Quick answer: The 10-minute investor pitch outperforms the 30-minute version in almost every Series A and Series B partner meeting. Investors are running an evaluation, not a comprehension exercise — they need enough to decide whether to take it to a partner discussion, not enough to underwrite the round in the room. The structure that holds in 10 minutes has 10 slides: cover, problem, solution, market, traction, business model, defensibility, unit economics, team, ask. Each slide gets roughly 50 to 60 seconds. Founders who try to fit a 12-slide deck into 10 minutes end up rushing the slides that matter most. Founders who write the deck for 10 minutes from the start spend the saved time on Q&A — which is where the real evaluation happens.

JUMP TO:

Marcus, a second-time founder, walked into a Tier 1 partner meeting in Mayfair with a 32-slide deck and a 28-minute presentation. The partners were polite, the questions were thin, and the meeting ran twelve minutes over the scheduled hour. He left feeling that the depth of the deck had earned the depth of the questions. The reality, relayed two weeks later when the term sheet did not arrive, was that the partners had decided in the first nine minutes and spent the next nineteen waiting for him to stop talking. The depth of his deck had buried the strongest moment of the pitch under twenty-three slides of supporting material the partners had not asked for.

The pattern is consistent across partner meetings at Series A, Series B, and most growth-stage rounds. The investor decision is made in a window that closes well before the founder reaches their conclusion slide. After that window, the rest of the pitch has only the power to weaken the case — additional slides surface additional risks, supporting material introduces additional questions, and the founder’s voice loses the rhythm that pulled the partners in. The 10-minute pitch is not a stripped-down version of the 30-minute pitch. It is a different deck, written for a different purpose: to win the right to a partner discussion, not to substitute for one.

This piece walks through the 10-slide structure that fits cleanly into 10 minutes, the timing discipline that makes it land, the slides that founders most often try to keep when they should cut, and the use of the saved time. The principles apply to most Series A and Series B partner meetings; they apply with minor modifications to demo days, family-office meetings, and corporate-venture pitches. The shape — 10 slides, 10 minutes, 50 to 60 seconds per slide — is the part that holds.

Want a one-page reference for the 10-slide pitch structure?

The Pitch Deck Structure Checklist is a free one-page reference covering the slide-by-slide structure that fits into a 10-minute investor pitch — what each slide has to answer, what to cut, and where founders most often run over time.

Why length beats content in investor rooms

The instinct that more content makes a stronger case runs counter to how investor evaluation actually works. A partner meeting at Series A is an act of triage. The partners are not deciding whether to fund the company that day; they are deciding whether the case is worth a partner discussion the following week. That decision is binary, and it gets made on a small handful of signals: does the founder have a clear thesis, does the firm have credible traction, are the unit economics directionally workable, is the moat plausible, is the team operator-led. A 10-minute pitch can deliver all five signals if it is built for that purpose. A 30-minute pitch can deliver the same five and add fifteen minutes of additional surface that gives the partners new doubts.

The second reason length matters: a partner who has been listening for twelve minutes is in a different cognitive state from a partner who has been listening for twenty-five. After twelve minutes, the partner is still engaged, still tracking the argument, still forming questions that test the thesis. After twenty-five, the partner is fatigued, less generous in interpretation, and more likely to anchor on whatever doubt has surfaced — even doubts the founder could comfortably address with another two minutes. The deck that runs short ends on a strong frame. The deck that runs long ends on whatever the audience was thinking when fatigue set in.

The third reason is structural. The 10-minute version forces founders to write a tighter pitch. Every minute saved is a minute the deck cannot afford to spend on a slide that does not earn it. The discipline of writing for 10 minutes catches a lot of weak slides that survive a 30-minute draft because the deck has room for them. Founders who insist they cannot make their case in 10 minutes are usually correct — and that is the diagnostic. The case that cannot fit in 10 minutes usually has a structural weakness the longer version is hiding. Tightening to 10 forces the rewrite. For more on the slide-by-slide structure that supports a tighter deck, see our VC pitch deck template for 2026.

The 10-slide format that fits in 10 minutes

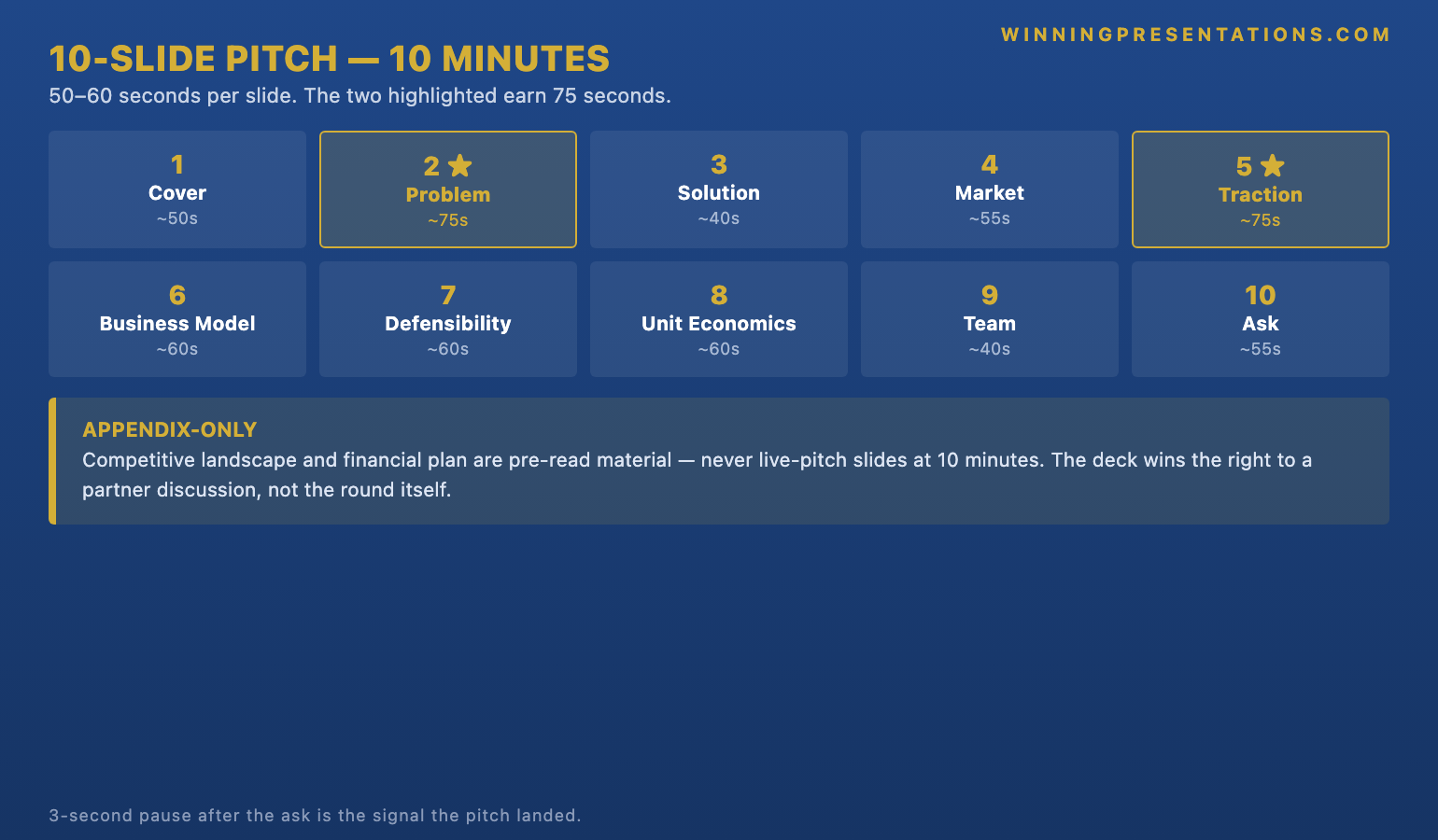

The 10-slide format runs as follows. Slide one is the cover with the company line. Slide two is the problem — specific, with a named buyer and a named consequence. Slide three is the solution, with one screenshot and one outcome metric. Slide four is the market, sized bottom-up, with the segment the firm is targeting first explicitly drawn. Slide five is the traction slide, leading with the metric that has moved fastest. Slide six is the business model — pricing, ACV, sales cycle. Slide seven is the defensibility slide. Slide eight is unit economics. Slide nine is the team. Slide ten is the ask: round size, valuation expectation, use of funds in three lines.

This is the 12-slide structure compressed in two specific places. The competitive landscape and the financial plan have been collapsed into other slides — the competitive position now lives inside the defensibility slide, and the financial plan is implied by the unit economics and the use-of-funds lines on the ask slide. Those are the two slides founders most often want to keep. Both are worth keeping in the appendix; neither is worth keeping in the 10-minute pitch. The competitive landscape, in particular, is almost always better delivered as a Q&A response than as a slide — the founder who can articulate competitive position from memory in answer to a partner’s question reads as more credible than the founder who points at a positioning map.

The order is the same as the 12-slide version through slide six, then tightens. The defensibility slide moves from position seven to position seven — unchanged in the order, but now carrying the load that used to be split with the competitive landscape slide. The unit-economics slide stays in position eight. The team slide moves up to position nine, before the ask, because the ask is the strongest closing position and team is the strongest credibility position before the close. The ask is always last. Putting the ask anywhere else interrupts the rhythm that the deck has been building. Founders who reorder these slides on instinct usually weaken the close.

Get the 10-slide structure that fits in a 10-minute partner meeting.

The Pitch Deck Structure Checklist is a free one-page reference for the slide-by-slide structure of a 10-minute investor pitch. What each slide has to answer, what to cut, and where founders most often run over time.

- One-page slide-by-slide structure for a 10-minute investor pitch

- Per-slide timing target (50 to 60 seconds per slide)

- What to cut when compressing from 30 minutes to 10

- Free download — instant access

The timing discipline: 50 to 60 seconds per slide

The 10-minute pitch divides into roughly 50 to 60 seconds per slide, with two slides — the problem and the traction — getting closer to 75 seconds, and the solution and the team getting closer to 40. That distribution is not arbitrary. The problem slide is where the partner forms the initial frame of the firm; spending an extra 20 seconds on a precisely named buyer and a precisely named consequence pays back across the rest of the deck. The traction slide is where the partner forms the initial belief that the firm is working; spending an extra 20 seconds on the cohort detail and the trajectory pays back in the questions the partner does not feel the need to ask later. Compressing those two slides to save time on others weakens the deck.

The timing discipline is taught by rehearsal, not by reading. Founders who write the deck and rehearse it twice run over by 4 to 6 minutes consistently. Founders who rehearse the deck eight to twelve times, with a stopwatch, hit the 10-minute mark within 30 seconds. The mismatch between draft length and rehearsed length is one of the more reliable signals of how much rehearsal a founder has done. Partners cannot tell from the deck whether the founder has rehearsed; they can tell from the timing. A deck that lands at 9 minutes 40 seconds with no visible rushing reads as a founder who has done the work. A deck that lands at 14 minutes with the founder visibly racing through the unit-economics slide reads as a founder who has not.

The harder rehearsal discipline is timing each slide individually rather than the deck as a whole. A founder who hits 10 minutes overall but spends 90 seconds on the team slide and 25 seconds on the unit-economics slide has built a different pitch than the structure intends. The slide-level stopwatch test catches that imbalance. Each slide needs its own target time, each rehearsal needs to record actual time per slide, and the variance between rehearsals needs to drop to under five seconds per slide before the pitch is meeting-ready. That is more work than most founders expect; it is also the single most reliable predictor of which decks land. For a closely related discipline on rehearsing under pressure, see the Executive Slide System.

What to cut when you compress from 30 minutes to 10

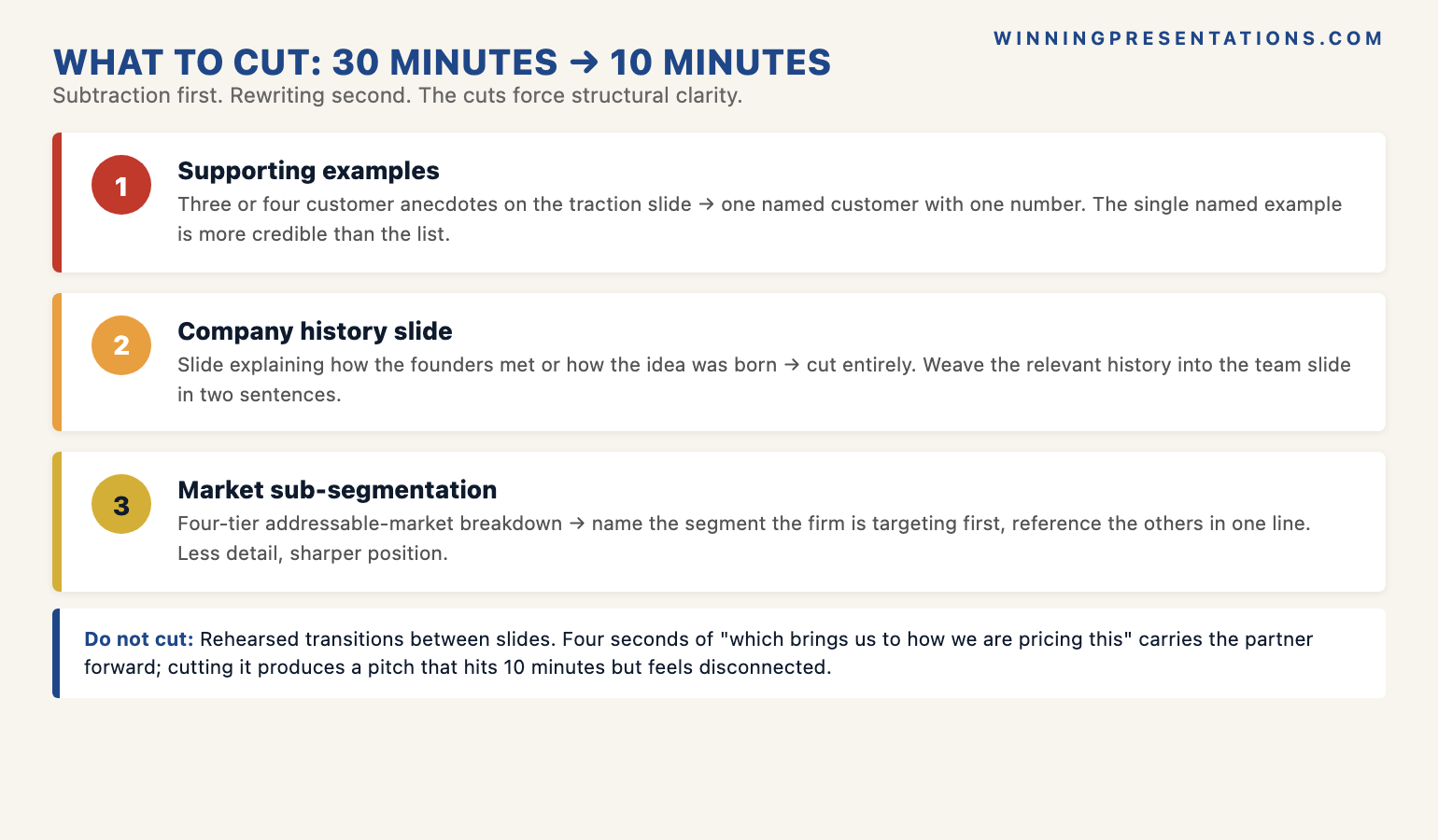

The compression is mostly subtraction, with a small amount of rewriting. Three categories of content come out. First, supporting examples: most pitches have three or four customer anecdotes on the traction slide; the 10-minute version has one, named, with one number. Second, the company history: most pitches have a slide explaining how the founders met or how the idea was born; the 10-minute version cuts the slide entirely and weaves the relevant history into the team slide in two sentences. Third, the market sub-segmentation: most pitches break the addressable market into four tiers; the 10-minute version names the segment the firm is targeting first and references the others in one line.

The rewriting is harder. Every paragraph the founder narrates over the slides needs to drop in length by 30 to 40 per cent without losing its load-bearing claim. That cannot be done by speaking faster — it has to be done by rewriting the script. The pattern that works: write the 30-minute script, mark every sentence as load-bearing, supportive, or transitional, and cut the supportive and transitional sentences ruthlessly. What is left should still hold the argument. If it does not, the load-bearing sentences themselves need rewriting. The exercise usually takes longer than founders expect; it is also where the deck gets sharper, because the rewrite forces clarity that the longer version did not require.

One thing not to cut: rehearsed transitions between slides. The 10-minute pitch lives or dies on rhythm, and rhythm depends on transitions. A rehearsed transition that takes four seconds to deliver — “which brings us to how we are pricing this” — is worth more than the eight seconds it appears to cost, because it carries the partner’s attention forward without the brief lapse that an unrehearsed transition introduces. Founders who cut transitions to save time end up with a pitch that hits 10 minutes but feels longer because the slides feel disconnected. The transitions are part of the structure, not an addition to it.

Using the saved time: Q&A is where decisions happen

The 20 minutes saved by compressing the pitch are not lost — they are returned to Q&A, which is where most partner meetings actually decide. A partner who has 20 minutes of unstructured questions is testing the thesis in ways the deck cannot anticipate: probing the moat, stress-testing the unit economics, asking about the team’s prior context, surfacing the assumptions in the financial plan that the founder has not yet articulated even to themselves. That is the meeting. The deck is the warm-up. The founder who has rehearsed for 30 minutes of presenting and 10 minutes of Q&A is mis-allocated; the founder who has rehearsed for 10 minutes of presenting and 30 minutes of Q&A is calibrated to where the meeting actually weighs.

The Q&A discipline is different from the deck discipline. Q&A rewards short answers, named evidence, and the willingness to say “we do not know yet but here is the analysis we will run”. A founder who has prepared sixty short answers to likely questions, mapped to the slides those questions will follow, walks into the room with a different level of preparation than the founder who has rehearsed the deck six times and trusted Q&A to take care of itself. The 10-minute pitch is the format that forces the founder to do the Q&A preparation, because the time has been freed up for it. The 30-minute pitch lets the founder skip the Q&A preparation, and the meeting then runs short on the most important part.

If you want the underlying slide-by-slide template library:

The Executive Slide System is a structured library of 26 slide templates, 93 AI prompts, and 16 scenario playbooks for board-ready executive slides — including slide structures for the 10-minute investor pitch format. £39, instant download.

The third use of saved time is silence at the end. A 10-minute pitch that finishes with the ask slide and is followed by a 3-second pause before the partners speak reads as a pitch that has fully landed. A 28-minute pitch that finishes 2 minutes over and is followed by an immediate question reads as a pitch the partners are eager to interrupt. The 3-second pause is a structural artefact of the 10-minute format; it is also one of the more underrated signals that the pitch has worked. Founders who fill the pause with additional content lose the moment. Founders who hold the pause and let the partners speak first read as composed and have more control over the conversation that follows. For more on the underlying slide structure, see our pitch-deck template for startups.

Frequently asked questions

Is 10 minutes really enough for a Series A pitch?

For the partner-meeting pitch, yes. The 10 minutes is not the whole meeting — it is the presentation portion of a meeting that runs 45 to 60 minutes total. The remaining time is Q&A, which is where the substantive evaluation happens. Founders who insist on 25 to 30 minutes of presenting are usually compressing Q&A to under 20 minutes, which is the wrong trade. Investors decide on the strength of their unstructured questions and the founder’s responses, not on the depth of the prepared narrative. The 10-minute structure is calibrated for the meeting as it actually runs, not for the meeting as the founder imagines it.

What about demo days where I have only 5 minutes?

The 5-minute version is a different pitch with a different purpose: demo days are not partner meetings. Demo-day pitches are written to win a follow-up meeting, not to advance toward a term sheet. The 5-minute structure compresses the 10-slide format into 6 slides — cover, problem, solution, traction, ask, contact — and drops the unit-economics, business-model, defensibility, and team slides. Those slides are best handled in the follow-up meeting where 10 minutes is available. Trying to keep all 10 slides in 5 minutes produces a pitch that feels rushed and lands flat. The 5-minute pitch is its own form, not a compressed version of the 10-minute pitch.

What if the partner asks me to skip slides?

Skip them. A partner who asks the founder to skip the market slide and go straight to traction is signalling what they want to hear; the founder who insists on walking through the market slide anyway has misread the room. The 10-slide structure is a default, not a contract. If the partner has done their homework, the early slides become redundant; the founder who can pivot to slide 5 in answer to the request and continue without losing rhythm reads as composed and well-prepared. The founder who hesitates or insists on the original order reads as scripted. Build the pitch so that any slide can be the entry point if the partner directs it there.

Should I send the deck before the meeting or only present it in the room?

Send a version before the meeting. The pre-read deck and the live-pitch deck are not the same artefact. The pre-read can run to 16 to 18 slides because the partner reads it at their own pace; the live pitch holds at 10 because the partner is listening. Sending only the live deck produces a pre-read that the partner finds thin; sending the pre-read version as the live deck produces a presentation that runs 25 minutes. The two artefacts serve different purposes and most experienced founders prepare both. The discipline of building the live-pitch deck for 10 minutes is independent of how thorough the pre-read deck is.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate decks committees back from decks they defer. Subscribe to The Winning Edge →

Not ready for the full Executive Slide System? Start here instead: download the free Investor Pitch Deck Checklist — a one-page reference for the slide-by-slide structure that goes into a 10-minute partner meeting.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.