- Why Audit Committee Presentations Are Not the Same as Board Presentations

- The Four-Section Structure Your Audit Committee Expects

- How to Handle Auditor and Committee Member Questions Simultaneously

- Presenting Sensitive Findings Without Signalling Weakness

- Pre-Briefing the Chair: The Step Most Finance Leaders Skip

- Frequently Asked Questions

Priya had presented to the main board six times. She understood the rhythm of those meetings — the expectation of confidence, the preference for brevity, the implicit protocol around how findings were framed. When the CFO asked her to lead the audit committee presentation for the first time, she assumed it would be similar. It was not.

Halfway through her second slide, the external audit partner interrupted. He wanted to understand the basis for a judgement call she had described as “management assessment.” Priya had expected questions at the end, not in the middle of the narrative. The audit committee chair then asked whether any of the three findings she had characterised as low-risk had been escalated for a second opinion. She had not expected that question either. The meeting did not go badly — but it went differently from every board presentation she had done before.

Afterwards, a more experienced colleague explained the dynamic. Audit committee presentations operate under a different set of expectations. The external auditor is not a passive observer — they are a participant with their own professional obligations. The committee chair is not simply a board member — they are accountable for governance in a way that makes them systematically more sceptical of management framing. And the standard of evidence required for a finding to be accepted without challenge is higher, not lower, than in a commercial presentation. Priya restructured her entire approach for the following quarter.

If you present regularly to audit committees, risk committees, or governance bodies and want a clearer structure for each section, the Executive Slide System includes slide templates and framework guides for finance and compliance presentations.

Why Audit Committee Presentations Are Not the Same as Board Presentations

Finance leaders who present confidently to their main board often find audit committee meetings unexpectedly difficult. The audience composition is similar — senior people in a formal governance setting — but the dynamics and expectations are structurally different in ways that catch prepared presenters off guard.

The first distinction is the presence of external auditors. In a board presentation, the presenter controls the information flow. In an audit committee meeting, external auditors bring their own independent assessment of the same material. This means the committee has access to a second view on the findings before or during the meeting. Management presentations that omit, minimise, or frame findings too favourably will often be corrected by the auditors in the same session — a dynamic that is visible to the committee and damaging to the presenter’s credibility.

The second distinction is the committee’s governance accountability. Board members attend meetings to make commercial and strategic decisions. Audit committee members attend specifically to provide oversight of financial reporting, internal controls, and risk management. Their professional orientation is fundamentally sceptical — they are there to ensure that material risks and control weaknesses are being surfaced, not managed away from view. A presentation that emphasises positive findings at the expense of a frank assessment of what is not working will strike an audit committee as evasive rather than balanced.

The third distinction is the standard of precision required. Board presentations often use directional language that is understood to be indicative rather than exact. Audit committees require definitional accuracy — a finding described as “low risk” will be interrogated on the basis of how “low risk” was defined and who made that assessment. Management judgements presented as facts will be challenged on their evidential basis. This is not hostility — it is the committee performing its governance function. The presenter who understands this dynamic in advance is far better positioned than one who experiences it as an unexpected challenge.

Understanding the difference between how a board receives information and how an audit committee interprets it is foundational. For background on the broader governance dynamic between management and board members, the article on presenting to non-executive directors covers the sceptical oversight posture these audiences bring to every management presentation.

Executive Slide System — £39, instant access

Structure Governance and Finance Presentations That Withstand Audit Committee Scrutiny

The Executive Slide System contains slide templates and framework guides specifically built for high-accountability governance contexts — including audit committee, risk committee, and compliance briefing formats where the standard of evidence and precision is higher than in commercial presentations.

- Slide templates for governance and compliance briefings

- AI prompt cards for framing findings and management responses

- Framework guides for structuring four-section audit presentations

- Scenario playbooks for sensitive findings and control environment assessments

Get the Executive Slide System →

Designed for finance leaders, CFOs, and internal audit heads presenting to governance committees and external auditors.

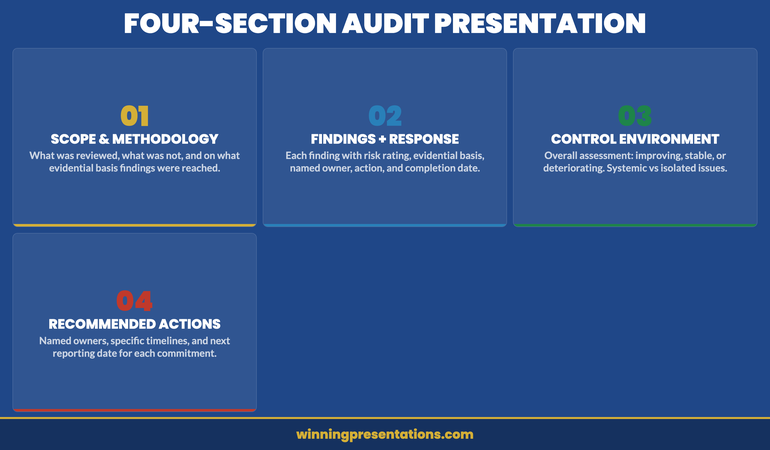

The Four-Section Structure Your Audit Committee Expects

Audit committees generally bring a procedural expectation to management presentations. They have seen enough poorly structured briefings to have formed a view about what constitutes a credible presentation of findings. A four-section structure is consistent with best practice in governance communication and provides the committee with the logical flow they expect.

Section one is scope and methodology. This section tells the committee what the review covered, what it did not cover, and on what basis the findings were reached. Committees are particularly attentive to scope because the scope of a review determines whether a finding of “no issues identified” is meaningful or simply a function of a narrow remit. If your methodology relied on sampling rather than full population testing, say so. If the scope was determined jointly with the external auditor, say so. Committees treat unexplained methodological choices as potential gaps.

Section two presents key findings with management response. Each finding should be stated with its risk rating, the evidential basis for that rating, and the management response already attached. The management response should be specific — a named owner, a completion date, and a description of the remediation action. Findings presented without responses invite the committee to ask what management is doing about them, which shifts the dynamic from a managed briefing to a reactive Q&A.

Section three assesses the overall control environment. This section steps back from individual findings to give the committee a view of whether the control framework as a whole is fit for purpose. Is the control environment improving, stable, or deteriorating? Are there systemic factors behind the findings, or are they isolated incidents? This section is where experienced presenters demonstrate that they are thinking about governance at a structural level, not just reporting individual deficiencies.

Section four proposes recommended actions with named owners and timelines. The committee should leave the meeting knowing what will happen, who is responsible for it, and when it will be reported back. Recommendations without owners and timelines are observations, not governance commitments. Audit committee members have an accountability function that extends beyond the meeting — they need to be able to verify that what was agreed has been delivered.

How to Handle Auditor and Committee Member Questions Simultaneously

One of the most distinctive challenges of an audit committee presentation is that questions can come from two distinct sources with different roles and different interests: the committee members who are providing oversight, and the external auditors who are providing independent assurance. Managing both simultaneously requires a different discipline from managing questions in a standard executive meeting.

Committee member questions tend to focus on governance adequacy — whether the control environment is sufficient, whether risks have been appropriately assessed, and whether management responses are proportionate. These questions often have a slightly adversarial quality not because the committee member is hostile, but because their governance role requires them to probe for gaps. Respond to these questions with the same four-part structure used for adverse data in any governance context: acknowledge the question, state the current position clearly, note any uncertainty, and confirm the action or timeline.

Auditor questions operate differently. The external audit partner is not challenging management from an oversight position — they are providing professional context based on their own independent review. When the auditor and management have reached different assessments of the same finding, that difference will emerge in the meeting. The most effective approach is to acknowledge the difference directly rather than contest it: “The external auditors have rated this as medium risk; management’s current assessment is low risk on the basis of [specific evidence]. We are in discussion to align our views before the next cycle.”

The most important discipline when managing dual-source questioning is maintaining the committee’s confidence in management’s objectivity. If the committee perceives that management is systematically minimising findings that the auditor has rated more seriously, the meeting dynamic shifts in a way that is difficult to recover from. Transparency about differences in assessment — presented as a professional dialogue rather than a dispute — preserves that confidence far more effectively than a unified narrative that the auditor then contradicts.

For related reading on managing live questions from senior governance audiences, the companion article on the difference between a board paper and a board presentation covers how written documentation and live briefings serve different governance functions and require different levels of precision.

Presenting Sensitive Findings Without Signalling Weakness

Every audit committee presentation includes at least one finding that management would prefer to frame more favourably than the raw assessment warrants. The challenge is to present that finding with the directness the committee requires without communicating that management is uncertain, defensive, or unable to manage the underlying issue.

The critical structural discipline is to lead with the finding’s factual description before providing any interpretive framing. Committees are experienced at recognising when a presentation is sequenced to soften a finding — when context and mitigating factors appear before the finding itself. This sequencing invites scepticism even when the mitigating factors are genuinely relevant. A finding stated directly and then contextualised is received as honest. A finding preceded by extensive context is received as hedged.

For high-sensitivity findings — particularly those that touch on compliance failures, regulatory risk, or senior personnel — the presentation format should include three specific elements: the finding stated in neutral, precise language; the management assessment of its significance with the rationale explained; and the immediate response already taken or the specific action committed to. The sequence matters. The committee’s primary concern is not the finding itself but whether management understands its significance and is responding to it appropriately. A presentation that demonstrates both qualities will generally satisfy the committee even when the finding is serious.

There is also a strategic discipline around what to proactively disclose versus what to wait for questions on. In audit committee presentations, proactive disclosure of sensitive findings is nearly always the stronger approach. Committees that learn of a sensitive issue through their own questioning — rather than through management’s upfront disclosure — draw a straightforward conclusion: management did not consider it important enough to lead with. That conclusion is often more damaging than the finding itself.

If you regularly use slide-based presentations for governance briefings and want a cleaner framework for structuring sensitive disclosures, the Executive Slide System contains slide templates designed specifically for high-accountability governance contexts including audit, risk, and compliance committees.

Pre-Briefing the Chair: The Step Most Finance Leaders Skip

The audit committee chair holds a specific governance role that differs from the role of a standard board chair. They are accountable for the committee’s oversight function and are personally exposed if material risks are not surfaced or if management responses are inadequate. This accountability shapes the chair’s posture in committee meetings — they tend to probe more systematically and are less likely to accept management framings at face value than a board chair in a commercial presentation.

Pre-briefing the audit committee chair before the meeting is the single most effective preparatory step that most finance leaders skip. A conversation of twenty to thirty minutes before the meeting achieves several things: it alerts the chair to any sensitive findings before they encounter them in the session, it allows the chair to indicate whether they have any specific areas of focus the committee has agreed to prioritise, and it gives you the opportunity to align on how the meeting will run procedurally.

A pre-briefed chair is also more likely to help manage the meeting constructively. When a committee member raises a question that has the potential to derail the session’s agenda, a chair who already has context can redirect the discussion more authoritatively. When an external auditor and management are in tension on a particular finding, a pre-briefed chair can frame the discussion in a way that acknowledges the difference without letting it dominate the meeting.

The pre-briefing conversation should not be used to negotiate the framing of findings or to secure the chair’s endorsement of a particular management position. Its purpose is alignment on process and context, not agreement on substance. A chair who feels that a pre-briefing conversation was used to pre-empt scrutiny rather than facilitate it will approach the full committee meeting with heightened scepticism.

For more on managing post-presentation follow-through with audit and board committees, the article on board presentation follow-up protocols covers how finance leaders structure the commitments made in governance meetings and report back reliably to the same audience at the next cycle. The same rigour that applies to audit committee presentations extends to the follow-through process. Also worth reading alongside this: the related article on dashboard presentations for finance directors, which covers the data framing principles that apply to all senior data and finance briefings.

Executive Slide System — £39, instant access

Build Governance Presentations That Demonstrate Credibility Under Scrutiny

The Executive Slide System includes slide templates, AI prompt cards, and scenario playbooks for finance leaders who present to audit committees, risk committees, and governance bodies where the standard of evidence and precision is higher than in commercial settings.

Get the Executive Slide System →

Designed for CFOs, internal audit heads, and finance leaders presenting to governance and compliance committees.

Frequently Asked Questions

How long should an audit committee presentation typically run?

Most audit committee presentations run between 20 and 40 minutes for the management briefing section, with additional time allocated for the auditor’s independent update and committee discussion. The management presentation itself should not exceed 25 minutes — audit committee time is heavily protected and committees will be frustrated by presentations that run over their allocated slot. The four-section structure helps with pacing: if you know each section has roughly five minutes, you can calibrate your level of detail accordingly.

What is the most common mistake finance leaders make in their first audit committee presentation?

The most common error is applying the framing conventions of a board presentation — where positive findings are emphasised and sensitive matters are contextualised before they are stated — to an audit committee context where that approach reads as evasive. Audit committee members are specifically trained to notice when material risks are being managed rather than disclosed. The correction is simple: state findings directly and then provide context, rather than leading with context to soften what follows.

Should the CFO always present to the audit committee, or can another finance leader lead?

The CFO typically leads the management presentation to the audit committee, but it is increasingly common — and strategically useful — to have a direct report lead specific sections or the entire briefing, particularly for routine quarterly reviews. This serves two functions: it develops governance presentation capability in the finance leadership team, and it demonstrates to the committee that the control environment is being managed at an operational level rather than being supervised only from the CFO level. Where a direct report leads, the CFO should remain present and available to contribute on questions of judgement or materiality.

The Winning Edge — Weekly Newsletter

One Insight Per Week on Executive Communication

Each week, The Winning Edge delivers one focused insight on executive communication — structure, delivery, influence, and the mechanics of getting senior audiences to yes. Straightforward, applicable, and written for people who present under pressure.

Free download: The Executive Presentation Checklist — a structured pre-presentation review covering structure, evidence sequencing, and delivery preparation.

About the Author

Mary Beth Hazeldine — Owner & Managing Director, Winning Presentations

With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, Mary Beth now advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and governance meetings. Winning Presentations is her specialist advisory practice.