In this article:

- Why Finance Committees Defer, Not Reject

- The Six-Slide Structure That Earns Approval in the Room

- Surface the Assumptions Before the Committee Does

- The Sensitivity Slide: Your Most Important Defence

- The Seven Questions Every Finance Committee Asks

- Chairing Your Own Request: Pacing the Conversation

- Frequently Asked Questions

Astrid Halvorsen, finance director at a Nordic industrial group, walked into the quarterly finance committee with a €28m capex request for a new production line. She had the engineering numbers, the payback calculation, and the competitive context. She opened with the strategic rationale, walked through the financial model, and finished with the timeline. Forty-two minutes. No interruptions. Professional silence.

The committee chair thanked her, paused, and said the words every capex sponsor dreads: “Thank you, Astrid. Very thorough. We’d like to take this offline and come back at the next session.” Four months of work, and the only decision in the room was to defer the decision.

In the corridor afterwards, the CFO was honest. The numbers were fine. The engineering was fine. The issue was that nobody on the committee could see, in the sequence of what Astrid had shown, what they were actually being asked to approve. The slides had explained the project. They had not structured a decision.

Six weeks later, Astrid re-presented with a different structure. Same project, same numbers, same €28m. The committee approved in nineteen minutes. What changed was the order in which she surfaced the strategic choice, the assumptions, and the sensitivities. The content had not been the problem. The sequence had been.

If you want a structured approach for capital expenditure presentations to finance committees, the Executive Slide System includes scenario playbooks and slide templates designed for capex, budget defence, and investment committee approval scenarios.

Why Finance Committees Defer, Not Reject

Finance committees rarely reject capex outright. They defer. A deferral feels softer than a rejection, but it is functionally the same outcome: the project does not happen on the timeline the business needs. The deferral signal is almost always structural. The committee has been given information in a sequence that did not build toward a decision, and so the safest decision — defer — is the one they reach by default.

The typical capex presentation starts with project context, walks through the financial model, ends with a timeline, and invites questions. This is a description of a project. It is not a decision frame. The committee is asked to approve a spend without being given a clear articulation of what they are choosing between. The absence of a choice architecture is what generates the “take it offline” response.

The second cause of deferrals is unresolved assumptions. Every capex case rests on forecast assumptions — demand growth, utilisation rates, unit economics, commodity inputs, discount rate. If the presenter does not surface those assumptions explicitly, the committee surfaces them in the discussion. Once a committee starts uncovering assumptions themselves, they lose confidence that they have been told the full picture, and the default response is caution. Caution equals deferral.

Stop Rebuilding Capex Decks From Scratch

The Executive Slide System includes 26 templates, 93 AI prompts, and 16 scenario playbooks — covering capital expenditure, budget defence, investment committee, and financial approval scenarios. Structured for committees that need a decision frame, not another project description.

£39 — instant access. Designed for executives who present capex and investment cases to finance committees.

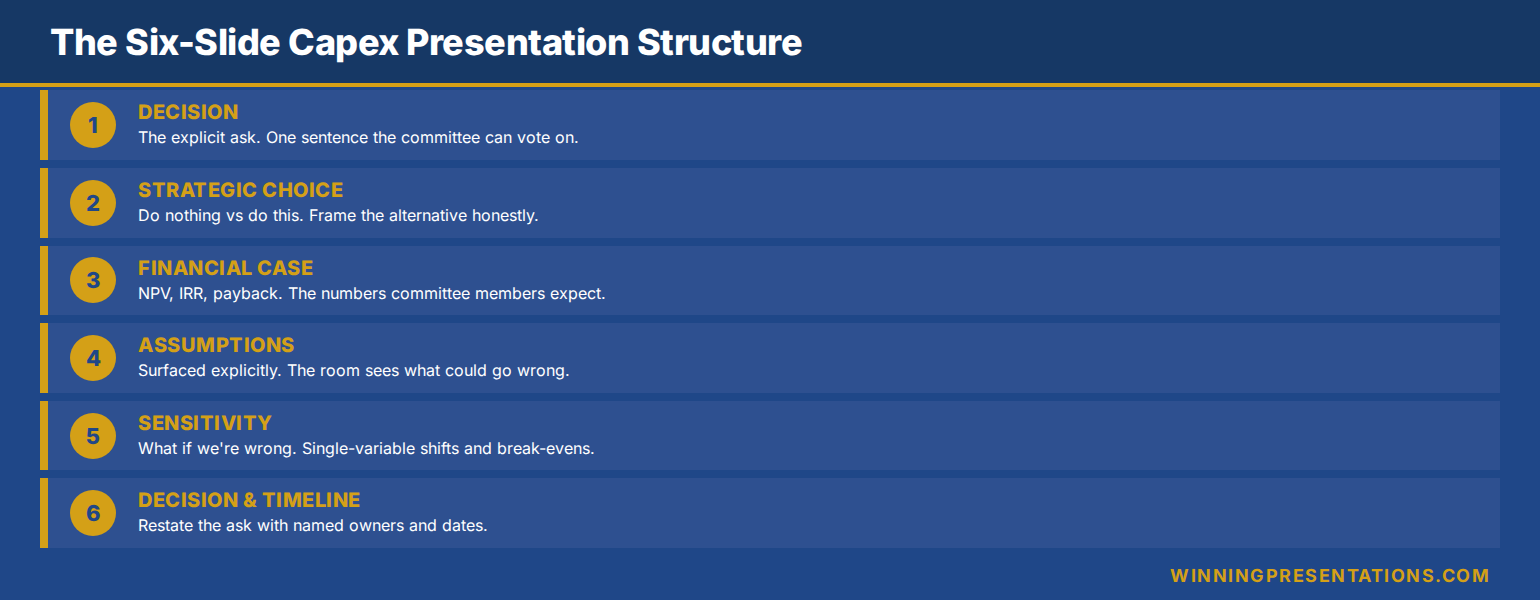

The Six-Slide Structure That Earns Approval in the Room

A finance committee capex presentation that secures an in-room decision follows six slides in a specific order. More than six and you dilute the decision frame; fewer and you leave defensible questions unanswered.

Slide 1 — The decision being asked for. Not the project. Not the context. The explicit decision. “We are asking the committee to approve €28m of capital expenditure to build a second production line in Gothenburg, to be commissioned by Q3 next year, funded from the 2027 capex envelope.” State the ask in the first forty seconds. The committee now knows what they are deciding on and can orient every subsequent slide against that frame.

Slide 2 — The strategic choice. What does approving this enable, and what does not approving it concede? This is the “do nothing versus do this” slide, and it is the slide most often missing from capex decks. Without it, the committee has no basis for comparison. A capex request is never evaluated in isolation — it is always evaluated against the alternative use of the capital. Make that alternative explicit.

Slide 3 — The financial case. NPV, IRR, payback period, and the basis for the discount rate. One slide. No financial modelling deep-dive. The detailed model sits in the appendix or pre-read. The committee needs three numbers in the room, not thirty.

Slide 4 — The assumptions. Explicit. Listed. Owned. The three or four assumptions the financial case rests on, with the direction of sensitivity. This slide pre-empts the committee’s most common question (“what are we assuming about demand?”) by surfacing the answer before they ask.

Slide 5 — The sensitivity and risk frame. What happens if the key assumptions shift by twenty per cent? What is the break-even demand level? What would cause us to recommend pausing the project mid-build? This slide is the committee’s confidence slide — without it, every question becomes a challenge to your optimism.

Slide 6 — The decision and timeline. Restate the ask. Restate what happens if approved today versus approved next quarter. State the governance structure for the project post-approval. End with the explicit request: “We are asking for approval today.”

Surface the Assumptions Before the Committee Does

The most common error in a capex presentation is burying the assumptions. Presenters want the financial case to look robust, so they state the NPV and IRR confidently and leave the assumptions implicit. A finance committee has decades of collective experience reading capex cases. They know the assumptions are there. The only question is whether the presenter will surface them first, or whether the committee will have to extract them.

Surfacing first is strategically better for one reason: it signals intellectual honesty. A presenter who says “this case depends on sustaining 78 per cent utilisation for the first four years — if that slips below 65 per cent, the NPV turns negative” has pre-empted the committee’s suspicion. A presenter who leaves the utilisation assumption buried in a financial model appendix creates the impression of having something to hide, even when they do not.

Structure the assumptions slide around three questions. What are the three or four most important numerical inputs? Where do those inputs come from — market data, internal forecast, vendor commitment, historical trend? What is the sensitivity of the NPV to each input? A committee that can see your thinking on these questions treats you as a credible counterpart. A committee that cannot treats the presentation as a sales pitch.

Related frameworks for structured financial storytelling appear in the guide to presenting financial data, which covers the broader discipline of converting numerical cases into decision-ready narratives.

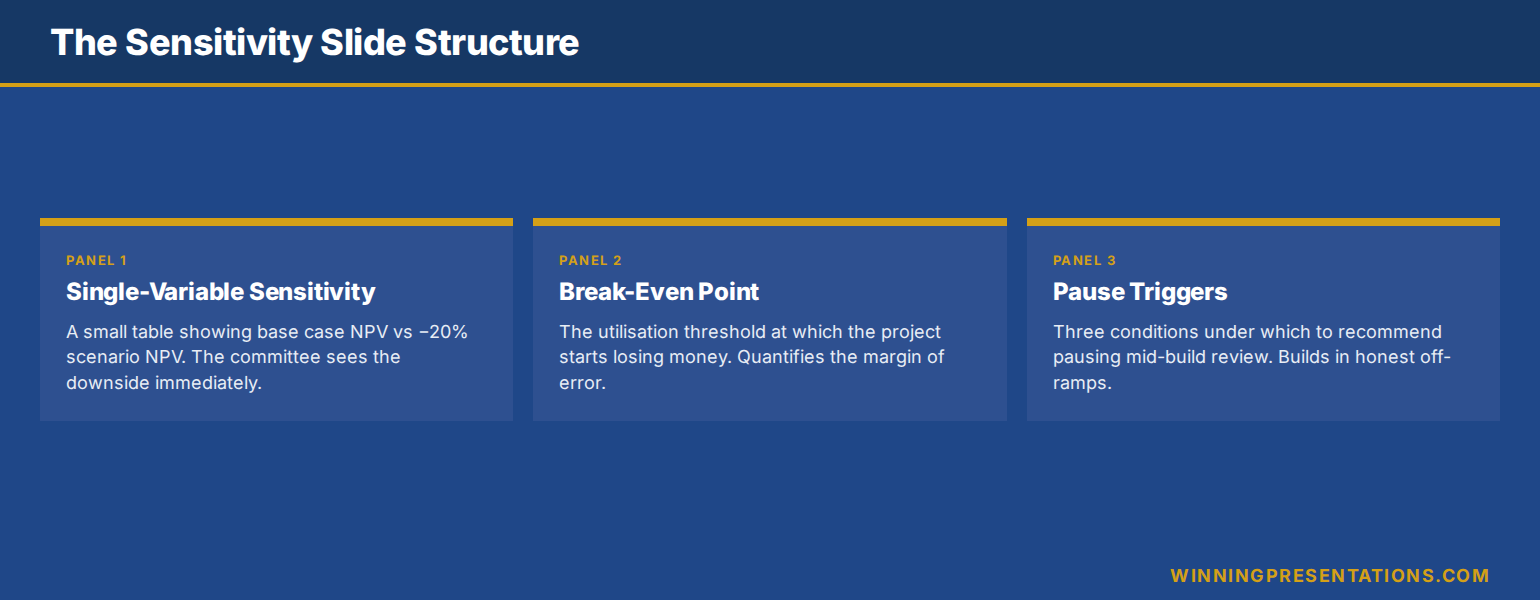

The Sensitivity Slide: Your Most Important Defence

Every experienced finance committee member asks the same question, in some form, during capex presentations: “What happens if you’re wrong?” The sensitivity slide is the answer. Build it, show it, and refer to it by default whenever a challenge is raised.

Single-variable sensitivity. For each of the three or four key assumptions, show the impact on NPV if that assumption moves by twenty per cent in the adverse direction. A simple table: assumption, base case, minus twenty per cent scenario, NPV outcome. The committee can read this in five seconds and is no longer asking the question in their head.

Break-even point. At what level of the key assumption does the project stop being NPV-positive? “If utilisation falls below 64 per cent across the first four years, the project returns its cost of capital but nothing more.” This number is more useful to the committee than an optimistic central case — it tells them the floor, which is what a committee actually approves against.

Pause triggers. Under what conditions would you recommend pausing the project mid-build? This is the slide that converts you from a sponsor into a fiduciary. A sponsor says “I believe in this project.” A fiduciary says “I believe in this project, and if these three conditions emerge during execution, I will recommend we pause and revisit.” Committees approve fiduciaries.

If you want a starting point for structuring sensitivity and risk slides, the Executive Slide System includes templates built for investment committee and capex defence scenarios.

Slide Templates for Committee Approval, Not Project Descriptions

The Executive Slide System gives you 16 scenario playbooks and 93 AI prompts for structuring capex, budget, and investment committee presentations — with decision frames, assumption slides, and sensitivity structures built in.

£39 — instant access.

The Seven Questions Every Finance Committee Asks

Finance committee questions cluster around seven predictable themes. A presenter who pre-empts these in the deck structure faces a much shorter and more collaborative Q&A. A presenter who does not faces forty minutes of reactive defence.

1. Why now? Why does this capex need to be approved in this cycle rather than deferred to the next budget round? The answer is almost always a combination of commercial opportunity cost and execution constraint — make both explicit.

2. What are we assuming about demand? The most common challenge. Answered by the assumptions slide.

3. What is the alternative use of this capital? Capital has a cost and a next-best use. Committees think in portfolios. Demonstrate that you have too.

4. What happens if we phase it? Can this be split into tranches with decision gates? Phased capex is easier to approve than a single lump approval, and offering a phased option voluntarily often earns approval on the full amount.

5. Who owns delivery? Committees approve capital to named executives, not to projects. Make the accountability explicit.

6. What is the post-investment review plan? When will the committee see the actuals against the plan, and against what milestones? A presenter who proposes a review protocol voluntarily signals confidence and discipline.

7. What could go wrong that we have not discussed? The hardest question. The best answer is a two-sentence acknowledgement of the biggest risk you genuinely lose sleep over, with a one-sentence mitigation. Fake candour is worse than no candour — experienced committees detect it instantly.

Chairing Your Own Request: Pacing the Conversation

You are not just the presenter. You are the chair of your own decision request. How you pace the conversation is part of the deck.

Open with the ask, not the story. A capex committee is not an audience that wants to be taken on a journey. They have read the pre-read. Open with the decision you are asking for, then walk the structure. You lose ten minutes of goodwill if you spend the first ten minutes on project context they already have.

Pause for interruption after each structural slide. The assumptions slide and the sensitivity slide are the two where the committee will want to interject. Build a five-second pause into your delivery after each, and make eye contact with the chair. If they have a question, this is the moment. If they do not, move on. Not building in the pause means they interrupt anyway — but now in the middle of your next slide, which fragments your flow.

Convert a discussion point into a decision point. When the committee starts debating the merits of the case, the temptation is to let the discussion run. Do not. After four or five minutes, intervene: “Chair, would it be useful if I restated the specific decision we are asking the committee to take today?” This is a chair move, not a presenter move, and it is legitimate when your deck is the subject of the discussion. Committees rarely resent it — they appreciate a presenter who helps them reach a decision rather than one who lets the discussion drift.

Close with explicit confirmation. “Chair, on the basis of what the committee has heard, are we able to record approval for the €28m capex in today’s minutes?” This direct close feels uncomfortable the first time. It is also the move that most often secures the approval in the room rather than next quarter. The same discipline applies across related board presentation slides where the presenter must convert discussion into decision.

Frequently Asked Questions

How long should a capex presentation to a finance committee be?

Twelve to fifteen minutes of presented content, followed by fifteen to twenty minutes of Q&A and discussion. The six-slide structure delivers to this timing. If your deck needs more than six slides to tell the story, the appendix is the right place for the detail — not the live presentation.

Should the pre-read contain the full financial model?

Yes, but separated from the executive summary. The pre-read should include a two-page executive summary that mirrors the six-slide structure, followed by the full model as an appendix. This lets committee members who want to engage with the detail do so at their own pace, without forcing the rest to wade through it.

How do you handle a committee that wants to defer despite strong numbers?

Ask explicitly what specific piece of information would move the decision from defer to approve. A committee that is deferring on structural grounds will often be unable to articulate the answer — at which point you can help surface the actual concern. A committee that can articulate a specific gap has given you a focused piece of work rather than a vague deferral.

What is the biggest mistake in capex presentation structure?

Treating the presentation as a description of the project rather than a structured decision request. Descriptive decks explain what the project is; decision-structured decks tell the committee what they are choosing between, what the case rests on, and what they are being asked to approve. Committees defer on descriptive decks. They decide on structured ones.

Join The Winning Edge

Free weekly newsletter for executives who present capex, budgets, and investment cases to finance committees. Practical frameworks, decision-structured slide approaches, and committee chairing techniques — delivered every Thursday.

Not ready for the full system? Start here instead: download the free Executive Presentation Checklist — a quick-reference guide for structuring any high-stakes executive presentation, including capex and investment committee scenarios.

Read next: If the capex request relates to a recent acquisition or integration programme, see Acquisition Integration Briefing: How to Update the Board Without Losing Them for a complementary framework on structuring post-deal investment requests.

The next step is structural. Take your current capex deck and check it against the six-slide sequence. Is the decision slide first, or buried? Is there a strategic choice slide, or just a project description? Are the assumptions explicit, or implicit? Rebuild the order before your next committee, and the Q&A will compress by half.

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes scenarios — including capital expenditure requests, budget defence, and investment committee approvals.