Quick Answer: Investor hostile questions are almost always invitations, not attacks. The technique that wins the room is steel manning — restating the investor’s objection in its strongest form, acknowledging the legitimate concern underneath it, and only then answering. Founders who defend lose credibility. Founders who dismiss lose the term sheet. Founders who steel-man show they have already thought harder about the risk than the investor has.

JUMP TO:

- Why investor hostile questions are usually invitations, not attacks

- The defence reflex: why every founder’s first instinct loses the room

- Steel manning explained — the technique lawyers and politicians use

- The four-step steel-man response framework

- Worked example: “your unit economics don’t work”

- When not to steel-man: the two questions where it backfires

- Practising steel manning so it becomes reflex

- FAQ

Mei was eleven minutes into her Series B pitch when the lead partner leaned forward and said, flatly: “Your unit economics don’t work. You’re burning cash to acquire users you’ll never make profitable. Convince me otherwise.” The other two partners stopped typing. One closed her laptop.

Mei’s first instinct was to defend — to walk the partner through the LTV calculation on slide seventeen. Her second, a second later, was to dismiss: “Actually, our contribution margin is positive at month nine.” Both were wrong, and she could feel it as she opened her mouth.

What she said instead: “The concern you’re raising is the one that should scare us most. If I can’t show you a path from today’s blended CAC of £84 to cohort-level payback under fourteen months, this isn’t a Series B business, it’s a bridge round. Let me show you what we think the answer is, then I want to hear where you still don’t believe it.” The partner who closed her laptop reached for it again. Mei had the room for the next thirty-two minutes.

When the hardest question is the one that decides the round

The Executive Q&A Handling System is a framework for handling hostile, unexpected and high-stakes questions in investor, board and executive settings — bridge statements, deflection techniques, composure protocols and the structural habits senior operators use when the room turns adversarial.

Why investor hostile questions are usually invitations, not attacks

A hostile question in an investor meeting is rarely personal. Partners sit through twenty or thirty pitches a week. The ones that hold attention are where the founder can be pushed hard on the central risk and respond without losing composure. The partner is trying to find out whether you survive the boardroom conversations they will have about you for the next seven years.

This reframe matters because the emotional shape of the question and its strategic intent are almost opposites. The question sounds like “you’re wrong.” The intent is almost always “show me you have thought about this harder than I have.” Founders who hear the first version defend. Founders who hear the second demonstrate judgement.

One kind is genuinely adversarial: the question designed to move the pricing conversation. “I’m not sure this is a £60m post-money business at current metrics” is not an invitation to rebut the metrics — it is an opening move in a valuation negotiation. Confusing the two is how founders lose ground they cannot recover.

The defence reflex: why every founder’s first instinct loses the room

Watch enough investor pitches and you notice that almost every founder, when pushed, does one of two things in the first sentence. They defend the specific number, or they dismiss the premise and pivot to a metric they prefer. Both lose credibility with experienced investors.

The defence reflex — “actually, the CAC is lower if you strip out the paid acquisition test” — signals that the founder has not yet accepted the central risk. Every “if you look at it this way” sounds like optimising the number rather than solving the problem. The partner stops listening to the specifics and starts listening to the posture.

The dismissal reflex is worse. “That’s not how we think about unit economics at our stage” tells the investor that the founder cannot hold two models at once — their own, and the one investors use to evaluate businesses like theirs.

Experienced founders do something slower and more effective. They pause. They restate the question in terms even stronger than the investor used. Then they answer. This is steel manning.

THE EXECUTIVE Q&A HANDLING SYSTEM — £39

The framework for handling the questions that decide the meeting

The Executive Q&A Handling System is a structural framework for hostile, unexpected and high-stakes Q&A in investor, board and executive settings. Bridge statements, deflection techniques, composure protocols and the steel-manning response pattern referenced throughout this article. £39, instant access.

For founders, executives and senior leaders who face live Q&A in high-stakes rooms.

Steel manning explained — the technique lawyers and politicians use

Steel manning is the rhetorical practice of stating an opponent’s argument in its strongest form before you respond. It is the opposite of straw manning, which weakens a position so it is easier to knock down. Trial lawyers do this in cross-examination. Senior politicians do it under press scrutiny. Supreme court advocates will often summarise opposing counsel’s case better than opposing counsel did before dismantling it.

It works because it demonstrates two things the audience wants to see: that you understand the argument against you, and that you are confident enough to give it its best hearing first. An investor asking a hostile question listens for those signals before anything else.

There is a second effect. When you restate the objection in its strongest form, you take control of the frame. The investor’s version is now your version. You choose which part to address first. The person who defines the problem shapes the conversation about the solution. For founders who have handled board pushback, the logic that works on hostile board presentation questions carries directly across.

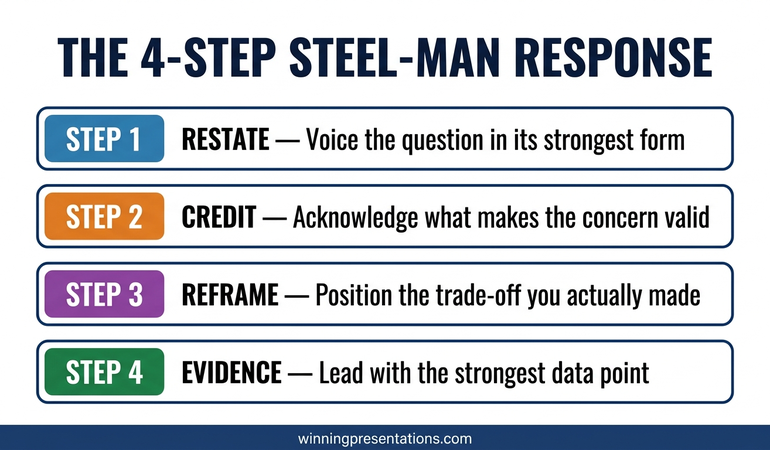

The four-step steel-man response framework

A steel-manned response has four moves. The whole sequence usually takes forty to sixty seconds before you reach the substantive answer — the most valuable sixty seconds in most pitch meetings.

Step 1 — Restate the concern in its strongest form. Not in the investor’s exact words, but in the version that would worry you most if you were in their seat. “If I were sitting on your side of the table, the version of this I’d want answered is…” You are signalling that you have thought about this from the investor’s position.

Step 2 — Name the legitimate risk underneath. Every hostile question contains a real risk. Identify it and say it out loud before the investor has to. “The legitimate risk is that we hit the growth ceiling on our current channel before cohort-level payback confirms the LTV assumption.” This moves the conversation from whether the risk exists to what the response to it is.

Step 3 — Show your actual thinking. Not a slide number. The specific mental model you use to hold the risk. “We think about it in three horizons: current channel saturation, second-channel activation, and pricing power on retained cohorts.”

Step 4 — Offer the investor a role in the remaining uncertainty. Invite them to say where they are still not convinced. “Tell me which of those three looks shakiest to you and let’s go there first.” You have given the partner permission to keep pushing without making it feel hostile.

The general Q&A handling framework covers the composure protocols underneath this — the pause before restatement, the eye-contact rule during step four.

Worked example: handling “your unit economics don’t work”

Take the partner’s opening challenge from Mei’s pitch and run it through the framework.

The question: “Your unit economics don’t work. You’re burning cash to acquire users you’ll never make profitable. Convince me otherwise.”

Step 1 — Restate stronger. “The concern you’re raising should scare us most. The version I find most useful internally: we have not yet proven that the cohorts we’re buying today will look like the 2024 cohorts on month-thirty payback. If they don’t, we’re not a Series B business at this valuation.”

Step 2 — Name the legitimate risk. “The real risk is CAC inflation on channels that haven’t saturated. We’ve seen a 19% CAC increase on paid search in six months. If that continues linearly, month-thirty payback moves from fourteen months to nineteen, and the LTV:CAC ratio drops below the threshold this round is priced on.”

Step 3 — Show actual thinking. “We’re holding that as three layered bets. First, paid search CAC is cyclical rather than structural, and we have cohort evidence. Second, the partnerships channel we launched in Q1 is running at 38% of blended CAC. Third, pricing power on retained 24-month cohorts gives us a lever we haven’t pulled.”

Step 4 — Invite continued pressure. “Of those three, the partnerships channel is the one I’d want to stress-test first. Do you want to go there, or see the 24-month cohort curves?”

This response does not defend the CAC number or dismiss the premise. It treats the question as the most important thing that will be said in the meeting and answers it with the seriousness that implies.

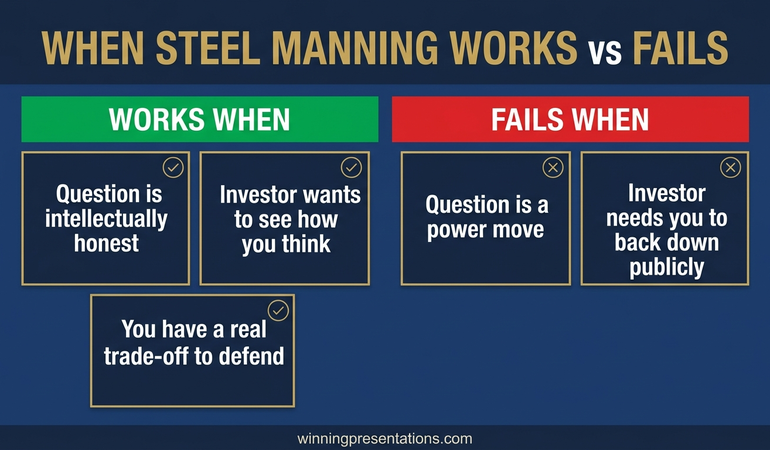

When not to steel-man: the two questions where it backfires

Steel manning is not a universal tool. Two categories of question make your position worse.

The factually wrong question. If the investor has misread the slide or is working from an outdated deck, do not steel-man the mistaken premise. Correct it briefly and move on. “Just to clarify — that number on slide nine is gross revenue, not ARR. ARR is on slide eleven at £6.1m.” Steel manning a factual error reinforces the error.

The pricing-negotiation question dressed as a diligence question. “I’m not sure this is a £60m post-money business” is not asking for analytical thinking on valuation. It is testing whether you will negotiate against yourself. The right response is calm and short: “We priced this round based on comparables at this stage. Happy to walk through the comparables set. But I’m not going to re-open the valuation conversation in the meeting — we have a term sheet process for that.” Steel manning a negotiating move concedes ground you cannot get back.

The rule: steel-man questions about the business. Don’t steel-man questions about the deal. Showing your thinking builds trust on the first. It leaks leverage on the second. For the wider taxonomy, the guide on how to handle tough questions in a presentation covers this in more detail.

Practising steel manning so it becomes reflex, not effort

Steel manning fails for most founders not because they do not understand the framework, but because it collapses under pressure if it has not been rehearsed. With a partner leaning forward and three seconds to respond, the first sentence has to arrive without effort.

Three practice habits build the reflex:

The hostile-question inventory. Before any investor meeting, write down the ten hardest questions you could be asked — not the ten most likely, the ten hardest. The ones that make you wince. For each, write the steel-man restatement in full sentences, not bullet points. Sentence structure is what your brain retrieves under pressure.

The cold-read drill. Hand the list to someone who does not know your business well. Ask them to read the questions aloud in a hostile tone, randomly. Pre-scripted rehearsal teaches you to answer the questions you expect. Cold-read drills teach you to handle the tone shift when the question is not the one you prepared for.

Recording and reviewing. Record yourself answering the ten hardest questions. Listen for the first three words of your response. If they are defensive (“actually,” “that’s not quite right”), you have defaulted to the defence reflex. Re-record until the first three words are the restatement. The opening phrase is the muscle memory. Everything else follows.

FOR THE NEXT INVESTOR MEETING ON YOUR CALENDAR

A structural playbook for the questions that decide the round

The Executive Q&A Handling System gives you the bridge statements, composure protocols and response frameworks that hold up in hostile investor, board and executive Q&A. Built for the moment the room turns adversarial and you have three seconds to decide how to respond. £39, instant access, no subscription.

Frequently Asked Questions

Isn’t steel manning just agreeing with the criticism?

No. Steel manning restates the concern in its strongest form and names the real risk underneath — then answers it. Agreeing concedes the point. Steel manning does the opposite: it shows you have considered the strongest version and thought through your response. Concession signals weakness. Steel manning signals that you have internalised the problem and still believe in the business.

What if the investor is wrong on the facts?

Do not steel-man a factual error. Correct it briefly and move on. “That number on slide nine is last-twelve-months gross revenue — ARR is on slide eleven at £6.1m.” Steel manning applies to questions raising a legitimate concern, even when the framing is aggressive. When the premise itself is wrong, clarify quickly so the real conversation can start.

How do I do this under time pressure?

Compress to two sentences. Sentence one is restatement-plus-risk: “The concern underneath is whether our cohort payback holds under CAC inflation — the thing we argue about most internally.” Sentence two is headline plus invitation: “Our honest answer is layered across three bets — happy to go deeper, or give you the short version first.”

Does this work for board Q&A as well?

Yes, often better. Boards are longer-term audiences — they see you every quarter and read defensive responses more harshly than a one-off pitch audience would. Steel manning at board level builds durable credibility with non-executive directors and shows the chair you can hold criticism without fragility.

The Winning Edge — weekly

One short note every Thursday on what actually moves boards, investors and senior stakeholders. No filler.

Partner post: If the meeting ends with a no rather than a yes, the next move matters more than the pitch itself. The guide on pitch rejection recovery for founders covers what to do in the seventy-two hours after a decline.

Related reading: Deck order shapes which hostile questions come up first — see investor pitch deck slide order and Series A pitch deck length.

Your next step: Before your next investor meeting, write down the ten hardest questions you could be asked and draft the steel-man restatement for each in a full sentence. Do it tonight, not the morning of. The reflex is built the day before, not the hour before.

About the Author

Mary Beth Hazeldine, Owner & Managing Director of Winning Presentations, advises executives across financial services, healthcare, technology and government on structuring presentations for high-stakes funding rounds, board approvals and stakeholder buy-in. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland and Commerzbank, she works at the intersection of finance, language and decision psychology.