Quick answer: The mid year review presentation slide senior leaders build last is the H1 verdict slide — the single page that names where the year stands, what it means for H2, and what the leader is asking the room to do about it. Most leaders build it last because it is the hardest slide to write before the analytical work is finished. The leaders who win the room build it first, in draft, and let the rest of the deck argue for or against the verdict the slide already names. The four-line verdict, the named delta against the plan, the explicit H2 ask, and the proposer’s own exposure on the next-six-months commitments are what separates the H1 review the committee approves from the one it absorbs and forgets.

JUMP TO:

- Why the verdict slide is the slide senior leaders build last

- The four-line verdict and the delta against plan

- The explicit H2 ask, not the implicit one

- The leader’s own exposure on the next six months

- The verdict-first diagnostic for the day before the review

- One thing to do before the next mid-year review

- Frequently asked questions

In June 2014 I sat in on a mid-year review at a European insurer where the head of one of the business lines was presenting the H1 result to the group executive committee. The room was the standard top-floor boardroom of a building in central Munich; eight people around the table, the group CEO at the head, the CRO and CFO either side of him, the head of strategy taking notes at the corner. The business-line head walked in with a 32-slide deck. Slide one was a clean cover with the line’s name and the half-year period. Slides two through twenty-eight were the analytical journey: market context, channel performance, claims development, expense ratios, distribution productivity, a competitor benchmark, four pages of bridge analysis explaining the variance against the plan. Slide twenty-nine was the verdict. The CEO read the cover, leafed forward to slide twenty-nine, read the verdict in twenty seconds, closed the deck, and asked one question: “What are you asking us to do about H2.” The business-line head had not written the H2 ask anywhere in the deck. He extemporised an answer for ninety seconds; it was reasonable; it was not the answer the CEO needed in writing for the rest of the committee to engage with. The review ended cordially. The H2 plan was deferred to a follow-up session two weeks later. Two of the proposed H2 initiatives never recovered the air they had lost in that twenty-minute meeting.

(This article was created with AI assistance; all stories and insights are based on 35 years of real client work.)

This piece walks through the slide senior leaders consistently build last in a mid year review presentation — the H1 verdict slide — and the reason that ordering is the single most expensive mistake in the H1 deck. The verdict slide is hard to write before the analytical work is finished because the analytical work is supposed to produce the verdict. That logic is the trap. The verdict is a leadership statement, not an analytical output. It is the leader’s read of where the half-year landed, framed in terms the committee can act on, and the analytical journey in slides two through twenty-eight exists to support it — not the other way round. Senior leaders who build the verdict first, in draft, on a blank slide on a Tuesday afternoon, write a different deck. The deck argues for the verdict the slide already names, the analytical pages serve the argument, and the H2 ask becomes the natural close because the verdict made it inevitable. Senior leaders who build the verdict last write the H1 deck I watched fail in 2014.

Before the next mid-year review, a structural check on the verdict slide is worth fifteen minutes.

The Executive Presentation Checklist walks through the openings senior committees actually engage with — the named verdict, the delta against plan, the H2 ask, and the proposer’s own exposure. Free download, no email gate.

Why the verdict slide is the slide senior leaders build last

The verdict slide gets built last for a reason that looks rational from the inside and is structurally wrong from the outside. From the leader’s perspective, the H1 review is a piece of analytical work: the team has been pulling channel numbers for three weeks, the finance team has rebuilt the bridge against the plan, the strategy team has drafted the market-context pages, and the verdict is supposed to emerge from the analysis. Writing the verdict before the analysis feels like guessing the conclusion of an investigation. Most leaders refuse to do it. They wait until the bridge analysis is final, the channel pages are signed off, and the competitor benchmark is in — and then they sit down to write the verdict, often the evening before the committee, often in the last forty minutes before the deck goes to print. The verdict ends up as a tired four-bullet summary of the analytical pages the leader is already deck-fatigued from reading. The committee opens the deck the next morning and reads exactly that: a tired summary of pages the committee was not going to read in detail anyway.

The structural problem with the build-last approach is that the H1 verdict is not analytically generated. It is leadership-generated. The bridge analysis tells the leader what happened against the plan; it does not tell the leader what to do about it, what to escalate, what to absorb, what to flag to the CRO, or what to recommend changing in H2. Those are leadership reads, made by the leader, before the analysis is finished, and then pressure-tested against the analysis as it lands. The leader who has the draft verdict on a sticky note on a Tuesday afternoon in week one of the H1-close runs the analytical work differently from the leader who waits for the analysis to write the verdict for them. The first leader uses the analysis to confirm or correct a hypothesis. The second leader uses the analysis to construct a hypothesis after the fact, under deadline pressure, and the result is the four-bullet summary the committee will read in twenty seconds and forget by the end of the meeting.

The German insurance review in 2014 was a textbook build-last failure. The business-line head’s verdict on slide twenty-nine read, paraphrased: H1 was broadly in line, claims a little high, channel mix shifted toward broker, expense ratio under control, momentum into H2 is positive. Every word was defensible against the analytical pages that preceded it. None of it was a verdict the CEO could act on. The CEO did not need a summary; he needed to know which of those five observations the line head considered the most important, which one was a leadership signal rather than a data point, and what the line head wanted the committee to do as a result. The verdict slide had been built last, from the analytical pages, and it inherited the analytical pages’ lack of leadership stance. The CEO read it accurately and asked the question the slide should have answered.

The four-line verdict and the named delta against the plan

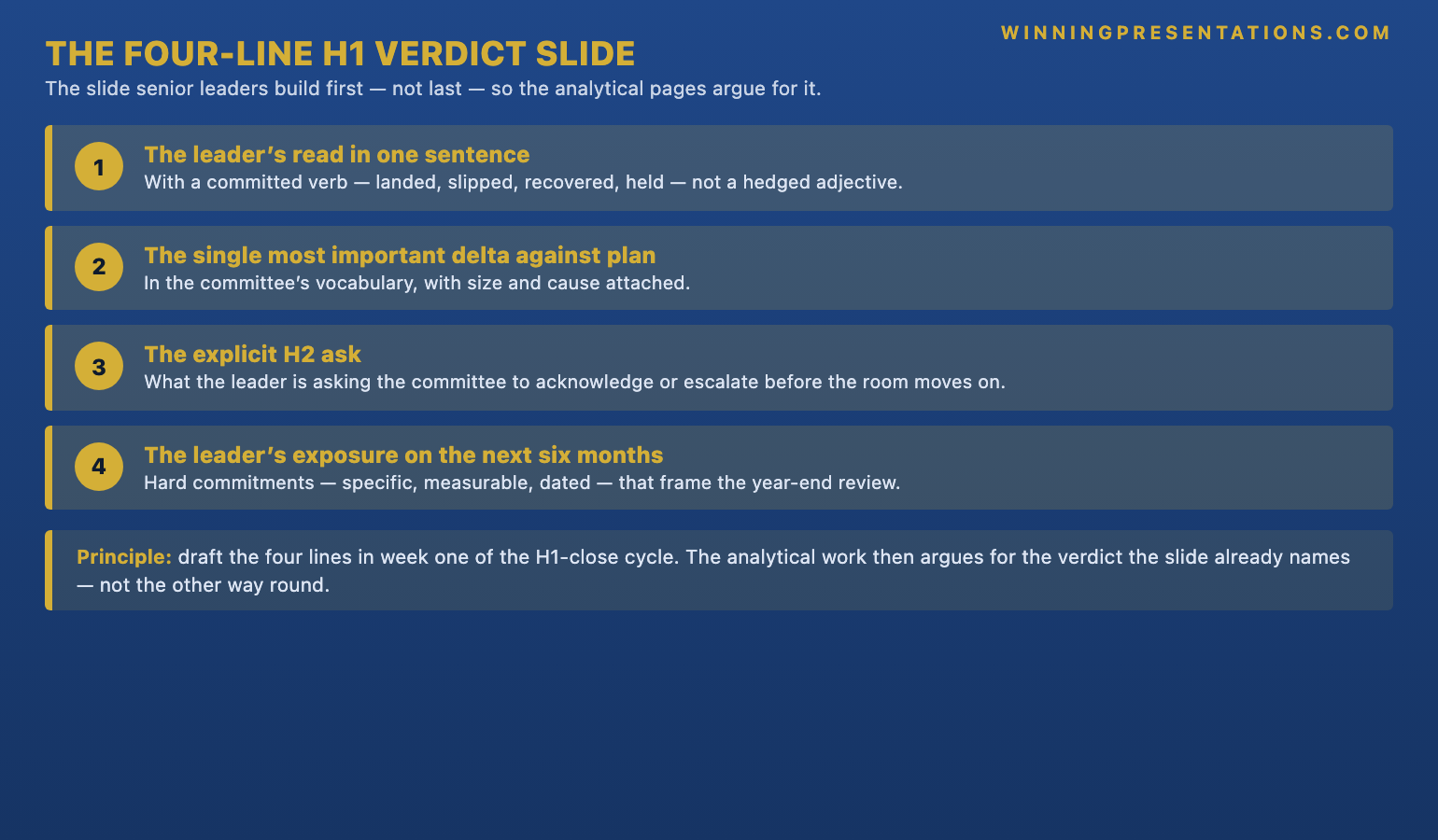

The verdict slide that earns committee engagement is four lines long. Line one names the leader’s read of the half-year in one sentence, with the strongest verb the leader is willing to put their name against — landed, slipped, recovered, compounded, held. Line two names the single most important delta against the H1 plan, framed in the committee’s vocabulary, with the size of the delta and the cause attached. Line three names what the leader is asking the committee to acknowledge or escalate before the room moves on. Line four names the leader’s own exposure on the next six months — the personal commitment that becomes harder to honour if the verdict is wrong. Four lines, on slide three, in 14-point type, with no further analytical content competing for the committee’s attention. The remaining pages of the deck exist to evidence the four lines, not to compete with them.

The discipline of the four-line verdict is the discipline of choosing what not to say. Most H1 reviews fail because the leader cannot commit to one delta-against-plan as the most important. The instinct is to list all the deltas, balanced for political coverage of every function in the business line. The committee reads the balanced list as evasion. The committee wants the leader’s read on which delta the leadership team is actually managing through H2, which one is signal and which one is noise, and which one the leader would mention if the CEO stopped them in the corridor afterwards. A four-line verdict that names one delta with conviction reads as leadership. A balanced four-bullet summary of every delta reads as a status report. Status reports get absorbed; verdicts get acted on. The same data lands differently depending on whether it is framed as a status report or a verdict.

The named delta against plan also needs the cause attached. Claims a little high is a status report. Motor claims ran 4.2 points above plan, driven by a step-change in the average severity of bodily-injury settlements in the southern German states, identified mid-Q2 and now reflected in the H2 underwriting guidance the underwriting committee approved on 4 June is a verdict. The committee reads the difference in two seconds. The first reads as a leader who has noticed something. The second reads as a leader who has noticed something, understood it, taken action, and is reporting the action alongside the observation. Committees approve H2 plans from leaders who already took the H1 action; they defer H2 plans from leaders who are reporting H1 observations and waiting for the committee to tell them what to do about them. The 3Ps framework for executive presentation coaching walks through the upstream rehearsal version of this discipline, where the verdict is pressure-tested against the named delta in the week before the committee.

The H1 verdict slide is faster to write when the slide structure is already built.

The Executive Slide System is the slide library senior professionals use to build the four-line verdict, the named-delta H1 bridge, the explicit H2 ask, and the proposer-carries-the-downside commitment page — without rebuilding the structure from scratch every review cycle. Built on 24 years in corporate banking and 16 years coaching senior professionals across financial services, insurance, consulting, and technology.

- 26 Executive Templates — including verdict slides, bridge-against-plan layouts, and H2-ask formats senior committees actually engage with

- 93 AI Prompts — rewrite the four-line verdict, the named-delta sentence, and the H2 ask in the leader’s own voice in fifteen minutes

- 16 Scenario Playbooks — including the mid-year review, the H1 board update, the half-year strategy refresh, and the next-six-months commitment page

- 7 Checklists — the verdict-first diagnostic, the H2-ask pressure test, and the next-six-months exposure check

- Instant download, lifetime access — usable across every review cycle, not just the one in front of you now — £39

The explicit H2 ask, not the implicit one

The second slide senior leaders build late, often because they assume the committee will infer it from the verdict, is the explicit H2 ask. The H2 ask is the single page that names what the leader wants the committee to approve, change, or escalate for the second half of the year, with a specific decision attached. Continue the H2 plan as originally approved is an H2 ask. Reallocate £6m of the H2 distribution budget from broker to direct, with the reallocation decision required by end of this session is an H2 ask. The team is broadly comfortable with the H2 trajectory and will keep the committee informed is not an H2 ask. It is a status update masquerading as an ask. Senior committees read status updates as deferrals: the leader has come to inform, not to decide, and the committee will return the implicit reciprocity by not engaging with the substance. The H2 ask either commits the leader to something the committee will be asked to evidence next quarter, or it does not exist.

The reason the H2 ask is so consistently missing or weak is that the leader has not made the decision themselves before walking into the committee. The leadership team has discussed three options for the H2 plan. The line head’s view leans toward option two but is not fully formed. The instinct, in the H1 deck, is to present the three options to the committee, lay out the trade-offs, and let the committee pick. The committee declines that invitation reliably. The committee’s role is to approve the line head’s recommended option, not to choose between options on the line head’s behalf. A leader who arrives with three options has not yet done the work to choose; the committee reads the un-chosen options as un-finished leadership, and defers the decision back to the line head with a polite suggestion to come back when the recommendation is firmer. The deferral costs the line head three or four weeks of momentum on whichever option they would have ended up recommending anyway.

The fix for the explicit H2 ask is mechanical. Two days before the committee, the line head writes one sentence on a sticky note that names the H2 recommendation, the size of the change against the original plan, the decision the committee is being asked to make, and the date by which the decision is required. The sentence is then read aloud to one colleague from outside the line who has the seniority to push back on it. If the colleague reads the sentence and immediately asks “what about option three”, the leader has not done enough work. If the colleague reads the sentence and says “I’d ask whether you’ve carried the implication through to the renewal volumes”, the leader has done the work and now has a specific risk to attach to the recommendation. The discipline takes about thirty minutes and is the difference between an H2 ask that gets the committee’s decision in the same session and an H2 ask that triggers a polite deferral and a fortnight of slipped momentum. The structure boards engage with on update-and-decide sessions covers the same dynamic at the board level, where the implicit H2 ask is even less forgiving.

If the H1 review is the prelude to a buy-in fight on the H2 plan, the structural method matters.

The Executive Buy-In Presentation System is the self-paced programme senior professionals use when the mid-year review is the warm-up to a contested H2 decision — reallocations, hiring freezes, channel shifts, distribution overhauls. 7 modules, no deadlines, no mandatory session attendance. Optional live Q&A calls, fully recorded. Self-paced with monthly cohort enrolment. Lifetime access to materials. £499.

The leader’s own exposure on the next six months

The third slide senior leaders build late is the next-six-months exposure page — the slide that names the leader’s own commitments for H2, in specific terms, with the conditions under which those commitments become harder to honour. The exposure page is uncomfortable to write because it names what the leader has promised the committee they will deliver, in a form the committee can hold against them at the next session. The instinct is to keep the commitments soft — focus on margin recovery, continue to improve channel mix, build out the new product capability. Soft commitments are non-commitments. The committee reads them that way. The leaders who win the room write the commitments hard: deliver the H2 motor combined ratio at or below 98.5%, complete the broker-to-direct reallocation within the existing H2 expense envelope, ship the new product capability with at least one signed pilot client by end of October. Each commitment is specific, measurable in the committee’s vocabulary, and dated. Each commitment is also implicitly the leader’s end-of-year operating commitment, made visible to the committee in writing.

The exposure page does not work as a backwards-looking accountability tool. It works as a forward-looking trust signal. The leader who arrives with three hard commitments for H2 has signalled to the committee that they have thought through the operational reality of delivering each one, that they are willing to be measured against them at year-end, and that the H2 plan is therefore worth the committee’s approval at the H1 session rather than at a follow-up session in October. Committees approve H2 plans against the leader’s personal credibility; the exposure page is the page where that credibility either gets put on the table or gets withheld. Withholding it is a structural choice the committee notices.

The exposure page also serves a downstream function the leader rarely thinks about during the H1 review itself. The same three hard commitments, written into the H1 deck and accepted by the committee in June, become the opening structure of the H2 review in December. The leader who wrote hard commitments in June walks into December with a deck that already has its scoring rubric defined. The leader who wrote soft commitments in June walks into December needing to reconstruct what the H2 plan actually was, defend an interpretation of vague H1 commitments against the committee’s memory of them, and somehow translate the analytical results into a verdict the committee will engage with. The H1 exposure page is the leader’s gift to themselves at year-end. Writing it well in June saves about four meetings of friction in December.

The verdict-first diagnostic for the day before the review

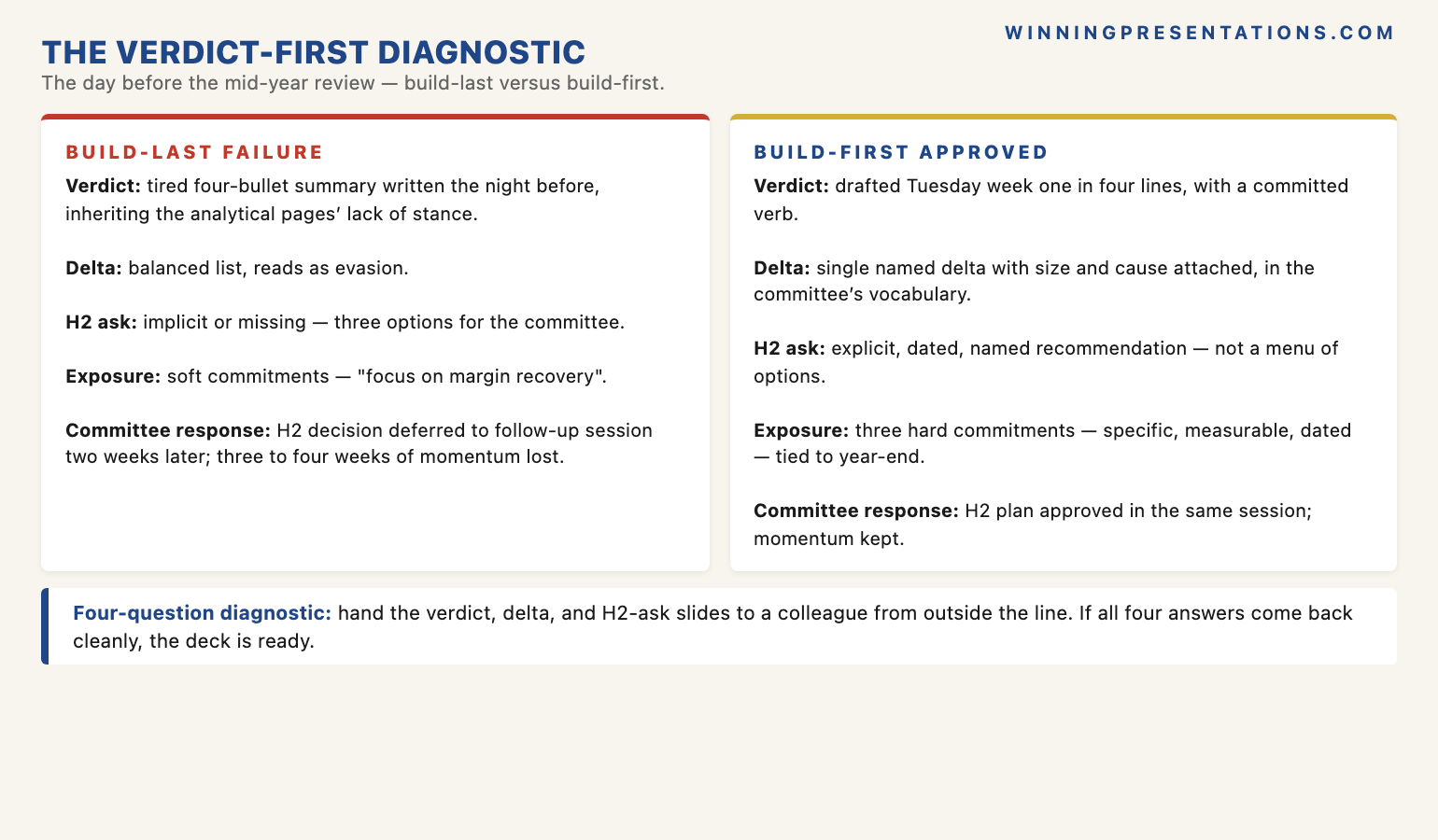

The verdict-first diagnostic is the test to run on slides three (verdict), nine or wherever the bridge sits, and the final slide before walking into the committee. The procedure is the same for every business line and sector. Print the verdict slide, the named-delta slide, and the H2-ask slide. Hand them to a colleague from outside the line — a peer line head, a senior finance partner, the chief of staff to the divisional head — with the rest of the deck withheld. Ask them four questions. What is the leader’s read of the half-year. What is the single most important delta against plan and why. What is the leader asking the committee to do about H2. What commitments has the leader made for the next six months. If the colleague answers all four questions clearly from the three slides alone, the deck is doing its work. If any answer is unclear or hedged, the corresponding slide is not yet right. Cut the line that drifted, sharpen the one that was too generic, add the cause to the delta sentence, attach the date to the H2 ask, and run the diagnostic again. Three iterations typically takes ninety minutes and is the difference between an H1 review the committee acts on and an H1 review the committee absorbs and forgets.

The diagnostic is mechanical specifically because the leader is too close to the analytical work to read the verdict as the committee will read it. The leader has spent three weeks inside the bridge analysis, the channel data, and the underwriting trends. The leader cannot any longer see the slide the way a CEO who has not seen it before will see it on the morning of the session. The colleague’s pattern-match against the four questions is the closest available proxy for the committee’s pattern-match in the room. The leader who runs the diagnostic walks into the H1 review having already passed the test the committee is about to run; the leader who skips the diagnostic walks in to find out, in real time and at much higher cost, where the structural gaps were.

One thing to do before the next mid-year review

On the Tuesday afternoon of week one of the H1-close cycle, before the bridge analysis is finished, before the channel pages are signed off, before any of the analytical work is final, write the four-line verdict slide in draft. Not the polished version. The four-line, hand-written, sticky-note version that names your read of the half-year, the single most important delta against plan, the H2 ask, and the next-six-months exposure. Put the sticky note on the wall above the desk. Run every piece of analytical work that lands over the following three weeks against the draft verdict. Update the verdict when the analysis demands an update. Read the verdict aloud at the start of every leadership-team review of the H1 deck. The verdict that survives the analytical work is the one that goes on slide three. The deck builds itself around it. The committee reads it in twenty seconds and engages with the H2 ask. The H1 review ends with a decision, not a deferral.

Frequently asked questions

Isn’t writing the H1 verdict before the analysis just guessing the conclusion?

It is hypothesis-driven leadership, which is the opposite of guessing. The leader has spent five and a half months running the business line; they already have a working read of where the half-year landed before the formal H1-close cycle begins. The draft verdict is that working read, written down, and then pressure-tested by the analytical work as it lands. If the analysis confirms the verdict, the leader walks into the committee with a verdict the analysis backs. If the analysis contradicts the verdict, the leader updates it and arrives with a verdict the analysis backs. Either way, the committee sees a verdict supported by analysis. The leader who waits for the analysis to write the verdict arrives with a tired summary of pages the committee will not read in detail. The hypothesis-first approach is how senior operating leaders run their businesses; the H1 review should be a continuation of that, not a departure from it.

What if the H1 verdict is genuinely mixed — some areas ahead of plan, some behind — how do you write a four-line verdict for that?

The mixed H1 is the typical case, not the exception. Almost every business-line H1 lands as some-ahead and some-behind. The four-line verdict still names one read, not five. The discipline is to identify the single most important leadership signal the committee needs to engage with for the half-year as a whole — the one delta that, if missed, would mean the H2 plan is wrong — and write the verdict around that. The other deltas appear in the bridge analysis. They do not compete with the verdict for the slide. A leader who insists on a balanced four-bullet verdict because the half-year was balanced is reporting averages instead of leading. Committees do not want averages. They want the leader’s read of which signal mattered most.

How long should the full H1 deck be, given that the verdict slide does most of the work?

Fifteen to twenty slides for a business-line H1 review is the working norm in senior committees. The verdict slide on slide three, the named-delta bridge on slides four to seven, the channel or function deep-dive where it serves the verdict, the H2 ask on the second-to-last slide, and the next-six-months exposure page on the last. Slides above twenty-five almost always indicate a deck built without a clear verdict, where the analytical pages are doing the work the verdict slide should be doing. Most decks above thirty pages can be cut to twenty without losing anything the committee was going to engage with anyway. The fifteen-to-twenty range is uncomfortable for leaders accustomed to longer decks; it is the range committees prefer because it forces leadership prioritisation before the meeting rather than during it.

Does this approach work for an H1 review where the news is bad and the leader is on the back foot?

It works better in that case than in any other. A bad H1 with a hedged verdict reads as a leader trying to soften the news. A bad H1 with a hard verdict — named, dated, with the leader’s exposure on the H2 commitments — reads as a leader who has absorbed the news and is asking the committee to act with them on H2. The committee’s response is dramatically different. Hedged bad-news H1s trigger leadership-credibility questions that compound across the rest of the year; hard bad-news H1s with a clear H2 ask often end with the committee approving the H2 plan and the leader walking out with more authority than they had in the room. The structural courage is uncomfortable to write the night before. The committee’s reaction is the same in every case I have watched: leaders who name bad news clearly are trusted more, not less.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly (Thursday) newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate the H1 reviews committees act on from the H1 reviews committees absorb and forget. Subscribe to The Winning Edge →

For the broader picture across slides, storytelling, confidence, and delivery, the seven-product Complete Presenter library is the bundle most senior professionals find useful as a single resource — £99 for everything, lifetime access.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises senior professionals across financial services, insurance, consulting, and technology on the structure of mid-year reviews, half-year board updates, and the H2-decision sessions that hinge on them.