Quick Answer: Investor pitch deck slide order matters because venture capital partners rarely read a deck in the order you built it. They flip ahead, jump to financials, and scan the team slide before they reach the problem. The sequence that survives this pattern puts a single-line company description first, problem and market second, product and traction in the middle, and team, ask and financials as a closing block. Each slide must hold up when read out of order.

JUMP TO:

- Why VCs read pitch decks top-down, not slide-by-slide

- The slide order most founders default to (and why it fails)

- The sequence that survives a 90-second deck flip

- Slide 1: The company in one line, not the team intro

- Slides 2 to 3: Problem and market, in that exact order

- Slides 4 to 8: Story, traction, model

- Slides 9 to 12: Team, ask, financials — closing strong

- FAQ

Priya had rehearsed her Series A pitch eleven times. Twenty-three minutes, thirteen slides, a clean story arc from customer pain through to unit economics. The VC partner on the other side of the table opened the PDF, looked at slide one for three seconds, then clicked straight to slide seven — the financials. Then slide eleven, the team. Then back to slide four. Priya was still talking about the problem.

She watched the partner read her revenue projections before he knew what her company did. He read the team slide before the product. By the time he worked his way back to the problem slide, his questions were already framed by numbers he had half-interpreted without context. The narrative she had built, carefully, linearly, collapsed inside ninety seconds because the deck had not been designed to be read out of order.

The feedback afterwards was polite and fatal. “Interesting space, not sure we’ve got conviction on the wedge.” Priya rebuilt the deck the following week around a single structural premise: every slide has to make sense on its own, and the order has to survive a partner who reads it top-down and sideways at the same time. The next three pitches landed differently. The fourth became a term sheet.

If your next investor pitch is in the diary

The Executive Slide System includes a scenario playbook for investor pitch decks built around top-down reading patterns — so each slide holds up whether the partner reads the deck front-to-back or jumps straight to the ask.

Why VCs read pitch decks top-down, not slide-by-slide

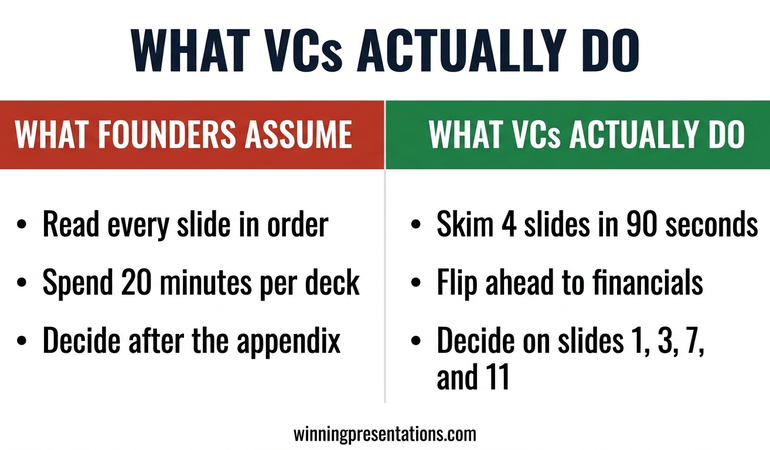

The assumption behind most investor decks is that the partner will read from slide one to the end, in the order you built it. That is not how most venture capital partners consume a deck, especially at first pass. A partner with twelve decks in their inbox on a Monday morning will open yours, scan the first slide, and then make a rapid decision about where to look next. Some will flip straight to the team slide. Some will go directly to traction. Some will scroll through all thirteen slides in under a minute, reading only the titles and headline numbers, and form a view before any detailed reading happens at all.

This behaviour is not disrespectful. It is the only way a working VC can triage dealflow. The implication for your investor pitch deck slide order is significant: the deck is not a presentation script. It is a document that will be read non-linearly by someone whose default mental model is “find the reasons to say no quickly.” Every slide has to answer a question on its own, and the sequence has to hold up when the partner flips ahead and circles back.

This matters even more in a live meeting. A partner who has already read the deck before the meeting will skip ahead while you talk. If slide seven surprises them before you have set up slide four, the narrative you rehearsed collapses. The sequence has to be robust to being read out of order, because it will be.

The founders who learn this structural rule early stop writing decks as linear stories and start writing them as indexed documents. Each slide is self-contained. The title earns its place. The headline number at the top answers the question the slide raises. The order still matters, because a VC who does read front-to-back should experience a coherent story. But no slide relies on the previous slide having been read first.

THE EXECUTIVE SLIDE SYSTEM — £39

Build a pitch deck that reads cleanly in any order a VC opens it

The Executive Slide System is 26 presentation templates, 93 AI prompts, 16 scenario playbooks, a master checklist and a framework reference. The investor pitch playbook is built around the non-linear reading patterns venture partners actually use — question-led titles, headline-first financial slides and a team slide that works whether it is read second or last. £39, instant access.

Get the Executive Slide System →

Designed for founders raising seed through Series B rounds in UK and European markets.

The slide order most founders default to (and why it fails)

The default pitch deck sequence most founders end up with looks roughly like this: title slide, team, problem, solution, how it works, market size, traction, business model, competition, financials, ask. It is a sequence assembled from fragments of advice across accelerator programmes, YC templates from 2011, and the decks of whichever founder the speaker happened to reference most recently.

Three structural weaknesses show up again and again.

Team too early. Opening with team implies the team is the core investment case. For most early-stage rounds, the team matters — but it matters in the context of the problem they are uniquely positioned to solve. Leading with team without first framing the wedge asks the partner to evaluate the founders in a vacuum. The better move is to earn the team slide by establishing the problem and the insight first.

For a deeper look at the specific mistakes founders make in deck structure, the investor pitch deck mistakes guide covers the recurring structural errors that show up across hundreds of decks.

Solution before market. Showing the product before establishing the market size means the partner is evaluating the product without a frame for how big the opportunity is. A clever product in a small market reads differently from a clever product in a £40bn market. The market size slide has to anchor the partner’s reading of everything downstream.

Financials and ask at the very end, as an afterthought. The ask is often the slide a partner most wants to see — how much, what valuation range, what runway it buys, what the next set of milestones looks like. Burying it behind competition and team slides means a partner who flips ahead finds it without any of the build-up that would make it land. The financials and ask need to be tight, headline-first, and capable of standing alone.

The failure pattern is consistent. The deck is built as a linear story, the VC reads it non-linearly, and the slides do not hold their weight individually. The fix is to rebuild the order around what survives a partner who reads the deck out of sequence.

The sequence that survives a 90-second deck flip

A working sequence for a seed-to-Series-B investor deck runs twelve to thirteen slides in the following order: company in one line, problem, market, product, how it works, traction, business model, competition, team, ask, financials, use of funds, closing milestones. The exact slide count varies, and some founders fold product and how-it-works into a single slide or split financials across two. The order is the load-bearing element.

The sequence is designed so that a partner who reads only the first three slides has a defensible first impression. A partner who skips to slide nine sees the team with context. A partner who jumps to the ask finds financials immediately before or after, so the numbers around the ask are never a separate hunt. Each of these reading paths produces a coherent picture.

The second discipline is that every slide has a question-led or claim-led title, with the answer as the headline beneath. “What problem are we solving?” with a one-sentence answer. “How big is the market?” with the number. “What traction have we built?” with the headline metric. A partner reading only the titles and the headlines should be able to form an investment thesis in ninety seconds.

For the related discipline of how much detail each slide can carry without losing the partner, the partner article on Series A pitch deck length covers the specific word and density limits that hold attention across a live reading.

If you would rather start from a ready-built template that already encodes this sequence, the Executive Slide System includes the investor pitch playbook with the full 12-slide sequence and editable templates for each position.

Slide 1: The company in one line, not the team intro

Slide one is not the place for the team. It is not the place for a mission statement. It is not the place for a logo parade of press coverage or partner institutions. Slide one has a single job: tell the partner what the company does in one line, clearly enough that a partner who reads only this slide knows whether this is in their investment thesis.

The working format is a single sentence with three components: who the customer is, what the product does, and the wedge. “We sell automated compliance monitoring to mid-market UK banks who cannot justify the headcount of a full risk team.” That is a sentence a partner can evaluate in three seconds. It frames everything that follows.

The common failure modes are predictable. A vague aspirational statement (“we are building the future of financial services”). A product description without the customer (“AI-powered compliance monitoring”). A customer description without the product (“we serve mid-market banks”). Each of these leaves the partner doing work the slide should have done.

Under the one-line description, slide one can carry the round stage, the amount being raised, and the headline traction number — one metric, not a dashboard. That is enough to frame the rest of the deck without overloading the opening.

Slides 2 to 3: Problem and market, in that exact order

Problem comes before market, and both come before solution. The sequence matters. Problem first establishes that the issue is real and painful. Market second establishes that solving it is worth capital. Only then does the solution slide carry weight.

The problem slide does its job when it describes a specific, named pain experienced by a specific, named customer segment, ideally with a dimension of cost or frequency that makes the pain quantifiable. “Mid-market UK banks spend an average of £1.8m per year on manual compliance review because existing tooling is built for tier-one institutions.” That is a problem a partner can evaluate. Generic pain statements (“compliance is complex and expensive”) leave the partner unable to judge whether the problem is worth a round.

The market slide is about size and shape, not total addressable market theatre. A partner has seen the “$50bn TAM” slide a thousand times and discounts it heavily. What they want is a bottom-up view: the number of target customers in the primary segment, the average contract value, and the implied serviceable market. A bottom-up £400m SAM reads as more credible than a top-down £50bn TAM.

The order matters because a partner who flips to the market slide before reading the problem slide interprets the market number without knowing what customer segment it covers. Putting problem first forces the partner’s attention through the pain before the numbers, which changes how the numbers read.

Slides 4 to 8: Story, traction, model

The middle block of the deck — product, how it works, traction, business model, competition — is where most decks either demonstrate that the company is working or fail to. The structural discipline is that each of these slides stands alone, and the traction slide in particular has to earn its position.

Product slide. A single screenshot or diagram that shows the core product surface. Not a list of features. Not a roadmap. The partner needs to see what the customer actually uses. If the product is not yet visual, use a two-line description of the primary workflow.

How-it-works slide. Three steps, maximum. This is the slide that converts the product into a workflow a partner can picture a customer completing. Overloading this slide with technical architecture is the most common failure mode.

Traction slide. One headline metric at the top of the slide, large font, impossible to miss. Revenue run rate, number of paying customers, growth rate — whichever number is strongest. Underneath, two or three supporting metrics. A partner who reads only the headline number should be able to judge whether the traction is material for the stage. This is the slide most often read out of order, so it has to stand alone.

Business model slide. Contract size, contract length, gross margin, CAC and LTV if you have them. Partners want to see unit economics that make sense at scale. Vague business model descriptions without numbers read as red flags at Series A and beyond.

Competition slide. Not a two-by-two matrix with your company in the top-right quadrant. That structure is tired and partners discount it. A better format is a short list of named competitors with a one-line description of why your wedge is different, honestly. Claiming no competition is worse than naming three and explaining the gap.

Slides 9 to 12: Team, ask, financials — closing strong

The closing block is where decks either convert interest into a meeting or drift into polite rejection. Team, ask, financials and use of funds need to be the strongest slides in the deck, not the afterthought they often are.

Team slide. Three to five people, maximum. Each person gets a name, a role, and one line that establishes the specific relevance to this problem. Not the full CV. Not every prior company. The relevance to this specific wedge is what the partner needs. A founder who spent eight years inside a bank building compliance tooling is the right person for this round. Say that in one line, not a paragraph.

Ask slide. Amount, valuation range if you are willing to share it, runway the round buys, and the set of milestones the round delivers. The ask is a slide the partner will flip straight to. It should read cleanly on its own. A vague ask (“we are raising a Series A”) without specifics signals a founder who has not thought through the round carefully.

For board-level context on how the structure and close of a strategic presentation land with senior stakeholders, the board presentation skills guide covers the related discipline that carries over into investor meetings.

Financials slide. Three years of projected revenue, gross profit and operating cash flow, with current-year actuals where available. Headline numbers at the top, supporting detail below. This is the slide a partner will scrutinise most. Overly optimistic hockey-stick projections signal founders who do not understand their own market. Conservative, defensible numbers signal founders who have done the work.

Use of funds and milestones. Where the money goes, what it buys, and what the business looks like at the next round. This is the slide that translates the ask into an investment story. A partner who reads the ask slide and the use-of-funds slide should understand exactly what the next eighteen months deliver and what the follow-on round looks like.

Priya rebuilt her deck using this closing block structure. The team slide was ranked second in her rehearsed sequence, but third or fourth in the positions she could not control. The ask slide held up whether read before or after the financials. The use-of-funds slide answered the question the partner asked every time. The term sheet came four weeks after the rebuild.

FOR THE NEXT INVESTOR PITCH ON YOUR CALENDAR

The complete scenario library for high-stakes investor meetings

The Executive Slide System gives you 26 templates, 93 AI prompts and 16 scenario playbooks — including the investor pitch playbook with the 12-slide sequence, question-led title patterns and the closing block structure referenced above. £39, instant access, no subscription.

If you are starting from a blank canvas and want a worked example of this sequence applied end to end, the investor pitch deck template walks through each slide position with a sample company applied.

Frequently Asked Questions

How long should an investor pitch deck be?

For a seed to Series B round, twelve to thirteen slides is the working range. Fewer than ten starts to feel under-developed. More than fifteen signals a founder who has not yet decided what matters. The length discipline is the same as the sequence discipline: each slide has to earn its place, and anything that would not survive a partner reading only the title and the headline should be in an appendix, not the main deck.

Should financials come early or late in the deck?

Late — but not at the very end. The working position is slide ten or eleven, after team and ask, before use of funds. A partner who flips ahead to the financials should find them adjacent to the ask, so the two read together as a single investment case. Putting financials first, before the problem and market, leaves the partner interpreting projections without the context to judge whether they are credible.

Why do VCs flip ahead in a deck instead of reading linearly?

Partners triage twenty to fifty decks per week at the top of the funnel. Non-linear reading is the only way to process that volume. A partner will typically scan the first slide, jump to team or traction, and then decide whether to read the rest. This is not disrespectful — it is the workflow of a busy investor. The response is not to ask partners to read your deck differently. It is to build a deck that holds up under their actual reading pattern.

What about the appendix — where does that sit?

The appendix sits after the main 12-slide sequence and exists for one reason: to answer the three or four questions a partner reliably asks in the meeting itself. Cohort analysis, sensitivity scenarios, detailed competitive breakdowns, technical architecture. Label each appendix slide clearly (A1, A2, A3) so you can jump to it on request without scrolling through thirty backup slides while the partner watches. An appendix that takes more than three seconds to navigate to is an appendix that never gets used.

Presentation playbooks, delivered Thursdays

The Winning Edge newsletter covers the structures real executives use for high-stakes meetings — investor pitches, board approvals and stakeholder buy-in. One issue per week, typically read in four minutes.

Not ready for the full system? Start here instead: download the free Executive Presentation Checklist — a one-page structural review to run over any pitch deck before it goes into a VC inbox.

Partner post: Once the slide order is right, the next structural decision is how much to put on each slide. The Series A pitch deck length guide covers the density rules that decide whether a partner reads through or skims out.

Your next step: Before you send your pitch deck to the next VC, open it in preview mode and read only the slide titles and the headline numbers at the top of each slide. If that reading on its own does not tell an investment story, the deck is not yet ready. Fix the titles and the headlines before you fix anything else.

About the Author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds and approvals.