frameworks, adversarial rehearsal guides, and response strategies for each category of pressure question.

Building a framework for questions you cannot fully answer

Pressure-testing will sometimes reveal that you genuinely do not have the answer to a question the audience is likely to ask. This is not a failure of preparation — it is the purpose of preparation. Finding these gaps before the room does is exactly what the process is designed to do. The question is what to do with them once you have found them.

There are three legitimate responses to a question you cannot fully answer, and one illegitimate one. The illegitimate response is to deflect — to give an answer that sounds responsive but does not actually address the question. Experienced questioners recognise deflection immediately, and it damages credibility far more than an honest acknowledgement of a gap.

The first legitimate response is to close the gap before the meeting. If pressure-testing reveals that you do not know your fuel price assumptions, get the answer before the presentation. Many gaps that feel large in the preparation phase are actually addressable with a few hours of additional analysis or a conversation with a colleague.

The second legitimate response is to acknowledge the gap explicitly in the presentation, frame it as a known uncertainty, and name how you are managing it. “The model does not include a scenario for a thirty per cent fuel price increase. We have not modelled that because it falls outside the range our supply chain team considers realistic — but if the board would find it useful, I can run that scenario and bring it to the next meeting.” This response is far stronger than being caught by the question.

The third legitimate response is to answer the spirit of the question without answering the exact question: “I don’t have that specific number with me, but the broader point you’re making about input cost sensitivity is addressed in the sensitivity analysis on slide nine — would it help to walk through that section?” This only works when the redirect is genuinely responsive to the concern behind the question, not a deflection dressed up as engagement.

For a structured bridging technique that supports these responses in the moment, see the bridging technique for difficult presentation questions: how to navigate without losing credibility.

When pressure-testing reveals a real gap

Occasionally, adversarial Q&A preparation does not just identify a question you cannot answer — it reveals that the case you are making has a genuine substantive weakness. The numbers do not hold up to a simple sensitivity analysis. The recommendation depends on an assumption that is clearly contestable. The implementation plan has a dependency that has not been addressed.

When this happens, the temptation is to press ahead anyway — the presentation is scheduled, the slides are built, and the gap might not come up. This is the wrong choice. A real gap that emerges in the room — that you were aware of and chose not to address — damages your credibility as a presenter and as an analyst in ways that take much longer to recover from than a delayed presentation.

The appropriate response is to decide, before the meeting, whether the gap is material enough to delay the presentation. If the gap would change the recommendation — or would change the conditions under which the recommendation holds — it is material, and the presentation should be delayed until the gap is addressed. If the gap is peripheral — it does not affect the core recommendation but represents a risk the audience should be aware of — it should be disclosed proactively in the presentation, not concealed in the hope it will not be raised.

Executives who earn lasting credibility in high-stakes Q&A settings are those who demonstrate that they have stress-tested their own analysis before presenting it. That quality of rigour is visible — in the specificity of their answers, in their ability to name the assumptions in their model, and in their comfort with the limits of what they know. It is the quality that adversarial Q&A preparation builds.

For a companion resource on presenting with confidence in the room, see presentation gestures: the body language signals that build executive credibility.

Executive Q&A Handling System — £39

The System Behind Executives Who Handle Tough Q&A With Clarity

The Executive Q&A Handling System — £39, instant access — gives you a structured method for predicting and preparing for every category of pressure question, running adversarial rehearsals, and managing the Q&A process so that difficult questions strengthen rather than undermine your credibility in the room.

Get the Executive Q&A Handling System →

Designed for executives who face high-stakes Q&A in board, committee, and investor settings.

Frequently Asked Questions

How much time should I allocate to Q&A preparation before a major presentation?

For a high-stakes presentation — board, investor, or senior committee — allocate at least as much time to Q&A preparation as to slide preparation. In practice, this is rarely done: most executives spend ninety per cent of their preparation time on the deck and twenty minutes on Q&A. The imbalance is understandable, because slide preparation is a creative task with a clear output, whereas Q&A preparation is an analytical task with an uncomfortable one. The adversarial rehearsal session should run for at least sixty minutes for a significant presentation. Data pressure-testing — checking sources, assumptions, and internal consistency — is a separate exercise and should be treated as a quality check on the analysis, not just the communication.

Is it better to ask a colleague or a senior mentor to run the adversarial Q&A?

A senior mentor or someone from outside your team is typically more effective than a close colleague. The problem with colleagues is that they are often too familiar with your context to ask genuinely challenging questions — they fill in the gaps with their own knowledge rather than exposing the gaps as the audience would. A mentor or trusted senior peer who does not know your specific project in detail is more likely to ask the naïve but important question that the audience will also ask. If you do use a colleague, brief them explicitly to ask the questions they think the sceptics in the room will ask — not the questions they themselves would ask as a supportive peer.

What should I do if I get a question in the room that I am genuinely not able to answer?

Say so — specifically and without apology. “I don’t have that figure with me, and I don’t want to give you a number I haven’t verified. I’ll get it to you by close of business today.” This response is more credible than a hedged estimate, more respectful than a deflection, and far less damaging than a wrong answer given confidently. What damages credibility is not the absence of an answer but the pretence of having one. Most experienced decision-makers have significantly more patience for honest uncertainty than for confident inaccuracy.

The Winning Edge

Weekly executive communication insight — every Thursday

Practical, no-filler analysis of Q&A strategy, board presentation technique, and executive communication — from 25 years of experience in high-stakes business settings.

About the Author

Mary Beth Hazeldine — Owner & Managing Director, Winning Presentations

With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, Mary Beth advises executives across financial services, healthcare, technology, and government on structuring presentations and managing the Q&A dynamics that determine whether decisions are made or deferred.