A stakeholder change presentation is the moment where leadership credibility is either built or broken. The restructuring decision has already been made. What remains is whether the people affected trust the reasoning, understand the timeline, and believe the leadership team is acting with integrity. Here’s how to structure the communication that preserves trust.

Dimitri had been given seventy-two hours to prepare the restructuring announcement. The pharmaceutical division he led was merging two research units into one, eliminating fourteen roles and creating nine new ones. His instinct was to lead with the strategic rationale—market pressures, patent cliff, the need to consolidate pipeline investment. His head of HR stopped him. “They won’t hear the strategy,” she said. “They’ll hear ‘fourteen people are losing their jobs.’ Start there.” Dimitri rewrote the entire presentation overnight. He opened by acknowledging the human cost directly, naming the support provisions before explaining the structural logic. He held separate thirty-minute sessions with each affected team rather than one all-hands announcement. The feedback afterwards was not “we agree with the decision”—it was “we understand why, and we trust the process.” Three months later, the merged unit was outperforming both predecessor teams. The people who stayed attributed it to how Dimitri handled the first conversation.

Preparing a restructuring communication? The Executive Slide System includes templates and frameworks for high-stakes organisational communications that maintain stakeholder confidence.

Jump to section:

- Why the Human Cost Must Come Before the Strategy

- Audience Segmentation: One Message Does Not Fit All Stakeholders

- Framing the Strategic Rationale Without Corporate Jargon

- The Timeline Slide: Certainty Where Possible, Honesty Where Not

- Preparing for the Questions You Hope Nobody Asks

- After the Presentation: Follow-Through That Rebuilds Trust

Why the Human Cost Must Come Before the Strategy

The most common error in stakeholder change presentations is leading with the strategic rationale. Market conditions have shifted. The competitive landscape demands a response. The organisation must evolve. All of this may be true, and none of it matters to the person sitting in the audience wondering whether they still have a job next month.

When people are anxious—and restructuring announcements generate acute anxiety—their cognitive processing narrows to a single question: “What does this mean for me?” Until that question is addressed, everything else is noise. The strategic rationale, the market analysis, the competitive pressures—none of it registers until the listener’s personal uncertainty is acknowledged.

Open with three things in this exact order. First, a direct acknowledgement that this announcement affects people’s lives and livelihoods. Not corporate-speak—plain language. “I know this is difficult. Some of you will be directly affected by these changes, and I want to address that before I explain the reasoning.” Second, the specific support provisions: redundancy terms, redeployment opportunities, career transition support, timelines for individual conversations. Third, and only third, the strategic context that explains why this restructuring is happening.

This ordering is counterintuitive for executives who think strategically. It feels as though you’re leading with bad news rather than building a logical case. That’s precisely the point. Stakeholders experiencing change don’t process logic until their emotional response has been acknowledged. Research in organisational psychology consistently shows that perceived procedural fairness—how the change is communicated and implemented—matters more to long-term trust than the change itself. Your stakeholder change presentation sets the perception of fairness from the opening sentence.

Communicate Change With Clarity and Credibility

The Executive Slide System gives you restructuring communication templates and decision frameworks—so your stakeholder presentation maintains trust whilst delivering difficult messages with precision.

- ✓ Board-ready templates for organisational change scenarios

- ✓ AI prompt cards to structure sensitive communications fast

- ✓ Framework guides for high-stakes leadership presentations

Get the Executive Slide System → £39

Designed for executives preparing high-stakes presentations

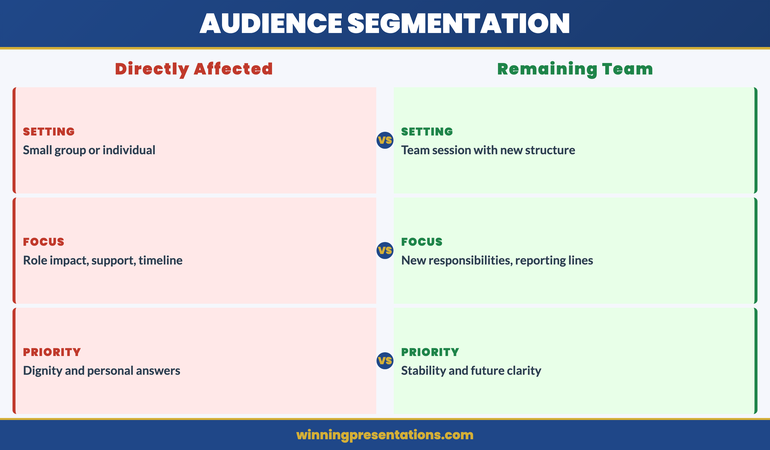

Audience Segmentation: One Message Does Not Fit All Stakeholders

A restructuring affects multiple audiences, each with different concerns, different information needs, and different levels of vulnerability. Presenting the same message to all of them—a single all-hands announcement—is efficient and almost always damaging. The people being made redundant, the people staying in restructured roles, the people unaffected but watching, the leadership team responsible for implementation, and the external stakeholders (clients, investors, partners) all need different communications.

For the directly affected group, the presentation must be personal, specific, and delivered in a small-group or individual setting. They need to hear what is happening to their role, what the timeline is, what support is available, and who their point of contact will be for questions. A large-audience announcement denies them the dignity of a personal conversation and creates a public spectacle of private distress.

For the people remaining in restructured roles, the presentation focuses on what changes for them: new reporting lines, new responsibilities, revised team structures, and the timeline for stabilisation. Their primary anxiety is not about redundancy—it’s about whether the organisation they’re staying in will function well enough to justify staying. Address that directly.

For the broader organisation—the people not directly affected—the presentation must explain why the restructuring happened, what the organisation looks like afterwards, and what it means for them operationally. Their anxiety is lower but their cynicism is often higher: they’re watching how leadership treats the affected colleagues, and that observation shapes their long-term trust. If you’ve read our guide on restructuring presentations and team trust, you’ll recognise the critical role that visible fairness plays in organisational recovery.

Framing the Strategic Rationale Without Corporate Jargon

Once the human cost is acknowledged and the support provisions are clear, the strategic rationale must follow. But the language matters enormously. Corporate jargon in a restructuring announcement—“right-sizing,” “synergy realisation,” “operational efficiency”—reads as evasion. It signals that the leadership team is hiding behind terminology rather than being direct about what’s happening and why.

The rationale should be expressed in three plain sentences. Sentence one: what has changed in the market or the organisation that made this restructuring necessary. Sentence two: what the restructured organisation will look like and why that structure is better positioned. Sentence three: what the leadership team has already done to minimise the impact on people. Three sentences. If you can’t explain the rationale in three sentences, you either don’t understand it fully or you’re trying to obscure something.

Avoid two common traps. The first is over-explaining—providing so much market context and competitive analysis that the rationale gets lost in data. Stakeholders experiencing change don’t need an MBA case study. They need to understand the logic simply enough to explain it to their families. The second trap is euphemism. Don’t say “we’re creating a more agile organisation” when you mean “we’re removing a layer of management.” Don’t say “some roles will be impacted” when you mean “fourteen people will be made redundant.” Direct language hurts in the moment but builds trust over time.

The most effective restructuring communicators—and Dimitri’s approach illustrates this—treat the rationale as context for a decision that’s already been made, not as justification for it. There’s a difference. Justification implies the leadership team is seeking approval from the audience. Context implies they’ve made a difficult decision and they’re explaining their reasoning honestly. Stakeholders respect the latter even when they disagree with the outcome.

The Timeline Slide: Certainty Where Possible, Honesty Where Not

After a restructuring announcement, the single most destructive force is uncertainty about timing. People can absorb bad news. They cannot absorb indefinite ambiguity. The timeline slide in your stakeholder change presentation must be as specific as possible about dates, and completely honest about what isn’t yet decided.

Structure the timeline in three phases. Phase one: what happens this week. Individual consultation meetings scheduled, support resources activated, FAQ document distributed. Phase two: what happens over the next thirty days. Consultation period, role confirmation for restructured positions, redeployment opportunities communicated. Phase three: what happens by ninety days. New structure operational, integration milestones, first review checkpoint.

For elements where dates are genuinely uncertain—regulatory approvals, union consultation outcomes, client contract negotiations—say so explicitly. “We expect this to be resolved by mid-May, but we’ll confirm the date by the end of next week” is far better than a vague “in due course.” Ambiguity in timelines is interpreted as either incompetence or concealment, regardless of the actual reason.

One detail that many leaders overlook: commit to a specific communication rhythm after the announcement. “I will send an update email every Friday until the restructuring is complete.” This single commitment reduces anxiety disproportionately, because it assures people that silence is not abandonment. The announcement presentation is the beginning of the communication, not the entirety of it. Our guide on how leaders can use redundancy announcement presentations covers the specific language and sequencing that preserves dignity during the most difficult conversations.

If you’re structuring a change communication for the first time, the Executive Slide System provides the structural templates that ensure every stakeholder audience receives the right message at the right moment.

Preparing for the Questions You Hope Nobody Asks

In restructuring communications, the Q&A session is where trust is won or lost. The presentation itself is a controlled environment—you’ve chosen the words, the sequence, the framing. The questions that follow test whether the presentation was honest or merely polished.

Prepare for five categories of questions. The “why me” question: “How were the affected roles selected?” Your answer must reference objective criteria—not performance, not politics. Structural logic: “These roles existed to serve a function that the new structure addresses differently.” The “what next” question: “What happens if I don’t accept the redeployment offer?” Have the answer ready with specifics. The “trust” question: “How do we know there won’t be another round in six months?” Be honest: “I can’t guarantee that no further changes will ever be needed, but this restructuring is designed to be stable for [timeframe].” The “leadership accountability” question: “Are senior leaders being affected too?” If yes, say so specifically. If no, explain why—honestly. The “real reason” question: “Is this really about strategy, or is it about cutting costs?” Do not deflect. “Cost reduction is part of the rationale, yes. We need to operate within [budget/margin]. The structural changes also position us for [strategic goal]. Both are true.”

The questions you hope nobody asks are exactly the ones you must prepare for most thoroughly. If you’re visibly uncomfortable or evasive when they surface, every other message in your presentation unravels. Our guide on town hall presentations that rebuild trust covers the Q&A preparation framework in detail, including how to handle emotional responses without shutting them down.

After the Presentation: Follow-Through That Rebuilds Trust

The presentation is the beginning, not the end. What happens in the seventy-two hours after a restructuring announcement determines whether the trust you’ve worked to preserve actually survives. Three actions are non-negotiable.

Action 1: Individual conversations within 48 hours. Every affected person must have a private, face-to-face (or video) conversation with their direct manager or a senior leader within two working days. Not an email. Not a group session. A personal conversation where their specific situation is discussed, their questions are answered, and they are treated as an individual, not a headcount number.

Action 2: Written summary within 24 hours. Distribute a written document that captures everything said in the presentation. People under stress do not retain verbal information well. The written summary serves as a reference they can return to once the initial shock subsides. Include all support provisions, timelines, contact details, and the strategic rationale in plain language.

Action 3: Visible leadership presence. In the days following the announcement, the leadership team must be visibly present. Not hiding in offices. Not travelling. Walking the floor, eating in the canteen, being available for informal conversations. This is not about having more formal meetings. It’s about demonstrating that the leaders who made this decision are not detaching from its consequences.

Dimitri did all three. Within forty-eight hours, every affected team member had a private conversation. A written FAQ was distributed the same afternoon. Dimitri ate lunch in the main canteen every day for three weeks. Trust isn’t built by presentations. It’s built by what leaders do after the presentation ends.

Lead Through Change With Structured, Honest Communication

Restructuring requires precision in every slide and every word. The Executive Slide System gives you the communication frameworks, stakeholder templates, and scenario guides you need—for £39.

FAQ: Stakeholder Change Presentations

Should I announce a restructuring in one large meeting or multiple smaller sessions?

Multiple smaller sessions, segmented by audience. The directly affected group should hear the news in a small-group or individual setting before the wider organisation. This prevents the public spectacle of people learning their role is at risk in front of hundreds of colleagues. The broader all-hands session should follow within hours, not days—delays create a rumour vacuum that’s worse than the announcement itself. The key principle is that no stakeholder should learn about changes to their own role from someone outside their direct leadership chain.

How do I handle tears or emotional reactions during the presentation?

Do not rush past them, minimise them, or pretend they aren’t happening. Pause. Acknowledge the emotion directly: “This is a difficult conversation and your reaction is completely understandable.” Offer the person the option to continue or step out for a moment. Do not move to the next slide whilst someone is visibly distressed—it signals that the agenda matters more than the people. Have tissues, water, and a private space available. If the session is derailed by strong emotion, call a brief pause rather than pushing through. Emotional responses are not obstacles to the communication—they are part of it.

What if I don’t have all the answers at the time of the announcement?

Say so honestly, and commit to a specific date when you will have the answer. “I don’t have that information yet—we’re still working through the consultation process. I’ll have an answer by next Friday and will communicate it directly.” This is far better than guessing, hedging, or deflecting. Stakeholders during restructuring have finely calibrated sensors for evasion. An honest “I don’t know yet” followed by a specific commitment builds more trust than a vague reassurance that turns out to be inaccurate.

The Winning Edge

Weekly insights on executive presentations, slide strategy, and boardroom communication.

Leading through organisational change? Download the Executive Slide System checklist for a quick restructuring communication framework.

If your restructuring is driven by a merger or acquisition, our guide to mergers and acquisitions presentations covers the board-level deal presentation that typically precedes stakeholder communications.

About the author

Mary Beth Hazeldine, Owner & Managing Director, Winning Presentations. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds and approvals.