In this article:

- What Executive Influence Actually Is (And What It Isn’t)

- Why Online Training Beats In-Person for Senior Professionals

- What Genuine Executive Influence Training Covers

- Stakeholder Mapping: The Discipline Most Programmes Skip

- Building Credibility Before You Need to Use It

- How the Executive Buy-In System Teaches Influence

- Frequently Asked Questions

Soraya Hashemi had been appointed Chief Commercial Officer at a FTSE 250 industrial group six weeks earlier, recruited from a competitor where she had spent fourteen years. On paper, the brief was straightforward: reset the commercial strategy and take three material investment cases to the board over her first twelve months. In practice, she discovered something no recruiter mentions at offer stage. The board that hired her was not the board she now had to influence.

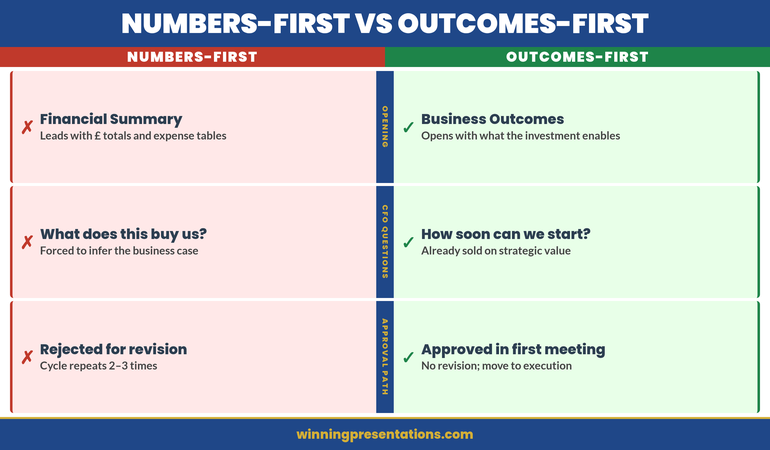

Her first presentation was a pricing realignment case worth £48 million in projected margin recovery. The content was unimpeachable — she had built the same type of case four times at her previous organisation, each one approved within a single meeting. This time, the non-executive chair asked a procedural question she had not anticipated, the senior independent director raised a cultural concern about customer disruption, and a newly appointed director — an ex-regulator — probed the risk framework for thirty minutes. The case was deferred. Not rejected. Deferred pending further analysis.

The second presentation, two months later, was the same pattern in a different suit. Strong content. Weak buy-in. She left the meeting with another round of work, another deferral, and a creeping sense that the board did not yet trust her judgement at the level they trusted her predecessor’s.

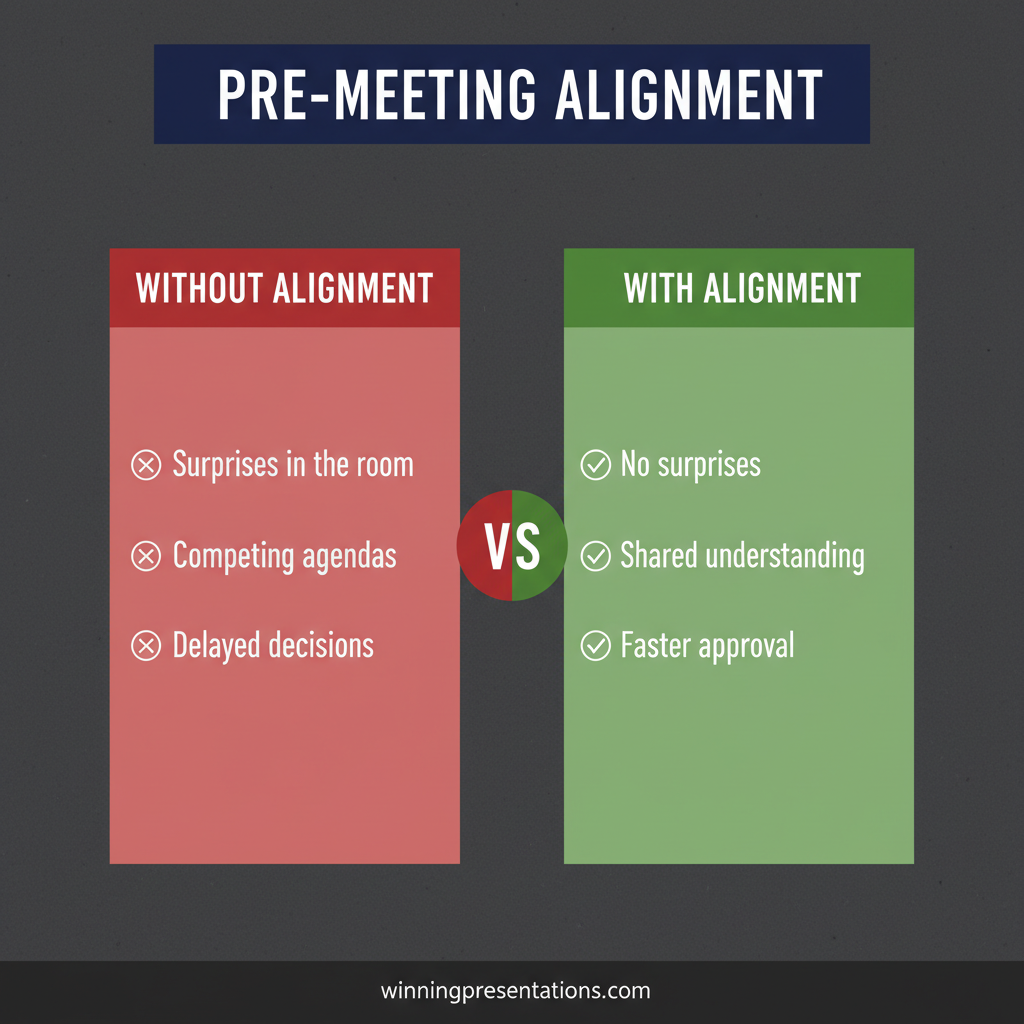

What changed was not the quality of her analysis. What changed was that Soraya stopped presenting information and started engineering consensus. Before the third case, she spent three weeks having individual conversations with every board member — not selling the case, but understanding what each director was worried about, what past experiences shaped their instincts, and what evidence they would need to move from scepticism to support. By the time she presented, every objection she heard in the room had already been surfaced, absorbed, and addressed. The case was approved in forty minutes. The chair called it the most composed board paper he had seen all year.

The difference between presentation one and presentation three was not confidence or delivery. It was a skill Soraya had never been explicitly taught — the skill of building influence before you enter the room.

If you want to develop this skill systematically, the Executive Buy-In Presentation System is a self-paced online programme that teaches the influence architecture senior professionals rarely learn on the job. Enrolment is open — join at your own pace.

What Executive Influence Actually Is (And What It Isn’t)

The phrase “executive influence” carries baggage. For many senior professionals, it evokes images of corporate politics, backroom dealing, or charisma-driven persuasion that feels uncomfortably close to manipulation. That framing is misleading, and it causes capable executives to avoid developing a skill they genuinely need.

Executive influence is the ability to align stakeholders around a decision when you do not have unilateral authority to impose it. It is not about changing what people fundamentally believe. It is about helping them see how your proposal connects to what they already care about — their strategic priorities, their organisational concerns, their professional risks. When done well, influence feels like clarity, not pressure. Stakeholders leave the room feeling understood rather than sold to.

The distinction matters because manipulation and influence produce different long-term outcomes. Manipulation extracts a single decision at the cost of future trust. Influence accumulates credibility that compounds across every subsequent interaction. Senior stakeholders — board directors, C-suite peers, institutional investors — are generally sophisticated enough to detect the difference within minutes. Attempting to manipulate a room of experienced non-executive directors is a short career strategy.

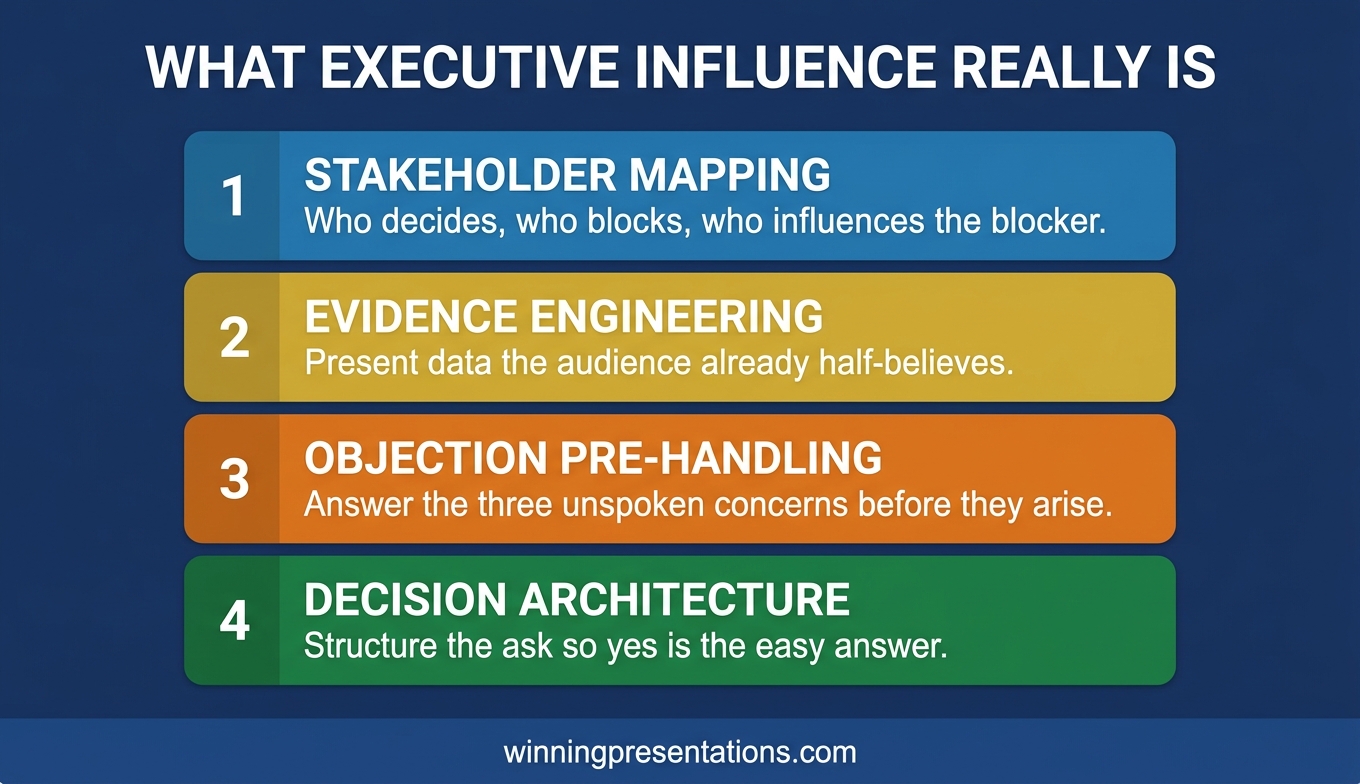

Genuine influence rests on three foundations: accurate understanding of what each stakeholder actually needs from the decision, credible evidence that your proposal serves those needs, and a presentation architecture that makes the fit between the two impossible to miss. None of these foundations are glamorous. All of them are teachable. This is the underlying logic of stakeholder buy-in psychology — and it is the core of any executive influence training worth the investment.

Executive Influence Training, Engineered for Senior Professionals

The Executive Buy-In Presentation System is a self-paced online programme that teaches the influence architecture used by senior executives to move material decisions through boards, investment committees, and C-suite peer groups. Stakeholder mapping, objection handling, credibility construction, and decision-ready presentation frameworks — all delivered in modules you can work through around your diary.

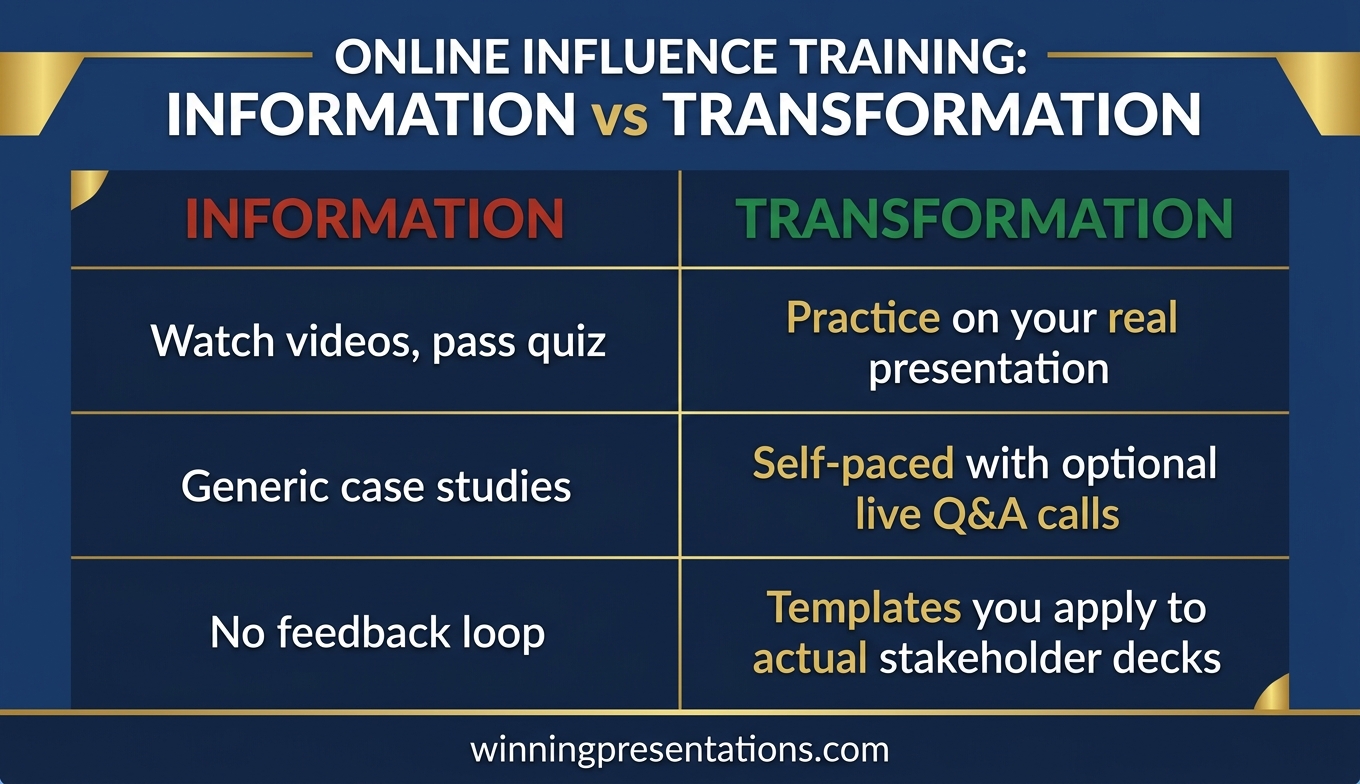

£499, self-paced with optional live Q&A calls (all recorded). Enrolment is open — join at your own pace.

Why Online Training Beats In-Person for Senior Professionals

There is a lingering assumption in executive education that the best training must happen in a room — a residential programme at a business school, a three-day off-site with a named professor, a corporate university cohort that meets quarterly. For many learning contexts, in-person retains real advantages. For executive influence training specifically, the calculus has shifted.

Calendar reality. Senior professionals do not have consecutive uninterrupted days. Board cycles, earnings windows, regulatory deadlines, and international travel make three-day workshops a scheduling fantasy for most executives above director level. A self-paced online programme that accommodates ninety-minute working sessions between meetings is not a compromise — it is a better match for how senior careers actually operate.

Applied repetition. Influence skills mature through repeated application in live situations, not through a single intensive workshop followed by a certificate. Online training that you can revisit before a specific board meeting, investment committee, or C-suite peer conversation compounds value in a way that a one-off residential cannot. You learn the framework once and then return to the relevant module the week before you need it.

Evidence-based learning. In-person executive programmes tend to favour memorable stories and charismatic delivery. Online formats favour systematic coverage — frameworks with worked examples, templates with live use cases, recorded sessions you can reference at the point of need. For a discipline where precision matters more than inspiration, systematic coverage wins.

Privacy. Many senior executives are reluctant to practise influence skills in front of peers. A shadow board, a regulatory scrutiny case, a private equity management presentation — these are exactly the scenarios most in need of training, and exactly the scenarios no executive wants to rehearse in front of strangers on a residential programme. Self-paced online learning allows genuine practice in a private environment.

The shift is not that in-person has become ineffective. It is that online delivery has become structurally better matched to how senior professionals actually learn and apply new skills in their day-to-day work.

What Genuine Executive Influence Training Covers

If you are evaluating executive influence training options, the syllabus matters more than the brand. Many programmes badge themselves as “executive influence” but cover little beyond generic communication skills repackaged for a premium audience. A credible syllabus addresses four specific domains:

Stakeholder mapping. Before you can influence a stakeholder, you need an accurate picture of their decision-making drivers, their information preferences, their past positions on similar issues, and the organisational pressures they are carrying. Training that teaches you to map this systematically — not just intuit it — is training that produces durable results.

Objection handling. Senior stakeholders raise objections in predictable structural categories: risk, cost, timing, precedent, alternatives, and fit with existing priorities. Training that teaches you to anticipate which category of objection each stakeholder will raise — and to build responses into the presentation itself rather than scrambling in Q&A — transforms how meetings unfold. This is one of the disciplines explored in depth in influencing senior executives.

Credibility building. Credibility is not a personality trait. It is a pattern of signals that stakeholders use to decide whether to trust your judgement. These signals include how you frame uncertainty, how you handle questions you cannot fully answer, how you position your recommendations relative to alternative options, and how you reference past decisions. Training that teaches credibility signalling explicitly is rare — and valuable.

Presentation frameworks. Influence is not delivered through free-form conversation. It is delivered through structured communications — board papers, investment cases, strategy proposals — that lead stakeholders through a sequence of logical steps towards the decision you are seeking. Training that gives you the underlying frameworks (not just templates) allows you to adapt to any high-stakes scenario rather than being trapped by a single format.

A programme missing any of these four domains is a communication course with an executive label, not genuine influence training.

If you want a structured approach to each of these domains, the Executive Buy-In Presentation System dedicates separate modules to stakeholder mapping, objection handling, credibility construction, and decision-ready presentation architecture.

Stakeholder Mapping: The Discipline Most Programmes Skip

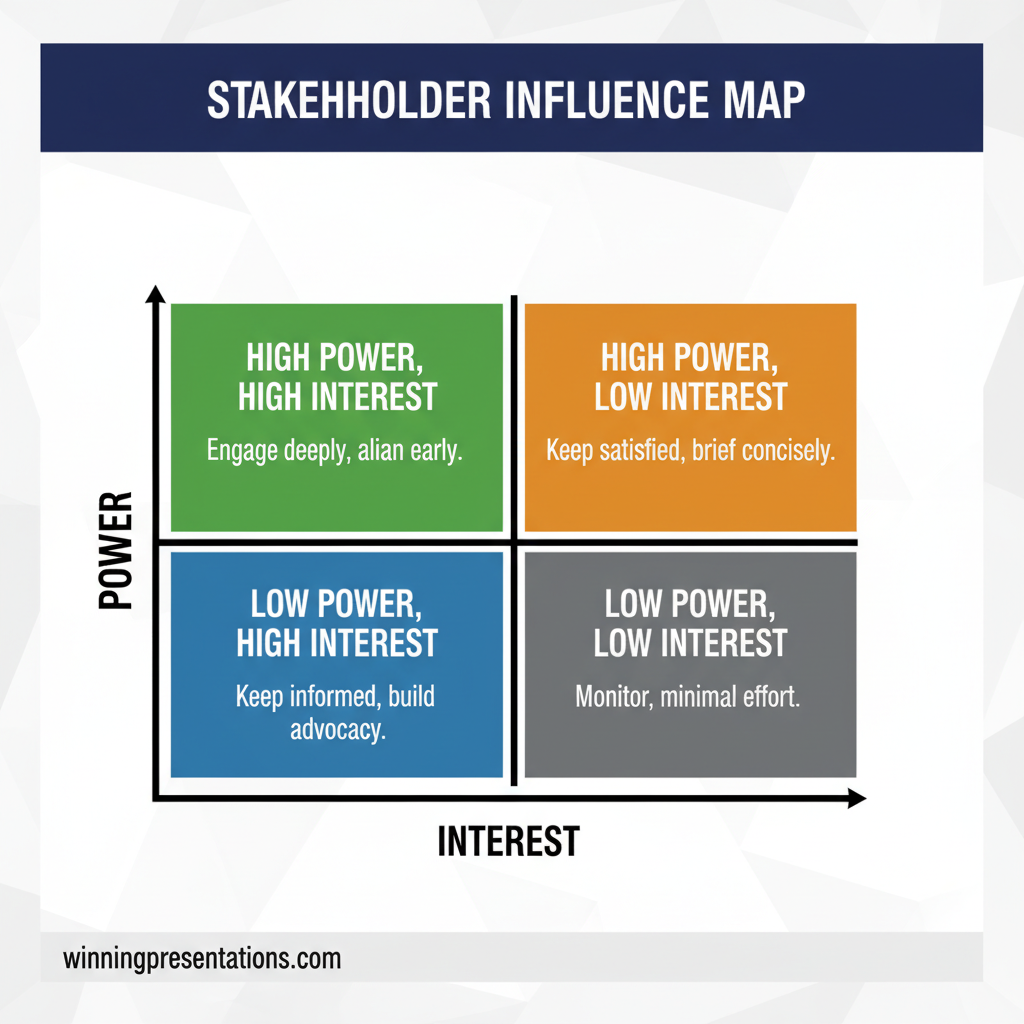

Most executive training courses treat stakeholder analysis as a two-by-two matrix exercise — interest versus influence, plotted on a whiteboard. That is a useful starting point for junior managers. For executives operating at board level, it is woefully incomplete.

Effective stakeholder mapping at senior level answers four questions for each individual whose support matters:

What is their decision history? How have they voted or positioned themselves on comparable issues in the past twelve to twenty-four months? Past decisions are the single best predictor of future receptivity. A director who has consistently challenged capital commitments above a certain threshold will challenge yours too — unless you pre-empt the challenge in the paper itself.

What are they professionally carrying? Every senior stakeholder has a set of external pressures that shape their instincts — a recent audit finding, a regulatory examination, a personal reputation concern, a committee they sit on, a past failure they are determined not to repeat. Understanding these pressures lets you frame your proposal in language that addresses what they are actually worried about, rather than what you assume they should be worried about.

What is their information preference? Some directors read every appendix before the meeting. Others scan the executive summary and rely on the discussion. Some want financial modelling detail; others want strategic narrative. Matching your presentation density to each stakeholder’s preference is not about flattery — it is about reducing the cognitive load that produces defensive responses in governance settings.

Who do they take counsel from? Senior stakeholders rarely form positions alone. They consult informally with trusted peers, executive search contacts, ex-colleagues, and advisers. If you can identify who your key stakeholders listen to, you can often shape the informal context around your presentation in ways that make a positive outcome significantly more likely.

This depth of mapping takes time — typically two to three hours per stakeholder for a major decision. Executives who do not make time for it are relying on intuition in a context where the penalties for being wrong are asymmetric.

Building Credibility Before You Need to Use It

The hardest moment to build credibility is the moment you need it. By the time you are standing in front of a sceptical board with a £48 million case, your credibility balance is already fixed — you are spending it, not accumulating it. This is why the most effective executive influence training emphasises credibility construction as a continuous discipline, not a meeting-specific skill.

There are four credibility signals that senior stakeholders weigh unconsciously in every interaction:

Calibrated confidence. You demonstrate calibration when you distinguish explicitly between what you know, what you believe, and what you are uncertain about. “Our modelling indicates a 70 per cent probability of hitting plan, with the downside scenario driven primarily by supply chain concentration” is a calibrated statement. “We are confident in the plan” is not. Calibration builds credibility because it shows your judgement is trustworthy — you are not overselling.

Predictable follow-through. If you commit to a piece of analysis by a committee meeting, deliver it — and if you cannot, flag it early. Stakeholders accumulate a mental ledger of who delivers on commitments and who generates drift. A clean ledger is one of the quietest forms of credibility, and one of the most durable.

Appropriate challenge. Executives who agree with everything their board says lose credibility as fast as executives who challenge everything. The sweet spot is disagreeing rarely but substantively, with evidence, when the disagreement genuinely matters. A director who sees you push back thoughtfully on a peer’s position is more likely to trust your analysis of your own material. This is one of the dimensions covered in executive presence training.

Intellectual generosity. Acknowledging the strongest version of opposing arguments — rather than straw-manning them — signals that you have genuinely engaged with the decision on its merits. Senior stakeholders notice this instantly. The executive who can articulate the case against their own proposal more compellingly than the sceptics in the room almost always wins the room.

These signals are teachable, but they require the kind of systematic, repeated application that self-paced online training supports better than a single residential programme.

The Online Influence Training Senior Professionals Actually Use

The Executive Buy-In Presentation System is a self-paced online programme for executives who need to move material decisions through boards, investment committees, and C-suite peer groups. Modules on stakeholder mapping, credibility construction, objection handling, and decision-ready presentation frameworks — designed to be worked through around senior diaries.

£499, self-paced with optional live Q&A calls (all recorded).

How the Executive Buy-In System Teaches Influence

The Executive Buy-In Presentation System is built around a single operating premise: senior professionals do not need more theory about influence — they need a system they can apply to the specific meeting on their calendar next month. The programme is organised around the decisions executives actually face, not around abstract competencies.

Module architecture. The programme is structured as a sequence of self-paced modules covering stakeholder mapping, objection pre-empting, credibility construction, slide architecture for high-stakes scenarios, and recovery tactics when meetings go sideways. Each module combines a framework, worked examples from real executive scenarios, and a set of templates you can adapt to your specific context.

Optional live Q&A calls. Alongside the self-paced content, the programme includes optional live Q&A sessions where enrolled executives can bring their own upcoming presentations for critique. All sessions are recorded, so missing a call never means missing the content. This is not a live cohort with fixed attendance requirements — it is a structured self-paced system with live support attached.

Applied practice. Each module includes practice scenarios built from real-world executive contexts — board meetings, investment committees, regulatory hearings, C-suite peer conversations. Rather than abstract exercises, the scenarios are designed to be worked through using an actual upcoming meeting on your calendar, which means the training pays for itself on the first presentation where you apply it.

Revisitable reference. The programme is designed to be returned to repeatedly rather than consumed once. An executive preparing for a board transformation vote can revisit the objection-handling module. An executive entering a new company can return to the stakeholder mapping module in their first ninety days. The value compounds across years, not just weeks.

Enrolment is open on a rolling basis, which means you can join at the point you need the training — not when a residential calendar dictates. For senior professionals whose diaries are the binding constraint, that flexibility is often the difference between investing in development and postponing it indefinitely.

Frequently Asked Questions

What is executive influence training?

Executive influence training teaches senior professionals how to align stakeholders around a decision in settings where authority is shared rather than assigned — boards, investment committees, C-suite peer groups, and regulatory forums. Genuine training covers stakeholder mapping, objection handling, credibility building, and presentation architecture. It is distinct from generic communication or public-speaking training because it focuses on the specific dynamics of rooms where experienced decision-makers are evaluating both the content and the judgement of the person presenting.

How long does online executive influence training take?

Self-paced online programmes typically require twelve to twenty hours of focused study to work through the core content, spread over four to eight weeks depending on the learner’s diary. Senior executives usually consume the material in ninety-minute blocks between meetings rather than in full-day sessions. The genuine value of influence training accrues over the following six to twelve months as learners apply the frameworks to specific upcoming presentations and revisit the material at the point of need. Unlike a three-day residential, online training is not finished when the calendar says so — it is finished when you have applied it across enough scenarios to make the skills reliable.

Is executive influence training worth it?

For senior professionals whose career progression depends on moving material decisions through groups they do not directly control, the return on structured influence training is difficult to beat. A single board paper that moves from deferral to approval often represents more economic value than the cost of the training itself. The more relevant question is not whether training is worth it, but whether the specific programme you are considering teaches the four foundational disciplines — stakeholder mapping, objection handling, credibility construction, and presentation architecture — or whether it is a communication course with an executive label. If a syllabus does not explicitly address those four domains, the training will polish delivery without building the underlying capability senior stakeholders actually respond to.

How does online training compare to in-person executive coaching?

One-to-one executive coaching remains valuable for deeply personalised situations — a specific leadership transition, a public reputation challenge, a particular board dynamic. For the underlying skill of influence, self-paced online training typically offers better coverage at a fraction of the cost and with greater schedule flexibility. The most effective approach for many senior professionals is a hybrid: a structured online programme to build the frameworks and templates, supplemented by targeted one-to-one coaching around specific high-stakes situations. Online training builds the repeatable system. Coaching sharpens its application to a particular moment. They are complements, not substitutes.

Join The Winning Edge

Free weekly newsletter for executives who present at board and committee level. Practical frameworks, stakeholder influence strategies, and slide structure guidance — delivered every Thursday.

Read next: If you are preparing to present to senior leadership specifically, see How to Present to Senior Management: A Framework for High-Stakes Meetings for a complementary guide on structuring communications that survive boardroom scrutiny.

Your next step: If you are evaluating executive influence training and want a programme built around the specific dynamics of senior stakeholder decision-making, explore the Executive Buy-In Presentation System. Enrolment is open — join at your own pace.

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes scenarios where stakeholder buy-in determines the outcome.