Quick Answer: You cannot predict every shareholder question at an AGM — but you can build a response framework that handles any question with composure. The most effective AGM presentations do two things well: they establish a clear narrative that pre-empts the most obvious concerns, and they give the presenting team a structured protocol for questions that fall outside the script. The slide deck gets you to the questions. The framework gets you through them.

Valentina was Director of Investor Relations at a London-listed insurance group. She had spent six weeks building the AGM presentation: clean slides, rehearsed remarks, every likely question mapped to a prepared answer. Then, three weeks before the meeting, an activist shareholder group published a public letter challenging the CEO’s long-term incentive structure. Everything she had prepared assumed a broadly cooperative room. None of it was built to absorb that kind of scrutiny.

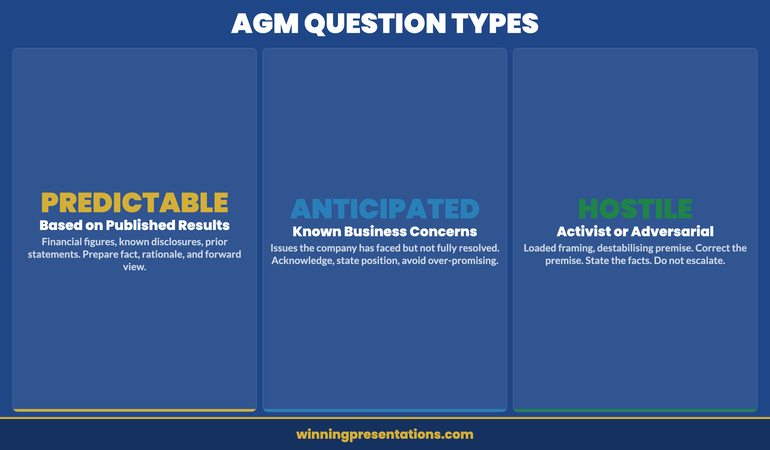

She did not rewrite the presentation. Instead, she spent two days working through every challenge the activist shareholders might plausibly raise — not scripting answers, but building a response framework for each concern: what the question assumes, what the factual position is, what the board’s stated rationale is, and how to close the answer without escalating. She categorised each question into three types: predictable, anticipated, and deliberately destabilising. Each type got its own response protocol.

On the day, three separate questions came directly from the activist group’s published agenda. She answered all three clearly, calmly, without notes. The Chair told her afterwards it was the strongest AGM she had seen run from an IR perspective in fifteen years.

What had changed was not the slide deck. The deck did its job — it got the meeting to the Q&A. The framework did the work that actually mattered. This article explains how to build both.

If your next high-stakes presentation is coming up soon

The Executive Slide System includes slide templates and scenario playbooks designed for board-level and investor-facing presentations — including the kind of high-scrutiny environments where the Q&A matters as much as the slides.

What Shareholders Actually Evaluate in an AGM

Most executives preparing AGM presentations focus almost entirely on the financial results and the strategic outlook. Both matter. But neither is what shareholders are primarily evaluating in the room.

What shareholders — particularly institutional shareholders and experienced retail investors — are actually assessing is whether the management team is credible, composed, and in command of their own narrative. The figures are already in the annual report. The slides largely confirm what shareholders already know. What cannot be read in a document is how the senior team handles the pressure of being questioned in public.

There are typically three audiences inside an AGM room. Institutional shareholders are analysing whether the governance narrative is coherent and whether management can defend its decisions under questioning. Activist shareholders or proxy advisers are looking for inconsistencies they can use to build a public challenge. Retail shareholders — often less financially sophisticated but no less engaged — want to feel heard and want reassurance that management understands their interests.

The mistake most AGM presentations make is addressing only the first group. The slides speak to institutional expectations: financial performance, forward guidance, governance disclosures. But the room also contains people who want a human response to their concerns — and the Q&A is where that either happens or it does not.

Understanding this three-audience dynamic changes what you put in your slides and how you prepare for questions. Your opening narrative should simultaneously signal competence (for institutional shareholders), acknowledge complexity (for those looking for weaknesses), and convey directness (for retail investors who want plain language). The board presentation 15-minute framework covers the same principles of narrative economy that apply here: less is more when your audience has already read the papers.

Executive Slide System

Build Presentations That Hold Up Under Shareholder Scrutiny

The Executive Slide System — £39, instant access — includes slide templates for board-level and investor-facing presentations, AI prompt cards for structuring your narrative, and scenario playbooks for high-scrutiny environments including AGMs, investor days, and governance reviews. Designed for presentations where credibility is being assessed alongside the content.

- Slide templates for board, governance, and investor-facing presentation scenarios

- AI prompt cards to structure your opening narrative and manage the framing

- Framework guides for building credibility in high-scrutiny presenting environments

- Scenario playbooks for meetings where the Q&A matters as much as the deck

Get the Executive Slide System →

Designed for executive presentations where the stakes require structural precision.

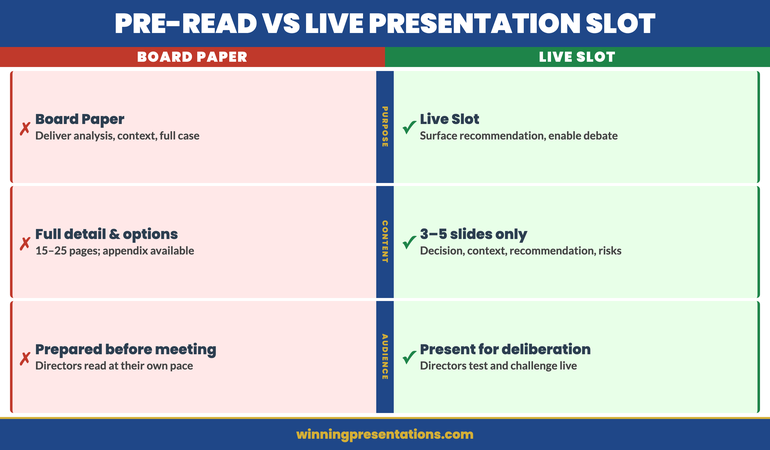

The AGM Presentation Structure That Creates Stability

An AGM presentation is not a results briefing. It is a governance event with a presentation embedded in it. That distinction matters for how you structure the slides.

Most AGM presentations follow a reporting sequence: financial results, operational highlights, strategic priorities, governance disclosures. This is appropriate. What tends to fail is the proportioning — too much time on the figures (which shareholders already have), not enough time on the narrative around decisions that were made or will be made.

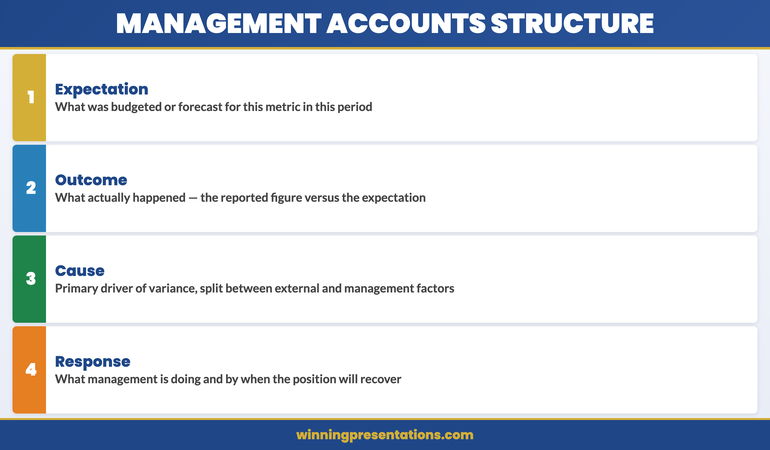

A stronger structure treats each section as a statement of accountability. Not just “here are the results” but “here is what we expected, here is what happened, here is why, and here is what we are doing as a result.” That four-part sequence — expectation, outcome, explanation, response — works for financial results, for governance decisions, and for any strategic change that requires explanation. It pre-empts the most obvious questions by answering them in the slides before the Q&A opens.

One structural addition that is consistently underused is what might be called an “open questions” slide near the end of the formal presentation. This slide briefly acknowledges two or three areas where management knows shareholders have questions — and states the company’s position on each. “We are aware that our capital allocation decisions have attracted comment. Our position is X.” This is not weakness. It signals confidence and depletes the most loaded questions before the room can ask them.

The formal presentation should run no longer than 20 minutes for a typical listed company AGM. Shareholders who have attended many of these meetings are attentive to brevity — it signals respect for their time and confidence in your material. For the structural principles behind executive brevity, the board strategy presentation framework offers a useful reference point on economy of narrative.

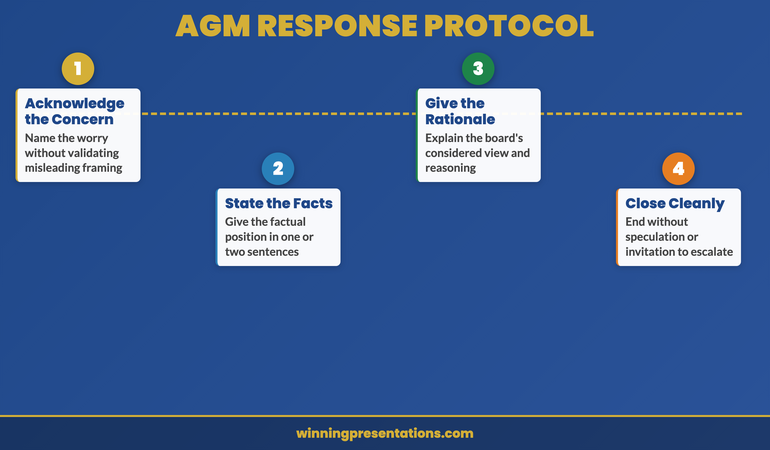

Building Your Q&A Response Framework

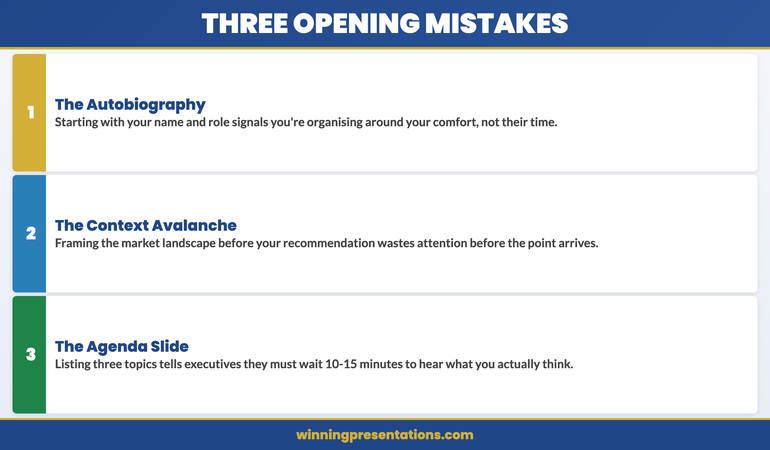

You cannot script every shareholder question. The attempt to do so is one of the most common mistakes in AGM preparation — executives spend hours writing word-for-word answers to 40 possible questions, then freeze when the 41st question arrives and the script doesn’t cover it.

A response framework is different from a script. Rather than writing specific answers, you build a decision protocol: given a question that falls into this category, here is how I respond structurally. The category, not the content, is what you prepare.

Three categories cover the majority of AGM questions. Predictable questions are based on published financial results, public disclosures, or statements the company has already made. For each predictable question, prepare a three-sentence answer: the factual position, the rationale behind the decision or outcome, and one forward-looking statement. Anticipated questions are based on issues you know the company has faced but may not have fully resolved — market position, management changes, regulatory matters. These require more careful handling; be factual, acknowledge the concern, and state the current position without over-promising. Hostile questions come with an agenda — from activist shareholders, from those with a specific grievance, or from those looking to destabilise the management team in a public forum.

For hostile questions, the framework is simpler than most executives expect. Acknowledge the concern without validating the framing. State the factual position. Close with the company’s considered position. Do not argue. Do not escalate. Do not speculate. The Q&A preparation principles in this briefing document framework apply directly to the AGM context: categorise before you prepare, and prepare the protocol before you prepare the content.

For executives building the slide architecture for investor-facing and governance presentations, the Executive Slide System includes scenario playbooks specifically designed for high-scrutiny presenting environments where the Q&A is as important as the deck itself.

When a Shareholder Goes Off-Script

Even the most thorough preparation will occasionally produce a question that sits outside your framework. The question is genuinely unexpected — a concern you had not anticipated, a detail from a subsidiary disclosure you had not mapped, or a question that is genuinely outside the scope of what the AGM is designed to address.

Off-script questions fall into three types, and each warrants a different response. The first is the out-of-scope question: a shareholder asks about a specific operational matter that is not germane to the AGM agenda. The appropriate response is direct: “That specific matter sits outside today’s agenda. I would ask that you contact our Investor Relations team directly, and we will ensure you receive a full written response within five business days.” This is not a deflection — it is a governance protocol, and most experienced shareholders accept it.

The second type is the genuinely unexpected question on a relevant topic where you do not have the precise detail to hand. Here, accuracy matters more than confidence. “I want to give you a precise answer on that. Rather than speculate, I would prefer to provide you with an accurate figure in writing by the end of the week.” This answer is far stronger than an approximate answer that turns out to be incorrect.

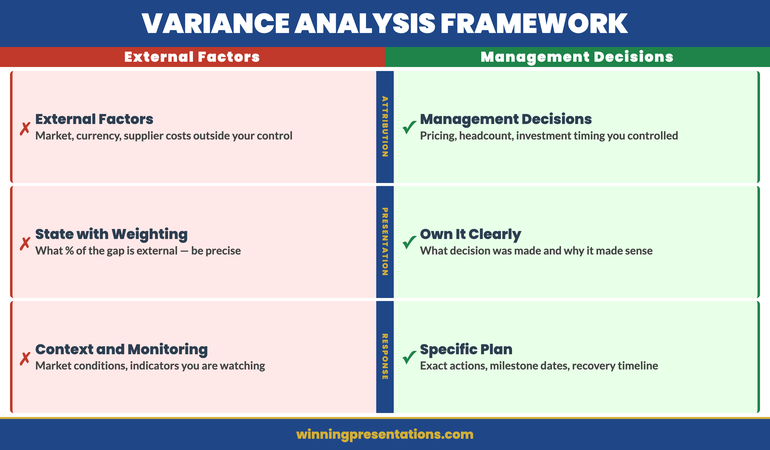

The third type is the deliberately destabilising question — one that uses a loaded framing or a misleading premise to put the management team on the defensive. The response here requires you to separate the premise from the concern. “I understand the concern about X. What I can tell you with confidence is Y. We are not in a position to speculate on [the destabilising element of the question], but the factual position on [the legitimate concern] is Z.” You are not accepting the framing. You are not ignoring the concern. You are addressing what is addressable. This connects to the response techniques covered in the management accounts presentation framework — how to handle questions where the framing itself is part of the challenge.

What to Do in the Silence Before You Answer

The seconds between a question being asked and your answer beginning are among the most scrutinised moments in an AGM. Shareholders are watching not just what you say but how you receive the question. A flinch, a glance at a colleague, a sharp breath — these micro-responses are read as signals of discomfort, and discomfort signals something to hide.

The most effective thing you can do in those seconds is nothing — at least, nothing visible. A deliberate pause of two to three seconds before you respond communicates consideration rather than hesitation. It signals that you are giving the question the weight it deserves, rather than reaching for the first answer that comes to mind. This is the opposite of how most executives experience that pause. They feel it as dangerous silence that needs to be filled. Shareholders tend to read it as composure.

What should be happening during those seconds is a rapid internal categorisation. Is this predictable, anticipated, or hostile? Which response protocol applies? That three-category framework reduces the cognitive load of answering under pressure — you are not constructing an answer from scratch, you are selecting the appropriate response structure and filling it in.

There is one phrase that buys time and sounds deliberate rather than evasive: “Let me be precise about this.” Used sparingly, it signals care. Used too often, it sounds like stalling. If you need longer to think — particularly for an off-script question — “I want to give you an accurate answer rather than an approximate one” is a stronger formulation than any version of “that’s a good question,” which no experienced shareholder finds reassuring.

The Closing Statement That Controls the Room’s Last Impression

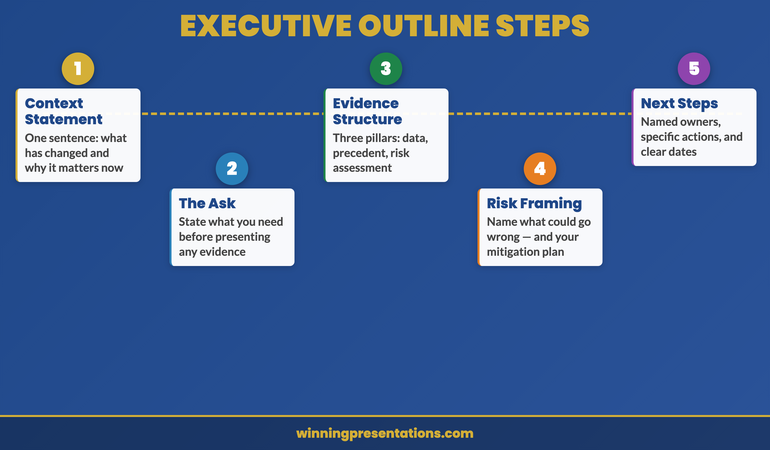

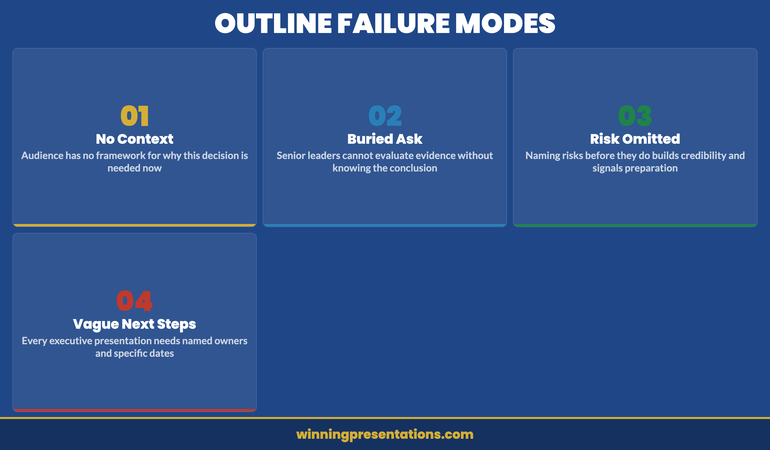

Most AGMs end poorly — not because anything went wrong, but because the close is not prepared. The chair says something like “and I think that concludes our questions for today,” and the meeting simply stops. Shareholders file out, and the last thing they remember is the final question, which may or may not have been an easy one.

A prepared closing statement is the most underinvested two minutes in AGM preparation. It does three things. First, it reaffirms the company’s strategic direction in one sentence — not a summary of the whole presentation, just the core message. “We remain committed to building long-term shareholder value through disciplined capital allocation and operational execution.” Second, it acknowledges any difficult issues raised in the Q&A — not relitigating them, but signalling that management has heard them. “We have heard the concerns about X, and we take those seriously.” Third, it thanks shareholders for their engagement with substance rather than politeness. Not “thank you for attending” but “your questions today reflect the kind of rigorous engagement that makes better companies.”

Two sentences on direction, one on difficult issues, two on shareholder engagement — six sentences that close the AGM on management’s terms rather than on whatever question happened to come last. The closing statement is the last thing shareholders remember. In the current environment, where AGM summaries circulate quickly through IR networks and financial media, it is also what shapes the first-day narrative in the press. Prepare it with the same precision you give to the opening.

Executive Slide System

The Structure Behind Every High-Stakes Executive Presentation

The Executive Slide System — £39, instant access — gives you slide templates, AI prompt cards, and framework guides for executive presentations where credibility and decision quality are evaluated simultaneously. AGMs, board strategy sessions, investor days — the scenarios where getting the structure right is not optional.

Get the Executive Slide System →

Designed for senior executives presenting in high-scrutiny environments.

Frequently Asked Questions

What should an AGM presentation include?

An AGM presentation should cover financial results in context (not just reported figures, but the narrative around them), operational highlights that connect to strategic priorities, governance disclosures including remuneration and board composition, and a forward-looking statement on strategic direction. A strong AGM presentation also includes an “open questions” slide that acknowledges known areas of shareholder concern and states the company’s position — this depletes the most loaded questions before the formal Q&A begins. The full presentation should run no longer than 20 minutes, leaving adequate time for substantive shareholder questions.

How long should an AGM presentation be?

For a typical listed company AGM, the formal presentation should run 15 to 20 minutes. Shareholders who attend AGMs regularly are attentive to brevity — going significantly over this signals poor preparation or excessive content. The Q&A is often where the meeting’s value lies for shareholders, and a long presentation risks compressing the time available for questions. If you have complex material to cover, the solution is a pre-read document circulated in advance, not a longer presentation on the day. Experienced IR teams treat the AGM as a conversation anchored by a concise presentation, not a presentation that happens to have a conversation attached.

How do you handle aggressive or hostile shareholder questions at an AGM?

Hostile AGM questions follow predictable patterns: they use loaded framing, they make assertions as premises, and they are designed to provoke a defensive response. The most effective protocol is to separate the premise from the legitimate concern. Acknowledge what is a real concern, state the factual position, give the company’s considered view, and close without speculating or engaging with the destabilising element of the question. Do not argue. Do not escalate. Do not accept a false premise by answering inside it. The goal is not to win the exchange — it is to give every other person in the room confidence that management is composed, factual, and in command of its own narrative. That is the shareholder relations outcome that matters most.

The Winning Edge

Weekly insights on executive presentations, delivered every Thursday. Practical frameworks, real scenarios, and no generic advice.

Free resource: Download the Executive Presentation Checklist — a one-page pre-presentation review for high-stakes executive meetings.

About the Author

Mary Beth Hazeldine — Owner & Managing Director, Winning Presentations

With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, Mary Beth Hazeldine advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds and approvals. She works directly with senior leaders to build the presentation architecture that gets decisions made. Learn more at Winning Presentations.