What I Watched Forty Senior Candidates Do in a Final-Round Presentation

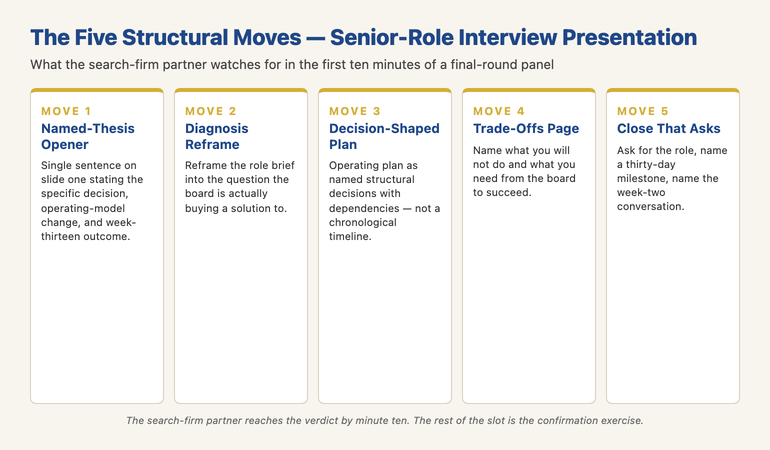

Quick answer: The interview presentation senior roles candidates win is built on five structural moves the search firm partner watches for in the first ten minutes: (1) a named-thesis opener that states what the candidate will do in the first hundred days, not what the candidate has done in the past; (2) a diagnosis slide that reframes the brief into the problem the board is actually buying a solution to; (3) a decision-shaped operating plan, not a phased timeline; (4) a candid risks-and-trade-offs page that names what the candidate will not do, and what they will need from the board to succeed; (5) a close that asks for the role, names a thirty-day milestone, and tells the panel what conversation the candidate wants to have in week two. The candidates who run those five moves get the offer. The candidates who walk the panel through their CV in slide form get the courtesy interview and the call from the search firm three days later that begins “the panel really enjoyed meeting you, but…”. Polish is not the differentiator at this level. Structural decisions on the first three slides are.

JUMP TO:

- Why the forty-five-minute format is structured the way it is

- Move one: the named-thesis opener for the first hundred days

- Move two: the diagnosis slide that reframes the brief

- Move three: a decision-shaped operating plan, not a timeline

- Move four: the risks-and-trade-offs page that names what you will not do

- Move five: the close that asks for the role

- The pre-panel diagnostic to run on your first three slides

- The collapse pattern: chronological CV deck, vague hundred-day plan

- One thing to do before the next panel

- Frequently asked questions

In 2007, I sat in on a final-round panel for a divisional managing-director role at one of the European banks where I worked through the second half of my banking career. The panel comprised the group CEO, the divisional chairman, the head of HR, an external non-executive director from a peer institution, and the senior partner from the executive-search firm running the process. The candidate was a deeply credible internal-plus-external hybrid with two decades in the sector, a verifiable track record, and references from three other CEOs in the industry. He opened slide one with his CV in summary form. Slide two was an organisation chart of the teams he had run. Slide three was a sector overview the panel had themselves written into the role brief eight weeks earlier. The search-firm partner sat to my left, watching the chairman. The chairman closed his copy of the deck at slide three and did not open it again. The candidate continued through forty-two slides over thirty-one minutes. He was offered a courtesy second meeting. He did not get the role. The role went to a candidate the panel met the following week whose first slide read, “In my first hundred days, I will rebuild the divisional pricing committee, separate the retail and corporate P&L reporting, and hire a deputy from outside the bank.” That candidate spoke for twenty-six minutes. The chairman closed his deck at minute eleven and put it on the table beside him — the gesture senior panels use when they have already reached the verdict.

(This article was created with AI assistance; all stories and insights are based on 35 years of real client work.)

This piece walks through the five structural moves I have watched senior candidates make in final-round interview presentations across two decades — the ones that earn the offer and the ones that produce the courtesy call. The moves are not about polish. The credible candidates I watched were all polished; polish is the minimum entry condition at senior-role level, not the differentiator. The differentiator is what goes on the first three slides and how the close lands. Final-round panels at the divisional-MD, CFO, COO, and non-executive-director level have substantially the same shape across sectors, and the five moves transfer cleanly between them. The article covers each move, the pre-panel diagnostic the search-firm partners I worked alongside ran on every shortlist, the collapse pattern that produces most of the polite declines, and the one structural decision worth making the morning of the panel itself.

Before the next final-round panel, a one-page structural check on the first three slides is worth a look.

The Executive Presentation Checklist walks through the openings senior panels actually reward — the named-thesis slide one, the diagnosis-reframe slide two, the decision-shaped operating-plan slide three, and the close that asks for the role. Free download, no email gate.

Why the forty-five-minute format is structured the way it is

Most final-round panels for senior roles are scheduled into a forty-five-minute slot. The format has settled into a fairly consistent shape across the executive-search firms I worked alongside in banking, and the shape is structural for a reason that has nothing to do with arbitrary convention. The first twenty to twenty-five minutes are the candidate’s presentation. The next fifteen are the panel’s questions. The final five are the candidate’s opportunity to ask the panel the question they have actually come to ask. Behind that visible structure is the invisible structure the search-firm partner is running in their own head. They have allocated minute one through minute three to forming the verdict on whether the candidate has read the brief correctly. Minute four through minute ten is allocated to forming the verdict on whether the candidate’s operating plan is shaped like a board would want to fund it. Minute eleven onward is the confirmation exercise. The search-firm partner is not waiting until the Q&A to decide; they are testing their early verdict against the remaining content.

The candidate who understands the invisible structure builds the deck to land the verdict in the first three slides and uses the remaining slides to deepen, not to introduce. The candidate who misunderstands the structure builds the deck to introduce themselves on slides one through five and only arrives at the operating plan on slide twelve, by which point the chairman has reached a verdict on a structural absence. The verdict is not unkind. It is mechanical. The panel cannot fund what it has not been shown, and a candidate who has not put the operating plan on the table in the first ten minutes has not given the panel something to fund. The polished CV walk, however accurate and however impressively delivered, is not a thing the panel can fund. The hundred-day operating plan is.

The forty-five-minute slot also has a polite social structure the candidates I watched fail consistently misread. The panel will sit through the full slot regardless of when they reach the verdict. They will ask cordial questions in the Q&A window. They will thank the candidate warmly. The search-firm partner will walk the candidate out and shake their hand at the lift. None of those gestures carry information about the verdict. The verdict has been reached, and the social structure is engineered to disguise it so that the candidate’s reputation in the market is protected regardless of the outcome. The candidate who walks out believing the meeting went well, on the strength of the panel’s cordiality, is the candidate who gets the polite three-day-later call. The board-of-directors presentation structure that earns the room’s tolerance covers the equivalent dynamic at the board level, where the cordiality runs even higher and the verdict has typically been reached even earlier.

Move one: the named-thesis opener for the first hundred days

The first move is the named-thesis opener. Slide one names what the candidate will do in the first hundred days of the role, in a single sentence that the chairman could repeat to a peer in the corridor afterwards. The sentence has three parts: the specific decision the candidate will take that is currently not being taken, the specific change to the operating model that decision will require, and the specific outcome the board will see in week thirteen. “In my first hundred days, I will rebuild the divisional pricing committee, separate the retail and corporate P&L reporting, and hire a deputy from outside the bank” passes the test. “I bring twenty-two years of relevant experience across European banking and a track record of delivering shareholder value” does not. The first sentence names commitments; the second names credentials. Panels at this level have already verified credentials — that is what the references were for. They are testing for commitments.

The most common failure mode is the qualification opener. “Thank you to the chairman and the panel for the opportunity to be here today; I’d like to walk you through my thinking on the role and how I see the next chapter for the division…” The sentence is what most candidates feel comfortable opening with. It is also the sentence that has lost the room by the end of it. The chairman has heard the equivalent sentence in seven of the last seven shortlists for similar roles, and the sameness of it tells them the candidate has not done the work to know what they are actually proposing. The named-thesis opener feels more exposed to deliver, which is why most candidates do not deliver it. The exposure is the signal the panel is looking for. The candidate who is willing to put the hundred-day commitment on the table on slide one is signalling they have done the work to know what the commitment is. The candidate who softens the opener is signalling the opposite, accurately, whether they intend to or not.

The discipline is the courage to write the sentence and not soften it. The instinct to soften comes from the candidate’s spouse, the candidate’s mentor, the search-firm consultant’s rehearsal feedback, and the candidate’s own caution about appearing presumptuous. Each of those voices is well-intentioned and each of them is, at this stage of the process, wrong. The panel has shortlisted the candidate because they are not presumptuous to be there. The shortlist has done that work. The slide-one decision is not whether the candidate deserves the role; that is settled. The slide-one decision is whether the candidate has formed a view of the role specific enough for the panel to interrogate. The named-thesis opener does that work. The soft opener leaves the work undone, and the panel reads the absence accurately.

Move two: the diagnosis slide that reframes the brief

The second move is the diagnosis slide. Slide two reframes the role brief into the problem the board is actually buying a solution to, which is almost always a different problem from the one in the formal job description. The formal job description is written by the HR function in consultation with the outgoing incumbent or the chairman’s office; it captures the visible scope of the role. The actual problem the board is hiring against is the conversation the board has been having in its own sessions over the previous six to twelve months — the one that produced the decision to make the hire in the first place. The candidate’s job on slide two is to demonstrate they have read both the formal brief and the actual conversation, and that they can distinguish between the two without making the panel uncomfortable. The signal the panel is reading on slide two is not whether the diagnosis is right; it is whether the candidate has done the listening to know what the board has actually been worrying about.

The diagnosis is built from three sources that all senior candidates have access to: the role brief and accompanying documents the search firm provided; the public materials the company has produced in the previous twelve months, particularly the annual report’s strategic-priorities section and any analyst-day transcripts; and the listening the candidate did in the preliminary conversations with the chairman, the search-firm partner, and any current board members the candidate met as part of the process. The synthesis of those three sources, written in two or three sentences in the board’s own vocabulary, is what goes on slide two. The candidates who get this slide right typically open it with a sentence beginning, “Behind the role brief is a question this board has been working through, which is…” The candidates who get it wrong open with a sentence beginning, “The role is, as described in the brief…” and read back the description the panel themselves wrote. The first sentence earns the chairman’s attention. The second sentence loses it.

The hardest part of slide two is the willingness to put a diagnosis on the table that might be partially wrong. The instinct is to keep the diagnosis general enough that it cannot be wrong. The general diagnosis is also general enough that it cannot be useful. The panel is interrogating the specific. “Behind the brief is a question about whether the divisional structure put in place in 2019 is the right one for the European footprint after the consolidation announcements of last year” can be wrong. It can also be exactly right. The candidate who puts it on the table is signalling they are willing to be wrong about specific things, which the panel reads as the willingness they want in the role. The candidate who avoids the specific signals the opposite. The executive buy-in presentation framework covers the broader application of this discipline across senior-approval contexts where the proposer has to put a specific reading of the room on the table before the room has confirmed they are open to it.

Move three: a decision-shaped operating plan, not a timeline

The third move is the operating-plan slide. The plan is decision-shaped, not timeline-shaped. A decision-shaped plan lists, in priority order, the specific structural decisions the candidate will take in the first hundred days, the specific dependencies each decision has on people, capital, and external relationships, and the specific signal the board will see in week thirteen that the decision was taken correctly. A timeline-shaped plan lists, in chronological order, the activities the candidate will undertake in weeks one to four, weeks five to eight, weeks nine to twelve, and week thirteen onward. The decision-shaped plan is what the board can fund and govern against; the timeline-shaped plan is the diary the candidate has constructed for themselves. Panels at this level fund decisions, not diaries.

The first three slides of a senior-role panel deck do nine-tenths of the work — and they are the slides most candidates spend the least time building.

The Executive Slide System is the slide library senior candidates use to build the named-thesis opener, the diagnosis-reframe slide two, the decision-shaped operating-plan slide three, and the close that asks for the role — without rebuilding them from scratch for every panel. 26 Executive Templates, 93 AI Prompts, 16 Scenario Playbooks, Master Checklist, Framework Reference. Built on 24 years in corporate banking and 16 years coaching senior professionals across financial services, insurance, consulting, and technology. Instant download, lifetime access.

- 26 Executive Templates — for the named-thesis opener, the diagnosis slide, the decision-shaped operating plan, and the asks-for-the-role close

- 93 AI Prompts — for the language work on slide one and slide two where most candidates spend their hardest hour

- 16 Scenario Playbooks — covering final-round panels, board-interview panels, internal-pitch panels, and the variants between them

- Master Checklist — the pre-panel diagnostic to run on the first three slides the morning of the panel

- Framework Reference — the structural moves the search-firm partners I worked alongside watched for, written up as a permanent reference

- Instant download, lifetime access — £39

The operating plan’s decisions live at the structural level rather than the activity level. Examples of decision-shaped items: “Decision one — collapse the two separate pricing committees into a single weekly forum, chaired by the deputy hired in week six, with a standing item on cross-divisional pricing tension. Dependency: deputy hire signed by week four. Week-thirteen signal: the four divisional heads attend the weekly forum without exception in the four weeks following the hire.” Examples of timeline-shaped items the operating plan must avoid: “Weeks one to four: meet all direct reports, review the operating model, attend the first board meeting, develop the hundred-day plan…” The timeline version describes what the candidate will be doing; it does not describe what the candidate will be deciding. Senior panels are interested in the deciding, not the doing.

The decision-shaped plan also signals what the candidate will not be doing in the first hundred days, by omission. The candidate who lists four structural decisions for the hundred-day window is implicitly signalling that everything else is out of scope for the window. The panel reads the signal as discipline. The candidate whose timeline lists fourteen items is signalling that none of them is the priority, and the panel reads that signal as the absence of one. Search-firm partners I worked alongside told me consistently that the single most reliable predictor of a successful senior hire was the candidate’s ability to name what they would not do in the first hundred days, not what they would. The decision-shaped operating-plan slide is where that signal lives.

Move four: the risks-and-trade-offs page that names what you will not do

The fourth move is the risks-and-trade-offs page. The page names two things the candidate is willing to put on the table that most candidates avoid. The first is what the candidate will explicitly not be doing in the first hundred days that some board members might expect them to do — the strategic initiatives, the personnel reshuffles, the operating-model changes the candidate has consciously deferred to year two. The second is what the candidate will need from the board to make the first hundred days work — the air cover on a specific decision, the budget envelope for the deputy hire, the introduction to two specific external relationships, the latitude to make a particular call without referring back. The candidate who puts both on the page passes the panel’s test of self-awareness; the candidate who hedges either reads as either over-promising or under-prepared.

The naming of what the candidate will not do is uncomfortable because it invites the panel to push back on the deferrals. The push-back is exactly what the panel wants to do, and the candidate who has thought through the deferrals is in a position to defend them; the candidate who has not is in a position to backtrack. The backtrack is what loses the room. A panel will tolerate a deferred priority that the candidate can defend; a panel will not tolerate a candidate who lists a deferred priority and then, under questioning, agrees to bring it forward. The agreement reads as the candidate having no real conviction about the deferral, which reads as the candidate having no real conviction about the priorities they did name. The discipline is to write the deferrals down, defend them under questioning, and only revise them if the panel surfaces information the candidate did not have. The 3Ps framework for executive presentation coaching covers the rehearsal work that prepares the candidate to defend the deferrals in the room, which is the work that distinguishes a candidate who survives the panel’s pressure from one who collapses under it.

The naming of what the candidate will need from the board is similarly uncomfortable. The instinct is to present as self-sufficient. The signal the panel is reading is the opposite. They want to know what the partnership with the candidate looks like in practice, which means they want to know what the candidate will ask of them in the first hundred days. A candidate who asks for nothing is signalling either that they do not yet know enough about the role to ask, or that they are unwilling to engage the board as a working partnership. Neither signal helps. A candidate who asks for three specific items — air cover on the deputy hire, an introduction to the two largest customers within the first month, the latitude to defer a specific committee for ninety days — is signalling they have already thought about the working relationship and the board reads that as the relationship they want.

Move five: the close that asks for the role

The fifth move is the close. The close asks for the role, names a thirty-day milestone, and tells the panel what conversation the candidate wants to have in week two. The asking-for-the-role part is the part most candidates skip, and the skip is one of the most reliably negative signals senior panels read. “Thank you for your time, I’d welcome any questions” is the standard close, and it carries no information about whether the candidate actually wants the role. “I want this role, and if you offer it to me my first call on day one is to the head of operations to schedule the pricing-committee restructure for week six; I’d like to have the conversation about the deputy hire with the chairman in week two” carries all the information. The close is not the place to be modest. The candidates who close modestly are the candidates who get the courtesy call. The candidates who close with the explicit ask, the named day-one action, and the named week-two conversation are the candidates who get the offer.

The thirty-day milestone is the second part of the close. It tells the panel what the board will see in the first month that signals the candidate is in the role rather than merely in possession of it. Useful milestones at this level: the announcement of a specific committee restructure; the signing of a specific external relationship; the first board paper on a specific topic the candidate has put on the agenda for the first board meeting in the role. Less useful milestones: the meeting cadence with direct reports, the publication of a values statement, the announcement of a strategy review. The board is looking for milestones that have content, not process. The candidates I watched who named content milestones in the close were the candidates who got the offer. The candidates who named process milestones got the polite second meeting.

The pre-panel diagnostic to run on your first three slides

The diagnostic is mechanical. Print slides one, two, and three of the deck the morning of the panel. Hand them to a colleague who has not been part of the preparation — a former boss, a peer from outside the sector, a long-tenured chief of staff. Ask three questions. Question one: from slide one alone, can you tell me what I am committing to do in the first hundred days, in one sentence? If the answer is yes and the sentence matches what is on the slide, slide one is doing its work. If the answer is no, or the sentence reconstructed is general where the slide should be specific, rewrite slide one. Question two: from slide two, can you tell me what problem you think the board is actually trying to solve, distinct from the visible role brief? If the answer comes back as a paraphrase of the role description, slide two has not yet been written; rewrite it. Question three: from slide three, can you name two decisions I am committing to take in the first hundred days, with their dependencies? If two decisions and their dependencies do not come back, slide three is still in timeline form rather than decision form; rewrite it.

For senior candidates with a final-round panel approaching, the structural method behind the five moves is worth investing in.

The Executive Buy-In Presentation System is the self-paced programme senior professionals use to build the structural method behind the five-move panel deck — the named-thesis opener, the diagnosis reframe, the decision-shaped operating plan, the trade-offs page, and the close that asks for the role. Self-paced programme with monthly cohort enrolment, 7 modules, no deadlines, no mandatory session attendance, optional live Q&A sessions fully recorded. Lifetime access to materials. £499.

The diagnostic takes thirty to forty-five minutes and surfaces, on average, two of the three slides as still needing structural work. The candidates I watched who ran the diagnostic the morning of the panel walked in with three slides that passed. The candidates who skipped it walked in with three slides that mostly passed, which at this level is the same as three slides that did not pass. The diagnostic is mechanical specifically because the candidate’s own judgement is unreliable about their own slides at this stage; they are too close to the content to read it as the chairman will read it. A colleague’s thirty-minute pass-run substitutes for the missing distance. It is the highest-leverage half-hour in the entire preparation cycle.

The collapse pattern: chronological CV deck, vague hundred-day plan

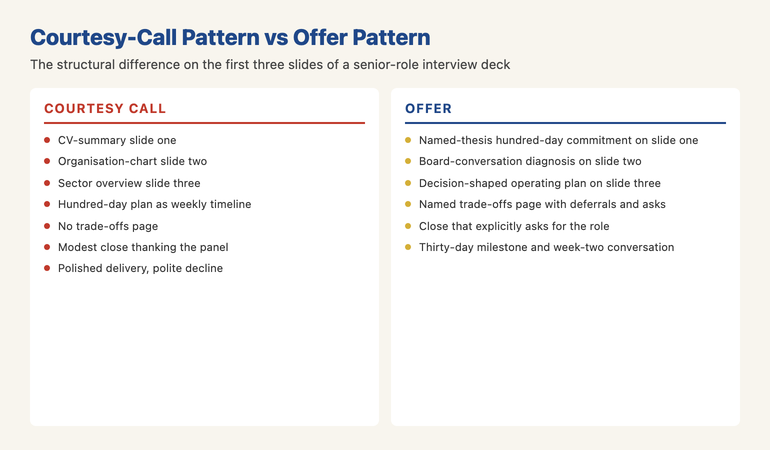

The collapse pattern has four stages and produces most of the polite declines I watched at senior-role panels. Stage one: the candidate opens with their CV in summary form, either as a literal CV slide or as a thinly-disguised “about me” opener that summarises their career rather than naming a hundred-day thesis. The panel registers the absence of a thesis in the first ninety seconds. Stage two: slides two and three describe the candidate’s prior roles, often with quantitative achievements, on the implicit logic that the panel needs to know about the candidate’s track record. The panel already knows about the track record; the search firm verified it before the shortlist. The slides are not adding information; they are using the candidate’s minutes in front of the panel to confirm what the panel already knew. The verdict is solidifying.

Stage three: the operating plan, when it eventually arrives on slide eight or nine, is presented as a timeline of weekly or monthly activities rather than as a decision-shaped commitment to specific structural moves. The panel reads the timeline as the candidate’s personal diary rather than as an operating plan the board can govern against. The chairman closes the deck. Stage four: the close thanks the panel, expresses enthusiasm for the opportunity, and invites questions. The panel asks two or three cordial questions, the chairman thanks the candidate, the search-firm partner walks the candidate to the lift, and the candidate leaves the building believing the session went well. The polite call comes three days later. The candidate, often, does not understand why; they had been polished, well-prepared, and credentialed. The polish, preparation, and credentials were not the issue. The first three slides were the issue, and the first three slides had nothing on them that the panel could fund.

The candidates who get the offer trained the structural method into the deck before walking into the panel — not on the day.

The Executive Slide System ships the templates, prompts, and playbooks the five-move panel deck depends on. 26 Executive Templates, 93 AI Prompts, 16 Scenario Playbooks. Built on 24 years in corporate banking and 16 years coaching senior professionals through final-round panels. Instant download, lifetime access. £39.

One thing to do before the next panel

Write the named-thesis opener for slide one in a single sentence the morning of the panel, and read it aloud to a colleague who has not seen any of the preparation. If the colleague can repeat the sentence back to you, in their own words, with the three components intact — the specific decision you will take, the specific change to the operating model, the specific outcome the board will see in week thirteen — slide one is doing its work. If the sentence comes back as a paraphrase of your credentials or a general statement about leadership style, the sentence on the slide is not yet right. Rewrite it before you walk in. The discipline of the named-thesis opener is the discipline that distinguishes the offer candidate from the courtesy-call candidate, and the courage to write the sentence is more important than the polish to deliver it. The panel is reading for evidence that you have done the work to know what you are committing to. Slide one is where they look first.

Frequently asked questions

Is the five-move structure appropriate for an internal candidate as well as an external one?

Yes, and arguably more so. Internal candidates often misread the panel’s expectations because they assume their internal knowledge is the differentiator; it is not, because the panel already knows the candidate is internally credentialed. The differentiator is whether the internal candidate has formed a view of the role that the panel had not already heard them articulate in their current capacity. The named-thesis opener and the diagnosis-reframe slide are particularly important for internal candidates, because they signal the candidate is bringing a new perspective rather than a continuation of their current one. Internal candidates who walk into the panel and present a polished version of what the panel has already heard them say in committee for two years are the candidates who get passed over for an external hire. Internal candidates who walk in with a hundred-day commitment that surprises the chairman, in a productive way, are the candidates who get the role.

How long should the actual presentation portion be within the forty-five-minute slot?

Twenty to twenty-five minutes is the working range. The shorter end of the range is generally better, because it leaves more time for the panel’s questions, which is the part of the slot the candidate has the most control over once it begins. Candidates who present for thirty-five minutes are signalling either that they could not edit the deck or that they do not trust themselves to handle Q&A; both are negative signals. The discipline of editing the deck down to twenty minutes is the discipline of deciding what is structural versus what is supporting. The structural material goes in the deck; the supporting material goes in the appendix the candidate can pull from in Q&A. The candidate who is comfortable presenting for twenty minutes and then engaging on whatever the panel wants to engage on is the candidate who reads as in command of the material.

What if the search firm has been explicit that the panel does not want a hundred-day plan?

The search firm’s guidance is worth taking seriously, but in twenty years of watching final-round panels the guidance “they don’t want a hundred-day plan” almost never means what it sounds like. It usually means “they don’t want a generic hundred-day plan that reads like every other candidate’s.” A candidate who responds to that guidance by removing the operating plan and presenting their career narrative instead is solving the wrong problem; the guidance was a warning against generic, not against operating plans. The right response is to build the decision-shaped operating plan the panel can actually fund — specific, named, and dependent on identifiable factors — and to present it as a working hypothesis open to the panel’s revision rather than as a fixed commitment. The named-thesis opener still applies; the operating-plan slide still applies; the close still applies. What changes is the framing around the operating plan, not the existence of it.

How should the close handle the question of salary, package, or terms?

Not at all, in the close itself. The close is the place to ask for the role and to name the thirty-day milestone. The negotiation conversation belongs in a separate session with the chairman or the search-firm partner, not in the final-round panel. Candidates who introduce package questions in the panel signal that they are evaluating the role as a transaction rather than as an operating commitment; senior panels read the signal accurately and find it disqualifying. The principled position is to make the panel choose the candidate first and to negotiate the terms second. The candidates who get the offer are the ones who close on the role, accept the offer in principle pending the package conversation, and have the package conversation in the following week. The candidates who negotiate in the panel are usually the candidates who are no longer choosing.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly (Thursday) newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate proposals senior committees and panels approve from proposals they defer. Subscribe to The Winning Edge →

For the broader picture across slides, storytelling, confidence, and delivery, the seven-product Complete Presenter library is the bundle most senior professionals find useful as a single resource — £99 for everything, lifetime access.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises senior professionals across financial services, insurance, consulting, and technology on the structural moves that distinguish final-round candidates who receive the offer from candidates who receive the courtesy call.