Quick Answer: A mid-year business review presentation must do more than report what happened in the first half. It needs to explain why performance landed where it did, what that means for the second half, and what decisions the board or leadership team needs to make now. The structure that works puts honest assessment first, resets the forward view second, and closes with a clear ask — not a summary of slides already shown.

Henrik had been Finance Director at a professional services group for four years when he presented his first mid-year business review to the full board. He had prepared what he considered a thorough deck — twenty-two slides covering every line of H1 performance against budget, with detailed commentary on each variance. He had spent three evenings getting the numbers right.

Forty minutes into the meeting, the Chair stopped him at slide sixteen. “Henrik, I appreciate the detail. But I need to ask: are we on track, are we off track, and if we’re off track, what are you asking us to do about it?” Henrik realised he had prepared a report when the board needed a presentation. The data was all there. The judgement — and the ask — was entirely absent.

He asked for a brief recess, came back, and spent ten minutes giving the board the two-slide version of what he had just presented: H1 summary in plain language, three decisions required for H2. The Chair thanked him. The remaining board members engaged immediately. The revised deck he prepared for the next mid-year review was eight slides total. It covered everything that mattered.

Preparing for a board or leadership review?

The Executive Slide System includes slide templates designed for financial review, performance reporting, and strategic update contexts — structured for senior leadership audiences.

What Most Mid-Year Reviews Get Wrong

The most common structural failure in a mid-year business review presentation is the same one Henrik made: conflating a management report with a board presentation. These are fundamentally different artefacts. A management report is a record of what happened. A board presentation is a judgement on what it means and a request for a decision. Presenting the former when the audience expects the latter creates the most common type of mid-year meeting failure — a technically thorough session that leaves leadership without the clarity they came for.

The second most common mistake is the false balance between backward-looking and forward-looking content. Mid-year reviews typically spend sixty to seventy per cent of their time on H1 performance and the remainder on H2 direction. This distribution is usually the wrong way around. Board members and senior leadership have already seen monthly management information during the first half. They are not coming to the mid-year review to hear the same numbers aggregated over a longer period. They are coming to understand the forward implications of what happened and to make decisions about the second half.

A third failure pattern is variance explanation without variance significance. Presenters often explain why revenue was down 12 per cent in March — the sales cycle lengthened, a key deal slipped — without addressing what that means for the full year, what the response is, and whether the structural assumption behind the original target is still valid. The explanation answers the question “what happened?” The board’s question is “what does it mean?” These require different slide structures.

The Structure That Works: Four Sections

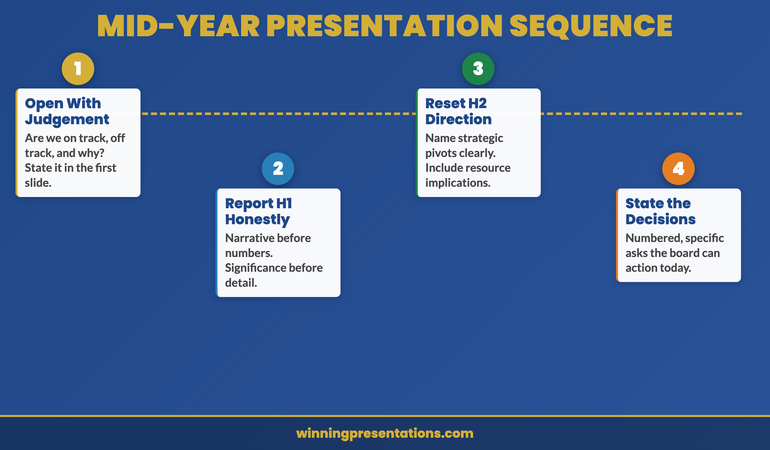

The mid-year business review presentation that serves a board or senior leadership team effectively typically contains four sections, not twenty-two slides. The discipline of the structure comes from being ruthless about what each section must do — and removing anything that doesn’t serve that function.

Section 1 — H1 Performance Summary. Three to five slides covering the most important performance dimensions: revenue versus plan, margin versus plan, key operating metrics, and any strategic milestones that were or were not achieved. The principle here is selectivity, not completeness. If you present twelve revenue lines when the board needs to understand two, you are making comprehension harder, not easier. Choose the metrics that tell the most important story.

Section 2 — What the H1 Results Mean. This section is the one most consistently missing from mid-year review decks. It takes the performance data from Section 1 and applies judgement: are the gaps structural or transient? Is the full-year target still achievable? Have any of the original strategic assumptions been invalidated by H1 performance? One to two slides. Direct language. This is the section where the presenter’s credibility is established or lost.

Section 3 — H2 Direction. What changes, and why. Revised targets if applicable, reprioritised initiatives, resource allocation decisions, any strategic pivots that H1 performance makes necessary. This section is also where the Q2 planning presentation framework overlaps — if the mid-year review triggers a formal Q3 planning cycle, the structure of that conversation follows naturally from this section.

Section 4 — Decisions Required. The most underused section in mid-year review presentations. A clear, numbered list of the specific decisions you are asking the board or leadership team to make. Not “feedback is welcome” — that is a non-ask. Specific decisions: approve revised budget, authorise additional headcount, endorse strategic pivot, confirm risk appetite. One decision per slide if they’re complex; a single decisions list if they’re straightforward. This section transforms the review from a briefing into a governance meeting.

Structure Your Review Deck for Decision-Quality Clarity

The Executive Slide System gives you slide templates and framework guides designed for the financial review and strategic update presentations that senior leadership teams require — structured for board-level comprehension, not management reporting.

- Slide templates for board review and performance reporting contexts

- Framework guides for structuring H1/H2 comparative narratives

- AI prompt cards to build strategic review decks faster

- Scenario playbooks for presenting difficult performance results

Get the Executive Slide System — £39

Designed for Finance Directors, Strategy leads, and business unit heads preparing senior leadership review presentations.

How to Report H1 Performance Without Losing the Room

The mechanics of how you present H1 performance data matter as much as the data itself. Two principles govern this section more than any others: narrative before numbers, and significance before detail.

Narrative before numbers means that every set of financial figures needs a one-sentence interpretive statement before the data appears. “Revenue for H1 came in at 94 per cent of plan. The shortfall is concentrated in one business line and reflects a single deal that slipped into H2.” That one sentence tells the board what they’re looking at before they look at it. Without it, every person in the room constructs their own interpretation of the same data simultaneously — and you spend the next eight minutes responding to four different reads of the same chart.

Significance before detail means leading with the implications rather than the components. For a variance that matters, present the significance first (“this puts the full-year target at risk if the trend continues”) and the detailed breakdown second. Audiences who understand why a number matters are far better equipped to process the detail than audiences who are still constructing their own significance judgements while you’re explaining line-item variances.

This approach aligns with the principles behind effective quarterly forecast presentations — the same narrative-first logic applies whether you’re presenting one quarter or six months of data. See also the team performance review presentation framework for how to apply the same structure to operational rather than financial metrics.

Resetting Strategic Direction for H2

The H2 direction section of a mid-year business review presentation is where most presenters underestimate the audience’s tolerance for directness. Boards and senior leadership teams do not need protecting from difficult strategic realities. What they cannot tolerate is ambiguity about what the presenter actually thinks.

If H1 performance has invalidated one of the strategic assumptions behind the annual plan, the H2 direction section is the place to say so clearly. “Our original assumption was that the enterprise segment would accelerate in H2 following the product launch. The H1 data suggests that assumption was optimistic. We are recommending a revised focus on the mid-market segment where conversion times are shorter and our H1 win rate was stronger.” That is a strategic pivot. Name it as such. Don’t bury it in hedging language.

The H2 direction section should also address resource implications directly. A strategic reset without resource implications is a strategic statement, not a plan. If the H2 pivot requires reallocating budget, deferring a project, or hiring in a specific area, those decisions need to appear in the deck — not be left as questions for a follow-up conversation. Leaving resource implications unresolved is the most common reason mid-year reviews generate a second meeting rather than decisions.

If you’re building the deck for a board or C-suite review, the Executive Slide System includes templates specifically structured for performance reporting and strategic review contexts.

The Ask: What Decisions Does the Board Need to Make?

The decisions-required section is the most structurally important part of a mid-year business review presentation, and the most commonly omitted. Its absence turns a governance meeting into a briefing session — the board receives information but doesn’t exercise judgement, which defeats the purpose of convening them.

A well-constructed decisions list is specific, bounded, and actionable within the meeting. It does not contain questions that require further investigation before a decision can be made — those belong in a pre-read or a follow-up. It contains decisions that the board has enough information to make based on what they’ve just seen in the preceding sections of the review.

The format that works most consistently is a numbered list, one decision per item, with a brief rationale attached to each. “Decision 1: Approve a revised full-year revenue target of £X, reflecting the H1 shortfall and revised H2 conversion assumptions. Rationale: the original target is no longer achievable without material upside on the deal that slipped; the revised target reflects the most credible H2 outlook.” The board can approve, reject, or request modification. That is a governance action. A vague “discussion of performance challenges” is not.

The competitive win-back presentation uses a similar bounded-ask principle — in both contexts, the precision of the ask determines whether the meeting produces a decision or a deferral.

From Performance Data to Board-Ready Presentation

The Executive Slide System gives you framework guides and scenario playbooks for translating complex performance data into the structured, decision-focused format senior leadership teams require.

Explore the Executive Slide System

Designed for senior professionals presenting to boards, executive committees, and investment committees.

Common Structural Mistakes and How to Avoid Them

Several structural patterns in mid-year business review presentations consistently undermine otherwise solid content. Recognising them in advance is more effective than diagnosing them after a difficult meeting.

Too many slides on context that the board already has. A mid-year review is not an onboarding session. Slides covering business model, market overview, and strategic objectives that the board approved in January are filler in a mid-year review. They signal that the presenter is either filling time or lacks the confidence to start directly with performance. Cut context to a single orientation slide if the board composition has changed, or omit it entirely if the audience is consistent.

Variance explanation without variance judgement. “Revenue was down 8 per cent because of a softer market environment in Q2” is an explanation. “Revenue was down 8 per cent, and based on our current pipeline we expect H2 to recover approximately half that gap, which means the full-year target is at risk by approximately 4 per cent” is a judgement with a forward implication. Boards need both; most mid-year decks only provide the former.

Ending on a summary rather than an ask. The final slide should not be “Key Takeaways from H1.” It should be “Decisions Required.” A summary restates what the audience just heard. A decisions slide asks them to act on it. If the meeting ends on a summary, the board leaves feeling informed but not empowered. If it ends on a decisions slide, they leave with clarity about what they did and what happens next.

Frequently Asked Questions

How many slides should a mid-year business review presentation contain?

For a board or senior leadership audience, eight to twelve slides is typically the right range. More than fifteen slides suggests the presenter hasn’t done the work of deciding what matters most. The discipline of reducing a full H1 performance record to twelve focused slides is itself a demonstration of strategic judgement. If supporting detail is essential, it belongs in an appendix that the board can reference rather than in the main deck.

What should go in the appendix of a mid-year review deck?

The appendix of a mid-year business review presentation is for detailed breakdowns that board members may want to reference during discussion — divisional P&Ls, segment-level variance tables, pipeline analysis — but that would slow the main narrative if included in the body of the deck. The rule is: if you need it to make the decision, it belongs in the main deck. If you might need it to answer a question, it belongs in the appendix.

How do you handle a mid-year review when performance is significantly below plan?

Present it directly. The most damaging presentation approach when performance is below plan is to soften, contextualise, or defer the difficult news. Boards have seen every version of that approach and it erodes credibility faster than the performance gap itself. Lead with the honest assessment, explain the root cause analysis, and come prepared with a specific H2 recovery plan and the decisions needed to execute it. Credibility in difficult performance conversations comes from candour and preparedness, not from minimising.

The Winning Edge Newsletter

Weekly presentation strategies, frameworks, and analysis for senior executives and finance professionals. Practical — not theoretical.

Free resource: Download the Executive Presentation Checklist — a pre-presentation reference for board and leadership review contexts.

About Mary Beth Hazeldine

With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, Mary Beth Hazeldine is Owner and Managing Director of Winning Presentations. She advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic review cycles. View services | Book a discovery call