Quick answer: “Walk me through line 47” is the CFO drill-down question that exposes whether the presenter built the deck personally or whether someone on their team did the work. The question is rarely about line 47 itself; it is a probe to test whether the presenter understands the underlying analysis. The four-line response structure that holds up names the line in plain language, explains how the number was derived, names the assumption it rests on, and offers either the sensitivity or the alternative. Guessing is fatal — a wrong answer here permanently damages credibility for the rest of the meeting and often for several quarters after. The structural fix is to anticipate which lines the CFO is most likely to zoom into and to prepare those four-line responses before the meeting.

JUMP TO:

Mei, an FP&A vice president at a Singapore-headquartered fintech, was three minutes into a quarterly finance review when the group CFO interrupted with seven words: “Walk me through line 47, please.” Line 47 was a £284,000 figure on a sub-schedule four pages into the appendix — not a line Mei had highlighted in her presentation, not a line she had rehearsed against, and not a line she had personally built. She had inherited the model from her predecessor and had double-checked the totals but not every input. She paused, started a sentence, paused again, and then said, honestly, “I’d like to come back to that — let me confirm with the team and circle back this afternoon.” The rest of the meeting proceeded politely. The follow-up was professional. But the next quarter, the CFO requested a different presenter from her team for the review.

The diagnosis was not about line 47. It was about what line 47 had revealed: that the presenter had not personally built the deck. The CFO’s question was a calibrated probe, and the probe had returned the answer it was looking for. Honesty in the moment had been the right move — guessing would have been worse — but the structural exposure was real. The lesson Mei drew, correctly, was that the next quarter’s preparation needed to include personally walking every line of every schedule that might appear in the deck, even at the cost of three additional days of preparation time.

This piece walks through what the “walk me through line 47” question is actually testing, why it is one of the highest-leverage moves a CFO has in a finance review, the four-line response structure that holds up under it, how to predict in advance which lines a CFO is most likely to zoom into, and what to do when you genuinely do not know the answer. The principles apply across budget reviews, capex submissions, quarterly business reviews, and any other finance presentation where the audience has the right to interrupt and the analytical depth to ask drill-down questions.

Want a one-page reference of the questions a CFO uses to test a finance deck?

The 10 Questions Every CFO Asks (+ Scripts) is a free one-page cheatsheet of the questions finance leaders most often use to probe a deck — with the response structures that hold up under each. Includes the drill-down patterns covered in this article. Free download.

Why “walk me through line 47” is the question CFOs really ask

The “walk me through line 47” pattern is one of the oldest moves in finance leadership and remains one of the most reliable. It works as a calibration question — a single, narrowly targeted ask that reveals whether the presenter has the depth to handle the rest of the meeting. The question is unfair in the sense that no presenter can know every line of every schedule equally well, but it is also fair in the sense that a presenter who has built the deck themselves can usually answer it, and a presenter who has not, usually cannot. The asymmetry is the point.

The question typically arrives early in the meeting, often in the first five minutes. The timing is deliberate. A CFO who establishes the depth question early gets useful information that calibrates their reading of the rest of the deck — if the presenter handles it well, the CFO can read the rest of the meeting at the strategic level; if the presenter handles it badly, the CFO knows to apply more analytical scrutiny on the rest of the slides and to weight the presenter’s interpretive judgements more carefully. The early-meeting placement is a feature, not an aggression.

The other reason the question is reliable is that it is hard to coach around. A presenter can rehearse the strategic message, can prepare for the obvious questions, and can practise the smooth flow of the deck. None of that protects against a randomised drill-down into a sub-schedule line. The only defence is depth — having built or personally walked the analysis underneath the slides. The question’s asymmetry between rehearsable surface and unrehearsable depth is what makes it valuable to the CFO. For more on the broader category of high-stakes finance Q&A this question lives in, see our budget presentation questions CFO piece.

What the question is actually testing

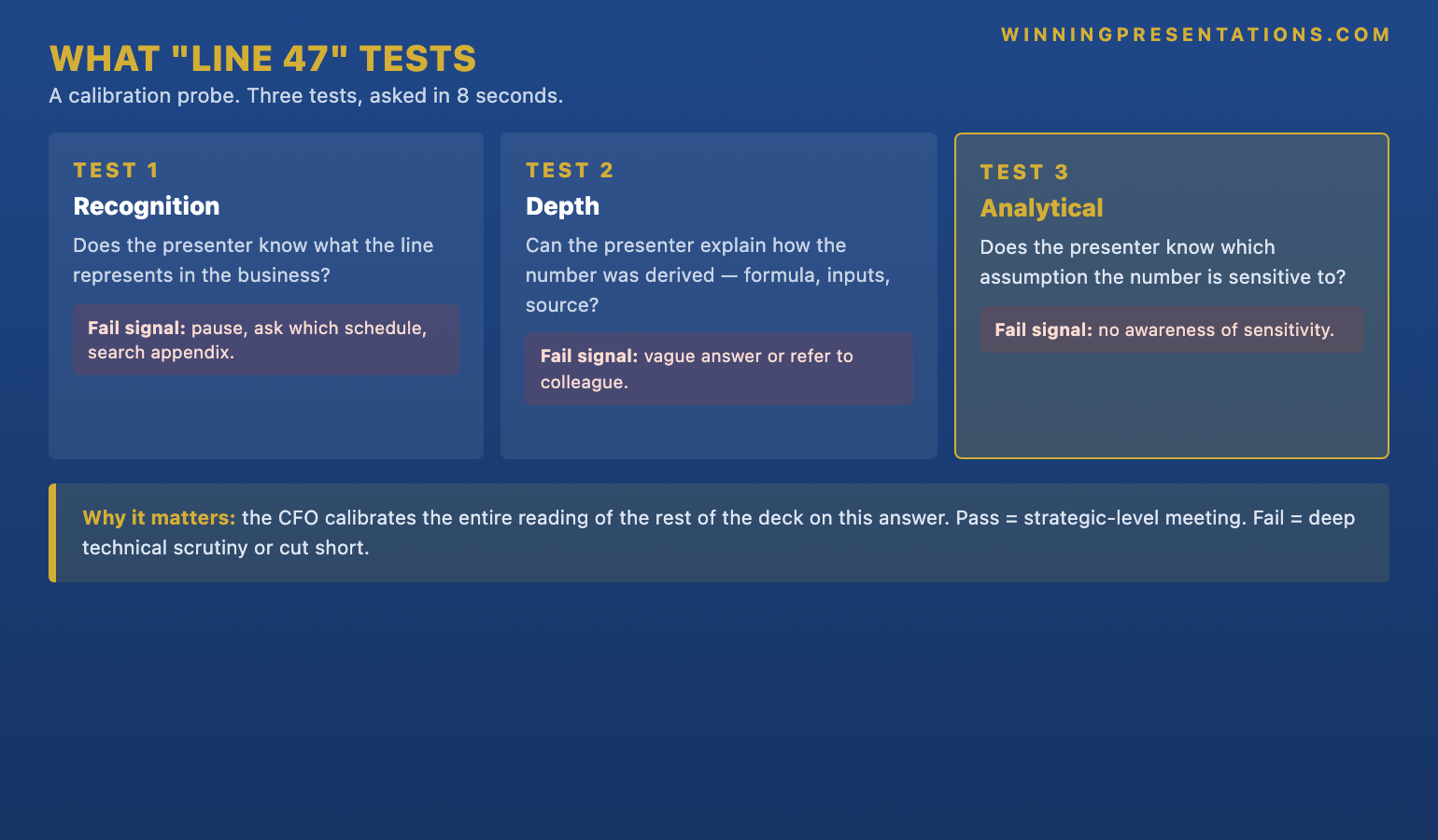

The question tests three things, in this order. First, does the presenter recognise the line and what it represents? A presenter who pauses, asks “which schedule?”, and then visibly searches the appendix has failed the recognition test before the answer begins. Second, can the presenter explain how the number was derived — the formula, the inputs, the source data? This is the depth test. Third, does the presenter know what assumption the number is sensitive to and what would change it materially? This is the analytical test. A complete answer covers all three. A partial answer covers the first two but not the third. A failed answer covers only the first or none of them.

The CFO is not, in most cases, trying to embarrass the presenter. They are trying to calibrate their own reading of the rest of the deck. A complete answer means the deck can be trusted at face value and the meeting can move at the strategic level. A partial answer means the deck is broadly sound but the CFO will probably probe one or two more line items before settling. A failed answer means the deck cannot be trusted at face value and the meeting either pivots to a deep technical review or, more often, gets cut short with a request to come back when the presenter can stand behind the work.

The asymmetry of consequence is significant. A presenter who passes the test gets a constructive, strategic-level review meeting. A presenter who fails it has not just lost the moment — they have changed the entire texture of the next 15 minutes and often the next several quarters. CFOs who form a view that a presenter is not standing behind their own deck do not usually update that view quickly. The line 47 moment is therefore one of the highest-leverage moments in the entire review, even though it lasts no more than 60 seconds and is not on the agenda. It pays to prepare for it disproportionately.

The four-line response structure that holds up

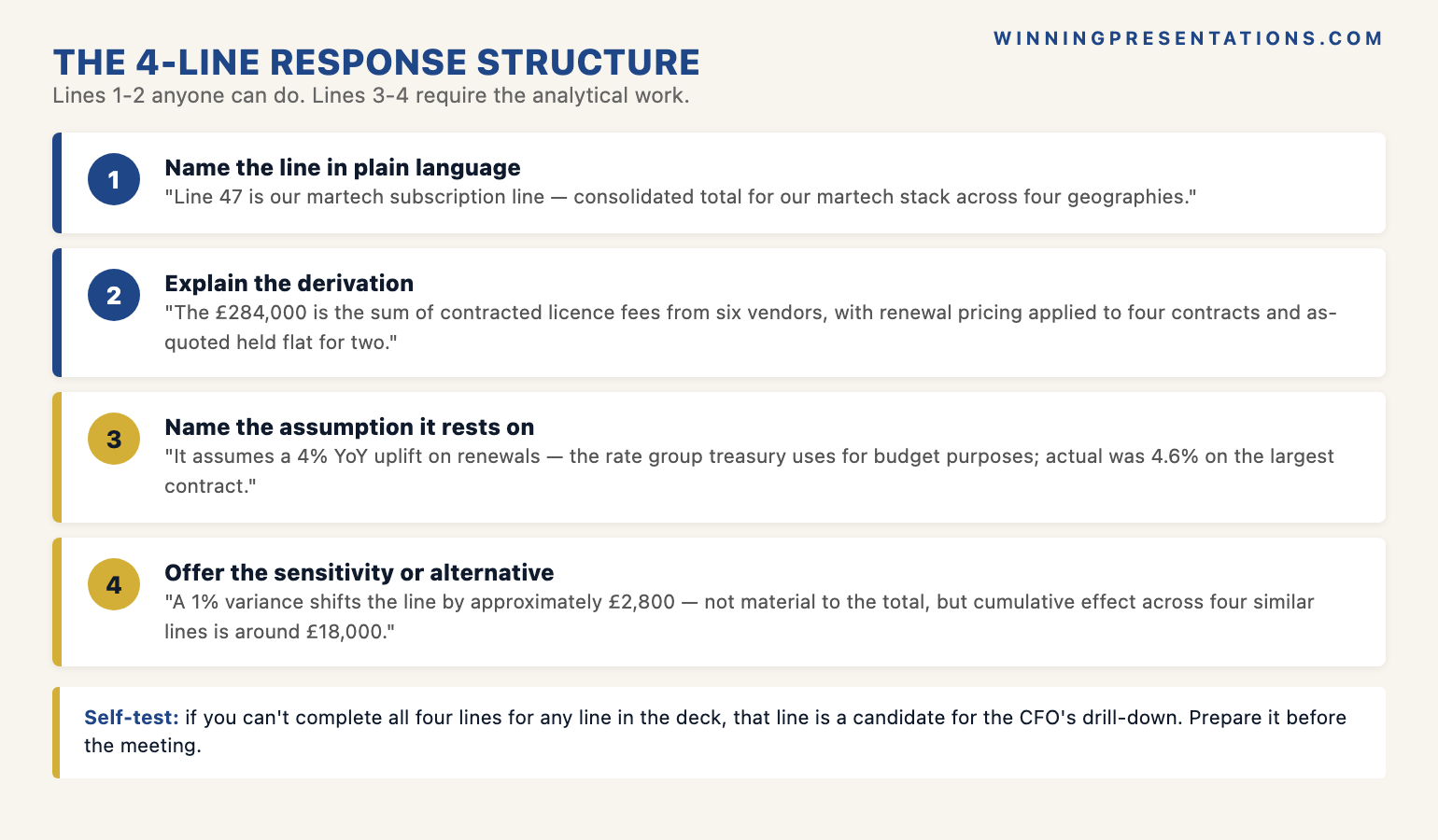

The four-line response structure has each line do specific work. Line one names the line in plain language: “Line 47 is our marketing technology subscription line — the consolidated total for the licensing of our martech stack across the four geographies we operate in.” Line two explains the derivation: “The £284,000 figure is the sum of contracted licence fees from six vendors, with renewal pricing applied to the four contracts that renewed during the period and the as-quoted rate held flat for the two that did not.” Line three names the assumption: “The number assumes a 4 per cent year-on-year increase on the renewals — that is the rate group treasury is using for budget purposes; the actual outcome was 4.6 per cent on the largest contract.” Line four offers the sensitivity or alternative: “A 1 per cent variance from the assumption shifts the line by approximately £2,800; the figure is not material to the total but the cumulative effect across the four similar lines is around £18,000.”

The structure works because it answers the question at three levels simultaneously — the line itself, the analytical work behind it, and the sensitivity that determines how much it matters. A CFO who hears this answer knows the presenter has personally engaged with the line and trusts the rest of the deck more as a result. The CFO may follow up with one more probing question, but the follow-up will be specific rather than searching, because the four-line answer has demonstrated the presenter can handle that specificity.

The discipline is in line three and line four. Line one and line two are answerable by anyone who can read the schedule; lines three and four require the presenter to have done the analytical work. A presenter who can name the line and the derivation but cannot name the assumption it rests on has answered at the data-entry level rather than the analyst level. CFOs notice the difference. The four-line structure is therefore both an answer template and a self-test: if you cannot complete all four lines for any line in the deck, that line is a candidate for the CFO’s drill-down probe and needs more preparation. For the wider discipline behind handling drill-down questions in high-stakes Q&A, see our Executive Q&A Handling System overview.

Build the response structures for the questions that will actually decide the meeting.

The Executive Q&A Handling System is a structured framework for the high-stakes Q&A that follows a finance deck — the drill-down probes, the assumption challenges, the sensitivity questions, and the calibration moves CFOs use most often. Includes the four-line response template covered in this article and the wider library of response structures.

- The 8-second pause-and-structure protocol that keeps you calm under drill-down pressure

- Response templates for the most common high-stakes Q&A scenarios

- Tough questions handled with calm authority and decision-safe answers

- The structural moves that separate technical depth from defensive rambling

- £39, instant download, lifetime updates

Which lines CFOs pick — and how to predict them

CFOs do not pick line items at random. The line they zoom into typically has at least one of four characteristics. First, the line is materially larger than its peers — a £284,000 line in a column of £40,000 lines stands out, and the CFO will probe whether the larger figure has a structural explanation or whether it is an aggregation that hides a different story. Second, the line has changed materially from the prior period — a doubling, halving, or sign reversal will draw a probe. Third, the line uses an unusual classification — a category that does not appear elsewhere in the schedule, or a category that appears only for this line. Fourth, the line sits adjacent to a line the CFO has independent reason to suspect — a category they have seen problems in elsewhere in the firm.

The implication for preparation is that you can largely predict which lines the CFO will probe. Run through every schedule before the meeting and flag any line that meets one or more of the four criteria above. Those are the candidates. For each candidate, prepare the four-line response structure. The preparation typically takes around two minutes per candidate; a 30-page appendix with eight candidate lines therefore takes around 16 minutes of focused work. That is the highest-return preparation time in the entire review cycle, because it directly counters the highest-leverage move the CFO will make.

The other useful technique is to ask the team that built each schedule to identify the one or two lines they would most expect a CFO to probe. The team has spent more time in the model than the presenter and usually has good intuition about which lines are most exposed. Their candidates almost always overlap with the candidates the four-criteria scan produces, and the overlap helps prioritise the preparation. The lines that appear on both lists are the ones to walk through most carefully; the lines that appear only on one are still worth preparing but at a lower level of detail.

When you genuinely don’t know the answer

Even with thorough preparation, there are moments when the CFO drills into a line you cannot answer. The question is what to do in that moment. The wrong move is to guess. Guessing produces a number or an explanation that may turn out to be wrong, which compounds the credibility damage rather than limiting it; a presenter who guesses badly has now misled the room rather than admitted ignorance. The right move is to acknowledge cleanly, name what you can offer in the moment, and commit to a specific follow-up.

The structure that works has three parts. Acknowledgement: “I want to be honest — I haven’t personally walked that line ahead of this meeting and I don’t want to guess on the derivation.” What you can offer in the moment: “I can tell you that the line falls in our martech category and that the prior-period comparison was approximately £210,000, so the variance is meaningful but not unprecedented.” Commitment: “I’ll have the full derivation, the assumption, and the sensitivity to you by close of business today; I’d rather give you the answer right than the answer fast.”

This response is not a save in the sense of recovering full credibility — that recovery happens through the follow-up, not in the moment — but it is significantly better than guessing. Most CFOs respond constructively to honest acknowledgement; almost none respond constructively to a wrong answer delivered confidently. The asymmetry is consistent. A presenter who knows their limits and is willing to say so is preferred to a presenter who fakes depth and is later found out, even though the latter has a slightly better moment in the room. The credibility ledger is over the meeting and the follow-up combined, not over the 30 seconds of the answer itself. For more on how to structure the broader response work that surrounds questions like this, see our how to present to a CFO piece.

If the deck-level structural work is also exposed in this meeting:

The Executive Slide System is a structured library of templates and frameworks for board-ready slide work — including the variance and assumption-set slide structures that pre-empt many of the drill-down probes covered above. Pairs with the Q&A response work for finance presentations.

Frequently asked questions

Should I bring the model laptop into the meeting so I can look up line 47 on the spot?

Generally no. Opening the model in the meeting reads as not having prepared, and the time spent finding the cell, scrolling to the formula, and tracing the inputs slows the meeting in a way most CFOs find unhelpful. The exception is for review meetings explicitly framed as model walkthroughs, where the model is the meeting. For standard finance reviews, the discipline is to know the deck and the schedules well enough that the model is not needed in the room; the model lives in the follow-up email, not in the meeting itself.

Is it acceptable to refer the question to a member of my team in the room?

Sometimes. If the team member who built the line is in the room and the meeting culture supports it, a brief handoff can work — “Priya built this section and can speak to it more accurately than I can — Priya?” But the move has to be calibrated. A senior leader who repeatedly hands off drill-down questions signals they are not personally across their own deck, which is the same credibility flag as not knowing the answer in the first place. One handoff in a meeting is fine; three handoffs is a problem. The rule of thumb is to handle the question yourself unless there is a substantive reason the team member can answer materially better — for example, they have just completed a re-baseline you have not yet been briefed on.

What if the CFO drills into a line that’s clearly immaterial?

Answer it the same way you would a material line. The drill-down is not really about the line’s materiality — it is about your depth. Treating a line as “too small to be worth answering” reads as deflection and amplifies the credibility damage. The four-line response works equally well on a £284,000 line and on a £28,000 line; the structure does not depend on the size of the number. The presenter who answers a small-line drill-down with the same rigour as a large-line drill-down often passes the CFO’s calibration test more cleanly than a presenter who answers only the big questions well.

How do I recover credibility if I gave a wrong or partial answer?

Through the follow-up, not through more talking in the meeting. Trying to recover in the moment usually compounds the damage — additional explanation reads as defensive, and the presenter ends up further from the original answer. The cleaner move is to acknowledge briefly (“Let me confirm that and come back to you precisely”), let the meeting proceed, and then send a tight, accurate follow-up note within hours that gives the full four-line response structure for the line in question. Most CFOs will accept the in-meeting limitation if the follow-up arrives quickly and is precisely accurate. The recovery happens between meetings, not within them.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate decks committees back from decks they defer. Subscribe to The Winning Edge →

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.