Quick Answer: A strong investor update deck has a consistent structure: headline position first, segment performance with variance explanations, forward quarter outlook with named risks, and a decisions-needed slide. The deck’s credibility depends on how you handle the weakest number, not the strongest. Investors learn to trust the reporting rhythm before they trust the forecast.

JUMP TO:

Astrid had to present her company’s Q2 update to a group of institutional investors who had been in the stock for six years. The quarter was uneven. Core business grew eleven percent. A newer product line — the one investors had been most vocal about — missed target by thirty-four percent. The natural instinct was to structure the deck around the good news and park the disappointing segment near the back.

She resisted that instinct, and it saved her reputation. When we rebuilt the deck together, the mixed segment went on slide four, named clearly, with a specific diagnostic and a revised twelve-month outlook. Her investor call that quarter had the same pushback you would expect. But six months later, when the segment had recovered, one of the largest holders told her on a private call: “The reason we held through that quarter was that you were the only management team who actually named what was broken.”

An investor update deck is a quarterly trust-building exercise. You are not presenting quarterly numbers. You are presenting your reliability as a reporter of those numbers. The deck that handles a bad quarter well is worth more than the deck that handles a good quarter well, because reliability is tested by bad quarters.

If your next investor update is mixed

The Executive Slide System includes structural templates for quarterly reviews and investor updates — including the mixed-quarter slide sequence referenced here.

Why investor deck structure matters more than content

Institutional investors read many decks every quarter. They look for patterns. A consistent deck structure, repeated quarter after quarter, does something content alone cannot: it establishes reporting rhythm. Investors start to anticipate the deck, and when the structure changes they notice — which is exactly what you want during a difficult quarter.

An inconsistent structure — different slide order each quarter, different segment groupings, different variance explanations — signals that management is reacting to the numbers rather than operating a stable reporting discipline. Even if the quarter’s results are strong, inconsistent structure erodes the underlying trust relationship.

The practical implication: decide your investor deck structure once, document it, and resist the temptation to restructure it when the numbers are uncomfortable. If you have to hide a segment inside a new slide arrangement, the investors have already seen the trick.

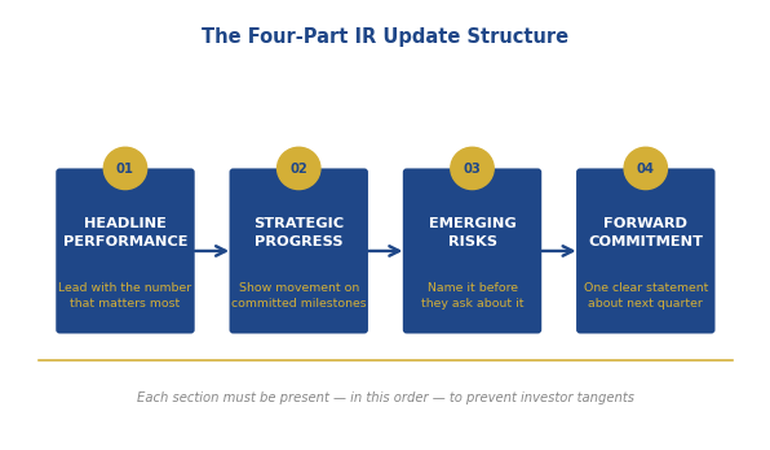

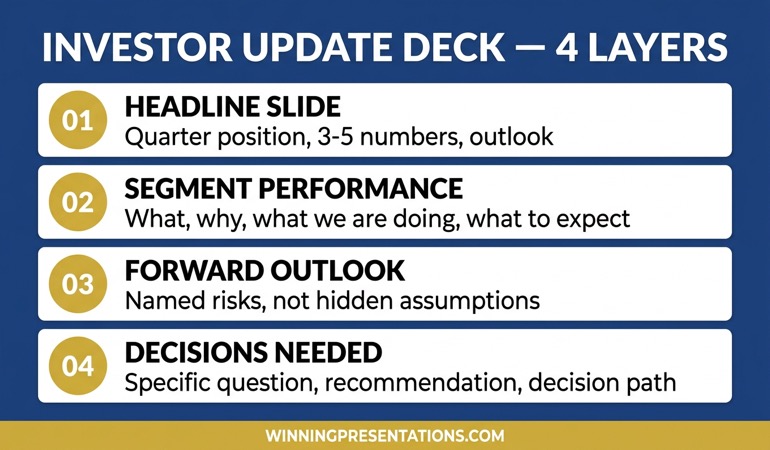

The headline slide: position before numbers

The first slide is not a title slide. It is the headline, and it takes a clear position. Three components:

The quarter in one sentence. Not a metric — a position. “Core business accelerated; newer product line underperformed materially and we have taken specific action.” The sentence earns its place by being true under scrutiny.

Three to five headline numbers. Revenue, growth rate, margin, cash position, and one forward indicator. These are always in the same order. Investors can compare at a glance to prior quarters.

The one-line outlook. Not detailed forecasts — a position on whether the forward quarter outlook has changed from the prior update. “Outlook unchanged” or “Outlook revised — details on slide seven.” Either is credible. What is not credible is an outlook that moves materially without explanation.

THE EXECUTIVE SLIDE SYSTEM — £39

The same deck structure, every quarter, without rebuilding from scratch

26 templates, 93 AI prompts, 16 scenario playbooks. The investor update playbook has the full slide sequence — headline, segments, outlook, decisions — with formatting that works for both in-person board settings and shareholder calls. £39, instant access.

Get the Executive Slide System →

Designed for recurring investor, board, and executive reporting cycles.

Segment performance with honest variance

The segment section is where mixed quarters are won or lost. A single layout applied to every segment — whether the segment performed well or poorly — creates the consistency that investors recognise and reward.

The layout is four blocks per segment:

- What happened: the actual number versus the prior-quarter forecast, plus trend direction.

- Why: the specific driver, in operational language, not marketing language. “The largest customer delayed a contracted order from Q2 to Q3” is operational. “Macro headwinds impacted demand” is marketing.

- What we are doing: the specific action being taken. If the answer is “monitoring closely,” the investors have already stopped listening.

- What to expect next quarter: the specific, falsifiable expectation. “We expect the contracted order to close in Q3 and margin to normalise.” If that expectation is wrong next quarter, that becomes the next quarter’s opening admission.

The discipline of naming a falsifiable next-quarter expectation is what separates reporting from narrative. Investors track these expectations across quarters. When you meet them, credibility compounds. When you miss them, the miss is already embedded in the reporting structure — it is a known miss against a named commitment, not a surprise.

For the related structure on annual reviews, the quarterly business review framework applies the same discipline to internal reporting cycles.

Forward outlook with named risks

The forward outlook section has a simple rule: no range is credible unless accompanied by the assumptions that would move it. A revenue outlook of £240m to £270m means nothing on its own. A revenue outlook of £240m to £270m, with the lower bound assuming the top-two customer renewals do not close in Q4 and the upper bound assuming they close on historical terms, is a range investors can pressure-test.

Name three to five specific risks that would move the outlook materially. Name them in the deck — not in the appendix, not in the Q&A. The risks investors can see are the risks they trust you are managing. The risks you hide are the risks they will surface themselves, and the surfacing will damage the update.

Specific, named risks also create a useful asymmetry in the Q&A. When an analyst raises a risk you have already named, you answer from your prepared position. When an analyst raises a risk you have not named, you answer from a defensive position. The difference matters. Investors cannot tell whether your analysis is accurate, but they can tell whether you are answering from strength or weakness.

Related: the annual budget presentation framework covers how to structure forward outlook for internal budget approval committees.

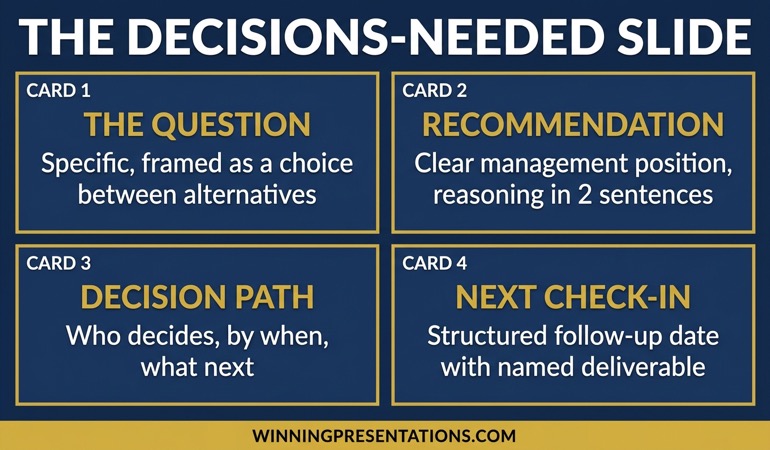

The decisions-needed slide

Some investor updates do not require decisions. Most do. Even a routine update typically has one or two items where investor input is genuinely useful: a capital allocation question, a strategic sequencing question, a governance matter. A dedicated decisions-needed slide near the end of the deck is how you surface these items with enough signal for them to get addressed.

The slide has three sections. The question (specific, framed as a choice between named alternatives). The management recommendation (clear, with the reasoning in two sentences). The decision path (who decides, by when, and what the next check-in looks like). Without this slide, decisions drift through Q&A and often do not get resolved. With it, investor input shapes the next ninety days.

If you need a ready-made template for the decisions-needed slide — including the recommended formatting for the recommendation and decision-path sections — the Executive Slide System scenario playbook for investor updates includes it.

How to handle a mixed quarter

A mixed quarter is the quarter that most damages or most reinforces your reporting credibility. The choice between the two outcomes is structural.

Lead with the mixed result, not the strong result. If core business was up and the newer product line missed, the opening headline names both — in that order. Opening with only the strong number and introducing the miss later in the deck signals that the sequence was chosen to manage the message. Investors notice.

Provide an operational diagnostic, not a narrative one. “Demand softened in the segment” is a narrative. “Three of our top-five customers in the segment deferred orders after a procurement change; we have re-engaged with each and expect resolution by end of Q3” is a diagnostic. The diagnostic is harder to write but more credible.

Name what you have changed. Not the corrective action plan — the actual change. If nothing has changed, say so and explain why the segment is expected to recover without intervention. “No structural change required; Q2 delay was transactional, not systemic” is a valid position if you can defend it.

The related risk committee presentation framework uses the same diagnostic discipline for risk-weighted internal decisions.

STOP REBUILDING THE DECK EVERY QUARTER

A consistent investor update framework, scenario-by-scenario

The Executive Slide System includes the investor update playbook — headline slide, segment performance layout, forward outlook structure, decisions-needed slide. £39, instant access.

Frequently Asked Questions

How long should an investor update deck be?

For a quarterly update, fifteen to twenty-five slides is typical. Longer decks signal a lack of editorial discipline. If you cannot cover the quarter in twenty slides, the material has not been edited enough. The appendix is where extended detail lives — it stays available but does not occupy presentation time.

Should I include questions I expect investors to ask?

Yes, but in the Q&A preparation document, not on the slides. The deck is your narrative. The Q&A document is your side preparation. Anticipating the top ten investor questions and rehearsing the answers is one of the highest-value uses of preparation time — arguably more than a final pass on the slides.

What if the CFO and I disagree on how to position a segment?

Resolve it before the meeting. A visible disagreement between the CEO and CFO during an investor update is more damaging than either of your individual positions. Align first, then present. If alignment is genuinely not possible, one of you presents and the other supports without contradicting — and the disagreement goes into a private follow-up session.

How do I handle investor pushback on the forward outlook?

Pushback on the outlook is useful signal. Take it, note it specifically, and commit to a follow-up. Do not defend the outlook in the moment if the pushback has merit. “That is a fair challenge. Let me take it back and come back to you with a revised view by end of next week” is a stronger position than trying to defend a number live. Investors respect the willingness to revise more than the defence of a position.

Structures for the meetings that matter, every Thursday

The Winning Edge is a weekly newsletter on the structural mechanics of high-stakes presentations. Concise, practical, no filler. Typically read in four minutes.

Not ready for the full system? Start here instead: download the free Executive Presentation Checklist — a one-page structural review for any high-stakes executive presentation.

Partner post: For the narrower case of presenting to a single risk-averse decision-maker, the risk-averse CEO presentation framework covers the one-to-one dynamic.

Your next step: Before your next investor update, pull up the deck from two quarters ago. If the structure is different, you have already identified the problem. Fix it once and commit to it.

About the Author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds and approvals.