Quick Answer

Boardroom presentation skills are not about charisma or natural confidence. They are a structured set of competencies covering how you organise information for senior decision-makers, how you design slides that support rather than replace your argument, and how you handle questions from people who are paid to challenge your thinking. These skills can be learned systematically, and the executives who present most effectively in boardrooms are typically the ones who have invested in structured preparation — not the ones who rely on instinct.

In this article

- What the boardroom requires that other settings do not

- The three core competencies of boardroom presenters

- Slide design principles for board-level audiences

- Delivery under pressure: pacing, tone, and presence

- Q&A at board level: how to handle challenge without losing control

- Frequently asked questions

Emeka had been presenting project updates to his line manager for three years with no issues. Then he was asked to present a strategic recommendation to the executive committee.

He built the same kind of deck he always built: detailed, thorough, twenty-eight slides covering every aspect of the proposal. He rehearsed the content until he could deliver it without notes. He arrived early, tested the projector, and felt reasonably prepared.

The CEO stopped him on slide five. “What are you asking us to decide?” Emeka paused. He knew the answer — it was on slide twenty-two. But the question exposed something he hadn’t considered: his deck was built to explain, not to persuade. In a boardroom, the audience doesn’t wait for the explanation to finish before they start making judgements. They are evaluating your recommendation from the moment you open your mouth. And if they have to wait twenty-two slides to find out what you’re recommending, you have already lost them.

That meeting changed how Emeka approached every subsequent board presentation. Not by learning to be more confident, but by learning to structure his content for the way board-level audiences actually process information.

Preparing for a boardroom presentation?

The Executive Slide System gives you the templates and frameworks designed specifically for board-level audiences — so your content is structured for how executives actually make decisions.

What the Boardroom Requires That Other Settings Do Not

The boardroom is not simply a higher-stakes version of a team meeting. It operates under a different set of rules, and presenters who treat it as a scaled-up project update consistently underperform.

Board members and executive committees have three characteristics that distinguish them from other audiences. First, they are time-constrained. A board meeting covers multiple agenda items in a fixed window. Your slot is shorter than you think, and the expectation is that you will use it efficiently. A presentation that takes forty minutes when you were allocated twenty signals that you do not understand the audience you are presenting to.

Second, they are decision-oriented. Every item on a board agenda exists because a decision is required. If your presentation does not contain a clear recommendation and a specific ask, the board will wonder why it was on the agenda at all. Information for its own sake is not valued at this level — information that supports a decision is.

Third, they are adversarial by design. Board members are paid to challenge, question, and stress-test proposals. This is not personal. It is governance. A presenter who interprets board questions as criticism rather than due diligence will become defensive — and defensive presenters lose boardrooms. The ability to receive challenge calmly and respond with evidence is the single most important boardroom presentation skill.

Understanding board presentation best practices starts with accepting these three realities and building your presentation around them — not around what you want to communicate.

The Three Core Competencies of Boardroom Presenters

Effective boardroom presenters are not born. They are developed through deliberate practice in three specific areas.

Competency 1: Executive framing

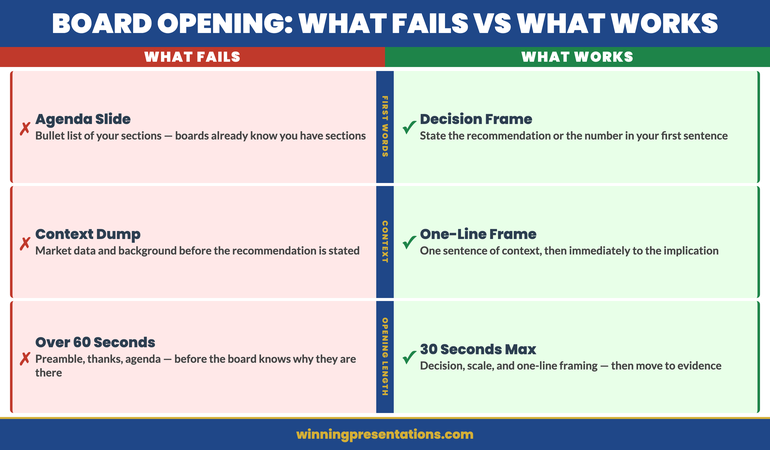

Executive framing means structuring your content so that the recommendation comes first, the evidence comes second, and the detail comes only when requested. This is the inverse of how most professionals are trained to communicate — in academic and technical settings, you build the case before presenting the conclusion. In a boardroom, the conclusion is the starting point. Everything else is evidence the audience evaluates against the conclusion you have already stated.

The practical test: if a board member walked in five minutes late and heard only your opening three sentences, would they know what you are recommending? If not, your framing needs to change.

Competency 2: Visual discipline

Board slides serve a fundamentally different purpose from team slides. A team slide can carry detailed data, complex charts, and supporting text because the audience will spend time with it. A board slide needs to communicate one idea per slide — clearly, visually, and without requiring the audience to read paragraph-length text while you’re speaking. The best board decks are visually spare: headline, supporting visual or data point, and nothing else. Everything else goes in the appendix.

The executive presentation structure that works at board level follows this principle: fewer slides, each carrying a single clear message, arranged in the order the board needs to receive them — not the order you created them.

Competency 3: Composure under challenge

This is the competency that separates good boardroom presenters from adequate ones. When a board member challenges your numbers, questions your methodology, or pushes back on your recommendation, how you respond matters more than what you say. Composure signals preparation. Defensiveness signals insecurity. The response framework is simple: acknowledge the point, address it with specific evidence, and move on. If you don’t have the answer, say “I’ll confirm that and come back to you by end of day” — not “That’s a good question” followed by improvisation.

Build Boardroom-Ready Decks in Half the Time

The Executive Slide System — £39, instant access — gives you the templates, frameworks, and AI prompt cards designed specifically for board-level audiences:

- 22 PowerPoint templates designed for executive and board presentations

- 51 AI prompt cards to build board-ready slides quickly

- Executive summary and strategic recommendation frameworks

- 6 checklists covering board, investor, sales, and executive scenarios

Get the Executive Slide System →

Designed for professionals preparing to present at board and executive level.

Slide Design Principles for Board-Level Audiences

Board slides fail when they try to do too much. The most effective board presentations follow four design principles that keep the audience focused on the decision rather than the data.

One message per slide. If a slide communicates two ideas, split it into two slides. Board members process information in units. A slide that contains both a financial forecast and an implementation timeline forces the audience to switch context mid-slide — and most won’t. They will focus on one and miss the other.

Headlines that state conclusions, not topics. A slide titled “Q3 Financial Results” tells the audience what the slide is about. A slide titled “Q3 Revenue Exceeded Forecast by 12%” tells the audience what to think about it. The second approach saves time, reduces ambiguity, and lets the audience evaluate the evidence against a stated conclusion rather than trying to derive the conclusion from the evidence.

Data in context, not isolation. A chart showing revenue at £4.2 million means nothing without a reference point. Revenue at £4.2 million against a forecast of £3.8 million tells a story. Revenue at £4.2 million against a forecast of £3.8 million and a prior year of £5.1 million tells a different story entirely. Every data point on a board slide needs context: versus budget, versus prior period, versus target.

Appendix for depth. The main deck should be ten to fifteen slides. The appendix can be fifty. This structure lets you present a concise narrative while having detailed evidence available if a board member wants to go deeper on a specific point. Saying “That’s covered on appendix slide 34 — I can walk through the detail if helpful” is one of the most effective boardroom moves. It signals both preparation and respect for the board’s time.

The opening lines of a board presentation set the tone for everything that follows. Get the first slide right — clear headline, specific recommendation, confident framing — and the rest of the presentation flows from a position of strength.

If you need templates for these slide formats, the Executive Slide System includes board-ready PowerPoint templates with headline-first layouts and executive summary frameworks built for these exact scenarios.

Delivery Under Pressure: Pacing, Tone, and Presence

Boardroom delivery is not about performance. It is about clarity under pressure. The executives in the room are evaluating your competence through how you communicate — not just what you communicate.

Pacing. Most presenters accelerate under pressure. In a boardroom, this reads as nervousness. The deliberate counter-move is to speak slightly slower than feels natural. A presenter who pauses after key points and lets the room absorb them signals confidence. A presenter who rushes through thirty slides signals that they are afraid of being stopped — which, ironically, makes the board more likely to stop them.

Tone. Boardroom tone is conversational, not performative. You are not giving a keynote. You are briefing a group of senior colleagues on a matter that requires their input. The register should be the same as if you were explaining the proposal to a respected peer over coffee — informed, measured, direct. Avoid the presentation voice that many people adopt when they stand at the front of a room: higher pitch, faster pace, more filler words. If you notice yourself shifting into performance mode, pause, take a breath, and resume at conversational pace.

Presence. Presence in a boardroom is largely a function of preparation and composure, not personality. A quiet presenter who knows their material and handles questions with specificity will always outperform a confident presenter who improvises answers and glosses over gaps. The board is assessing whether you can be trusted with the decision you are recommending. That trust comes from demonstrating that you have thought about the problem more deeply than they have — not from demonstrating that you are comfortable in the spotlight.

Q&A at Board Level: How to Handle Challenge Without Losing Control

The Q&A is where boardroom presentations are won or lost. A strong deck can be undermined by weak question handling, and a competent Q&A performance can rescue a deck that was only adequate.

Anticipate the top five questions. Before every board presentation, write down the five most likely questions you will be asked. For each one, prepare a specific, evidence-based answer — not a general deflection. Board members ask questions they already know the answer to; they are testing whether you know it too.

Answer the question that was asked. Under pressure, presenters often answer the question they wish had been asked rather than the one that was. If a board member asks “What is the worst-case scenario?”, do not redirect to the expected scenario. Answer the specific question directly, then add context. The pattern is: direct answer, supporting evidence, context. In that order.

Own what you don’t know. “I don’t have that figure to hand, but I’ll confirm it and circulate to the board by end of day” is a perfectly acceptable boardroom answer. What is not acceptable is improvising a number, hedging with qualifiers, or visibly floundering. Board members have seen hundreds of presenters. They can tell the difference between a genuine knowledge gap and a competence gap. Owning the gap quickly and specifically is how you keep their confidence.

Do not argue with the chair. If the board chair redirects the conversation, closes a line of questioning, or asks you to move on, do so immediately. The chair controls the room. A presenter who pushes back against the chair’s direction — even politely — signals that they do not understand the governance dynamic. Save the additional point for a follow-up email.

See also how today’s related articles tackle adjacent challenges: structuring a budget overrun presentation for executive committees, adapting presentations for cross-cultural audiences, and the career cost of avoiding presentations at work.

Stop Building Board Decks From Scratch

The Executive Slide System — £39, instant access — includes 22 board-ready templates and 51 AI prompt cards that build your deck in half the time. No more starting from a blank slide.

Get the Executive Slide System →

Designed for professionals who present to boards and executive committees.

Frequently Asked Questions

How many slides should a boardroom presentation have?

Ten to fifteen in the main deck, with an appendix of as many as needed for supporting detail. The main deck should cover the executive summary, the recommendation, the key evidence, the risk assessment, and the ask — nothing more. Every additional slide dilutes the narrative and reduces the time available for Q&A, which is where the real decision-making happens.

What is the most important boardroom presentation skill?

Composure under challenge. The ability to receive a direct, sometimes sharp question from a senior executive and respond with specific evidence rather than defensive improvisation is the single most distinguishing skill of effective boardroom presenters. This is a learnable skill, not a personality trait — it comes from thorough preparation and rehearsed responses to the most likely challenges.

How do you prepare for a board presentation when you have never presented to one before?

Three steps. First, ask someone who has presented to this specific board what they expect — every board has its own culture, pace, and level of detail appetite. Second, build a modular deck: short core presentation with a comprehensive appendix. This lets you flex based on how the meeting evolves. Third, rehearse the Q&A more than the presentation itself. Write down the five hardest questions you might be asked and prepare specific, evidence-based answers for each. The presentation is the vehicle; the Q&A is the test.

Can boardroom presentation skills be learned or are they innate?

They are entirely learnable. The executives who appear most natural in boardrooms are almost always the ones who have invested the most in structured preparation, feedback, and deliberate practice. What looks like innate confidence is typically the result of repeated exposure, well-designed slide frameworks, and a systematic approach to Q&A preparation. Nobody is born knowing how to structure a board deck or handle a challenge from a non-executive director — these are acquired skills that improve with practice.

The Winning Edge — Weekly Presentation Intelligence

Every Thursday, I share one framework, one real-world example, and one practical technique drawn from 24 years of presenting in boardrooms across three continents. Join The Winning Edge newsletter →

Not ready for the full system? Start here instead: download the free Executive Presentation Checklist — a one-page reference covering the structure, opening, and critical elements every boardroom presentation needs before you walk in.

About the Author

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds and approvals.