Quick Answer

To end a presentation effectively, close with a single decision request, a named next step with an owner and a date, and one concrete reason why acting now matters more than deferring. The final 90 seconds determine whether your work produces a decision or another review cycle. Most executives end with “any questions?” — the single most reliable way to hand the decision back to the room.

In This Article

- Why the last two minutes determine the decision

- The “any questions?” trap and why it kills approvals

- The Decision-Action-Reason framework

- What your final slide should contain

- When the room pushes back at the close

- Adapting your close for board, budget and pitch formats

- Five closing mistakes to eliminate before your next meeting

- Frequently asked questions

Valentina spent six weeks building the case. The data was solid. The recommendation was clear. Every likely objection had been addressed in the appendix. She walked into the steering committee knowing she had done everything right — and for 28 minutes, she was correct.

Then she reached the last slide.

“So… that covers the overview. Any questions?”

Three weeks later she was told the committee needed more time to review the financial modelling. The project was deferred. It had nothing to do with the quality of her analysis. It had everything to do with the final 60 seconds. She had done the hardest part of the work — built the argument, earned the room — and then handed the decision back rather than asking for it.

This is not an unusual outcome. It is the default outcome when executives end presentations the way they were trained: summarise, thank the room, open the floor. That structure works in educational settings and team briefings. In a high-stakes decision meeting, it works against you.

Need a complete presentation structure for your next high-stakes meeting?

The Executive Slide System includes closing slide templates and scenario playbooks designed for board meetings, budget approvals, and executive decision settings.

Why the Last Two Minutes Determine the Decision

How people feel at the end of an experience shapes how they judge the whole of it — a well-documented principle in behavioural psychology. In a presentation context, this means your closing does not just wrap up what came before. It is the frame through which the entire preceding 25 minutes is interpreted and acted upon.

A weak close retroactively weakens strong content. When a presentation ends with “any questions?” after a carefully constructed argument, the implicit signal is: I have given you information; I am leaving the conclusion to you. For a senior audience who expected a recommendation, that reads as uncertainty. And uncertainty from a presenter is one of the most effective reasons to defer a decision.

A strong close, by contrast, frames everything that came before as evidence for a specific action. It tells the room: here is what I need from you, here is who is responsible, here is when it needs to happen. That is not pressure. That is the clarity that senior executives are paid to produce — and to respect when they see it in others.

The “Any Questions?” Trap and Why It Kills Approvals

“Any questions?” is not neutral. It is a structural signal that you have finished presenting and are handing control of the meeting back to the room. In most social and educational settings, this is appropriate. In an executive decision meeting, it is a strategic error.

When you ask for questions, three things reliably happen. First, the most vocal person in the room asks about the detail that interests them most — which is rarely the detail most relevant to the decision. Second, someone raises an objection that opens a discussion you had not prepared for. Third, the person with decision authority says nothing, because they are waiting to see how the rest of the room responds before committing.

By the time two rounds of questions have been answered, the energy has dispersed. The thread connecting your recommendation to a specific action has dissolved. The meeting closes with “let’s take this offline” or “we’ll review and come back to you” — and the decision clock resets entirely.

The alternative is not to eliminate questions. Questions are expected and valuable. The alternative is to sequence correctly: close before you open. Ask for the decision first. Then invite questions inside that framework, so any discussion that follows moves toward a commitment rather than away from it.

The Decision-Action-Reason Framework

The executive closing framework has three components delivered in sequence. Each takes under 30 seconds. Together they take a presentation from “informative” to “actionable.”

1. The Decision Request

State precisely what you need the room to approve. Not “I would welcome your thoughts on this.” Not “we are hoping to move forward.” A direct request: “I am asking for approval to proceed with Phase 1 at a budget of £240,000, with implementation beginning 5 May.” One sentence. One number. One date.

2. The Action Assignment

Name the next step, the owner, and the deadline. “If approved today, Henrik in Finance issues the purchase order by the 22nd, and we brief the vendor team the following Monday.” This collapses the gap between approval in the room and work starting in the building. It also signals that you have already thought through the consequences of a yes — which is the strongest form of preparation credibility.

3. The Reason to Act Now

Give one concrete reason why this decision is better made today. Not manufactured urgency — a real one. A contract window, a regulatory deadline, a competitive pressure, a resource availability issue. “The vendor holds our preferred pricing until the 30th of this month. A decision today locks that rate; a deferral to the next meeting costs an additional £18,000.” That is a reason to act now.

This sequence works because it removes ambiguity from the moment that matters most. The room knows what is being asked, who does what next, and why waiting has a cost. That is the structure of every decision that gets made cleanly.

What Your Final Slide Should Contain

Most executives end with either a “Thank You” slide or a dense recap of everything they just covered. Both are errors. The “Thank You” slide is the visual equivalent of “any questions?” — it signals completion without requesting action. The summary slide gives the room something to read rather than something to respond to.

Your final slide should contain three things: your recommendation in one complete sentence, the next action with an owner and a date, and a single contact detail for private follow-up. No bullet points. No appendix links. No “for more information, see slide 22.”

The recommendation line should be a full sentence containing the decision: “Recommended: Approve Phase 1 of the infrastructure modernisation programme at a total budget of £850,000, commencing Q3 2026.” Not a headline. A recommendation.

The action line should name a specific person: “Priya (PMO Director) to issue the project mandate by 30 April.” Naming someone in the room creates a social commitment that a generic “next steps” section never achieves.

The contact detail handles the executives who prefer to follow up privately — which is more common in board and committee settings than public questions. Include your email and direct line. Make a quiet yes easy to convert into a confirmed one.

When the Room Pushes Back at the Close

Pushback at the close is not failure. It is information. When a senior executive challenges your recommendation in the final moments rather than the middle, it means they were engaged enough to form a specific objection. That is a better outcome than polite silence followed by a deferral.

Distinguish between two types. Informational pushback means they want more data before committing: “Can you send the full cost model?” or “What contingency is built into that figure?” Respond by acknowledging the question and naming a specific follow-up: “I’ll send the full breakdown by close of business today. Does that allow us to confirm by Thursday?” You have answered the objection and preserved the decision timeline.

Positional pushback means someone has a strategic concern that data alone will not resolve: “I am not sure the timing is right given current market conditions.” This requires a different move — not more numbers, but a question: “What would need to be true for the timing to feel right?” That surfaces the actual concern, which you can then address directly rather than arguing past it.

In both cases, your goal is the same: preserve the decision timeline. The presentation closing framework exists to keep that timeline intact even when the conversation becomes complicated. You can give more information. You can address a concern. What you should not do is allow “let’s revisit this” without attaching a specific date and a specific commitment.

Adapting Your Close for Board, Budget and Pitch Formats

The Decision-Action-Reason structure works across formats, but the emphasis shifts depending on the meeting type.

Board presentations require the sharpest decision request. Board members are there to make decisions, not review process. Lead with the decision, spend the most time on the reason, and keep the action step brief. If the board approves, the operational team handles the implementation detail.

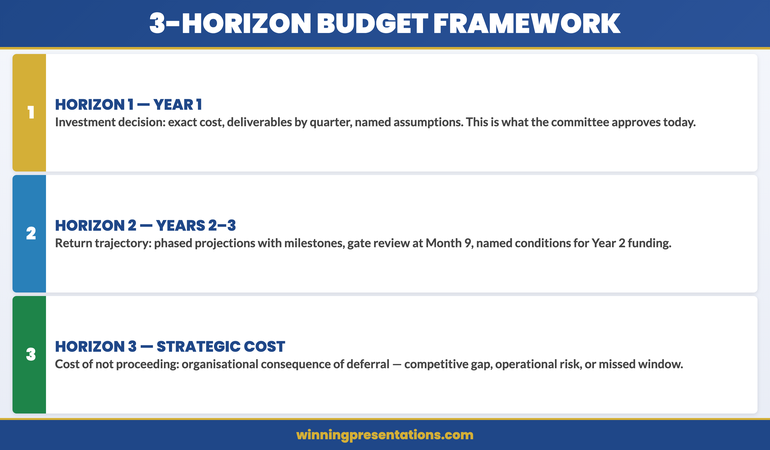

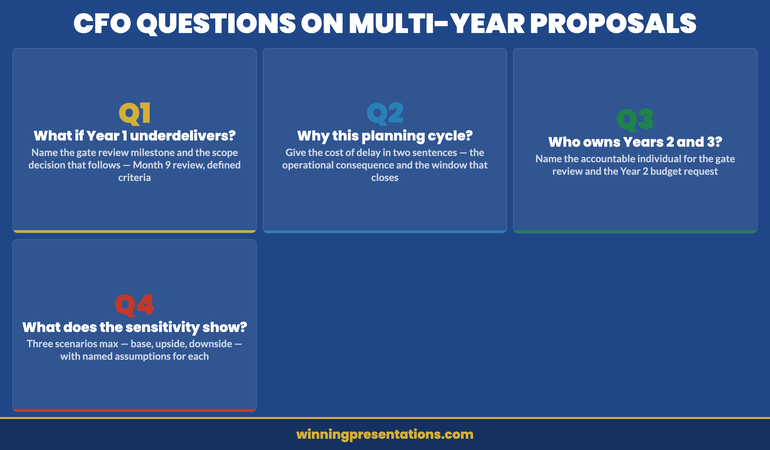

Budget presentations require the strongest reason to act now. Finance audiences are trained to identify costs and risks — their default position on any budget request is scepticism. Your closing reason must be cost-of-delay rather than cost-of-approval. “Deferring this to Q4 means we miss the procurement window and pay spot rates, adding 23% to the total cost” is more persuasive to a CFO than any benefit statement. The multi-year budget proposal framework builds this kind of close into the full structure from first slide to decision request.

Pitch presentations require the clearest action assignment. In a sales or partnership context, the close is about commercial commitment, not internal approval. The action step should be specific and low-friction: “I would like to suggest a 30-minute call with your procurement lead next week to walk through the implementation timeline. Would Tuesday or Wednesday work?” A specific ask produces a specific answer. “Let us know when you are ready” produces nothing.

In all three formats, the underlying principle holds: a presentation outline that does not build toward a specific close is a report. The difference is not in the quality of the analysis. It is in whether you ask for the decision. For opening-to-close consistency, the how to start a presentation guide covers the techniques that prime the room for a decision-ready close from the first slide.

If you are rebuilding your closing sequence before an upcoming board or budget presentation, the Executive Slide System includes closing templates for every major executive meeting format.

Build a Closing Slide That Gets the Decision

The Executive Slide System — £39, instant access — includes closing slide templates and scenario playbooks for executive decision settings. Stop ending with “any questions” and start ending with a named decision, a clear next step, and a reason to act today.

- Closing slide templates for board meetings, budget approvals and project sign-offs

- Framework guides for structuring the final 90 seconds of any high-stakes presentation

- 51 AI prompt cards to build your closing sequence in under 10 minutes

- 15 scenario playbooks covering executive meeting formats

Get the Executive Slide System →

Designed for executives who need board-ready decks without spending three days in PowerPoint.

Five Closing Mistakes to Eliminate Before Your Next Meeting

Beyond “any questions?”, four other habits consistently undermine strong presentations.

The summary recap. Starting your close with “so, to summarise what we covered today…” treats the room as if they were not listening. Senior executives were listening. They do not need a recap — they need a direction. Skip the summary and move directly to the decision request.

The passive recommendation. “We believe this is the right approach and would welcome your feedback.” This positions you as an adviser rather than a decision owner. Own the recommendation: “I recommend we proceed” is more credible than “we feel this could work.”

The overstuffed final slide. A closing slide with six bullet points, three logos, and a disclaimer signals that you have not decided what matters most. Clarity on the final slide is a proxy for clarity in your thinking. One recommendation. One action. One contact.

The time apology. “I know we are running short on time, so I will skip ahead…” undermines your authority in the final moments. If you are running long, cut from a content section in the middle — never from the close. The close is the only part the room must hear to make a decision.

The open-ended handover. “I will leave it with you to review and come back when you are ready.” This has no decision, no timeline, and no owner. The presentation becomes a document in someone’s inbox rather than a meeting with an outcome. Always leave the room with a specific next step and a named date.

Need the Full Deck Structured, Not Just the Close?

The Executive Slide System — £39, instant access — provides slide templates and AI prompt cards for every section of an executive presentation, from opening to decision request.

- 22 PowerPoint templates covering executive, board and investor scenarios

- 51 AI prompt cards to draft, refine and polish every section in minutes

Get the Executive Slide System →

Designed for executives preparing decision-stage presentations under time pressure.

Want the complete toolkit?

A closing framework that drives action is one of seven pieces senior presenters need in every executive deck. The Complete Presenter Bundle pulls all seven products together — slides, Q&A, anxiety, storytelling, delivery, openers, cheat sheets — for £99 (save £91.97 vs buying separately). Lifetime access.

Frequently Asked Questions

How long should the closing section of a presentation be?

For a 30-minute executive presentation, your close should take no more than 90 seconds to deliver. The decision request takes 20 seconds. The action assignment takes 20 seconds. The reason to act now takes 30 seconds. A brief pause and the invitation for questions takes the remainder. If your closing is running longer than 90 seconds, you are recapping rather than closing — and recapping in the final moments signals uncertainty to the room.

What if the decision-maker is not ready to commit at the end of the meeting?

Ask for a conditional commitment rather than a full approval. “If the financial model I send today confirms the figures, can we confirm this decision by Thursday?” A conditional commitment is far more useful than an open-ended deferral. It gives you a specific follow-up action, a named deadline, and a clear criterion for the decision. Most deferrals happen because no one defines what “more information” actually means. Your job at the close is to make that definition concrete.

Is it appropriate to end a presentation with a question?

Yes — but the right question. “Any questions?” is not a close; it is an abdication of the decision moment. A closing question that works presupposes forward motion: “Which of these two implementation options fits better with your Q3 planning cycle?” or “Is there anything that would prevent us from confirming this today?” These questions move the conversation toward a decision. The distinction is between a question that opens an undefined conversation and one that frames a specific choice.

What should I do if my presentation goes over time and I have to shorten the close?

Never shorten the close. If you are running long, cut from a content section in the middle — specifically the section that contains the most detail the audience already knows or can read in a supporting document. The opening, the recommendation, and the close are non-negotiable. An executive who hears your recommendation and your decision request, even without the full supporting argument, is better positioned to make a decision than one who has all the context but no direction on what to do with it.

The Winning Edge — Weekly Executive Communication Insights

Each Thursday: one high-stakes communication technique, one real case study, one action you can apply before your next meeting.

Download the free Executive Presentation Checklist — a one-page structure review you can run through the day before any high-stakes meeting.

About the Author

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she has delivered high-stakes presentations in boardrooms across three continents.

A qualified clinical hypnotherapist and NLP practitioner, Mary Beth advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds and approvals.