Quick answer: Founder pitch anxiety is not a confidence problem; it is a structural problem dressed up as one. The four reasons successful founders freeze in investor meetings are: identity exposure (the firm is the founder, so questions about the firm feel like questions about them), evaluation asymmetry (the partner is judging the founder; the founder cannot judge back), the prepared-script trap (rehearsed answers collapse the moment the partner reframes the question), and the post-failure carry (a previous bad meeting compounds rather than fades). The rebuilding pattern has four moves: separate the firm from the founder, prepare for the question rather than the answer, run mock pitches with someone who has done partner-side diligence, and reset the nervous system in the 90 seconds before the meeting starts.

JUMP TO:

James, a second-time founder with a successful exit behind him, walked into a Sand Hill Road partner meeting last month and lost the first three minutes of his pitch to a freeze he had not experienced in fifteen years. His voice tightened on the problem slide. His prepared line about the addressable market came out in the wrong order. By the traction slide he had recovered, but the room had already cooled, and the questions that followed were the polite kind. He left the meeting more confused than disappointed. He had run two companies, sold one of them, and presented to investors hundreds of times. He could not work out why this meeting had broken something the others had not.

The pattern is more common than the headlines about confident founders suggest. The most experienced entrepreneurs — second-time founders, operators with public-company backgrounds, executives who have presented to boards for two decades — describe a specific kind of freeze that hits them only in investor meetings. It does not happen in board meetings, all-hands meetings, customer pitches, or press interviews. It happens in the partner meeting, with money on the table, and the freeze comes from a different place than the standard speaking anxiety that founders experience earlier in their careers. Diagnosing it correctly is the first step in addressing it.

This piece walks through the four structural reasons high-functioning founders freeze in investor pitches, the rebuilding pattern that works for founders who have already tried the standard speaking-anxiety toolkit and found it insufficient, and the 90-second reset that sits in the corridor outside the meeting room. The framing is for second-time founders and experienced operators raising at Series A or later — the pattern looks different at pre-seed and seed, where the freeze usually has different roots. If the freeze is novel, sudden, and confined to investor meetings, the structural diagnosis usually fits.

If you are heading into a high-stakes pitch and the anxiety has started compounding:

Conquer Your Fear of Public Speaking is a structured programme covering the cognitive and physiological techniques that work specifically for high-functioning professionals — including founders who have presented for years and now find a freeze pattern they cannot reason their way out of.

Why founders who run companies still freeze in pitches

The investor pitch is structurally different from every other meeting an experienced founder runs. In a customer meeting, the founder is selling something the buyer can choose to take or leave; rejection is a business event. In a board meeting, the founder is presenting to people who are already invested and whose role is to support; rejection is rare and contained. In a partner meeting, the founder is the product, the rejection is personal, and the room is run by a partner whose job that day is to test whether the firm — and by extension the founder — is worth the partner discussion the following week. None of the founder’s other meeting types prepare them for that combination.

The second structural difference is the shape of the conversation. Most meetings the founder runs follow a familiar rhythm: the founder presents, the audience asks aligned questions, the meeting builds toward a decision the founder is helping to make. The partner meeting reverses that rhythm. The founder presents into a room that is already running its own internal evaluation in parallel with the pitch. The questions that surface are not the audience helping the founder; they are the partner testing the case against doubts the partner has not yet voiced. A founder who is used to being the most senior person in the room loses that orientation in a partner meeting. The freeze often follows the moment the founder notices the orientation has shifted.

The third structural difference is the recovery cost. In a board meeting, a stumble is absorbed by the relationship; the founder recovers in the next sentence and the meeting continues. In a partner meeting, a stumble in the first three minutes can compound through the rest of the pitch — the founder notices the freeze, the noticing introduces fresh anxiety, the fresh anxiety produces a second stumble, and by the unit-economics slide the founder is presenting around the freeze rather than through it. Experienced founders know this is happening and that knowledge is part of what makes it worse. Naming the structural difference is the first move in stopping the compound. For a closely related discipline on holding composure under high-stakes scrutiny, see our piece on conquering speaking fear.

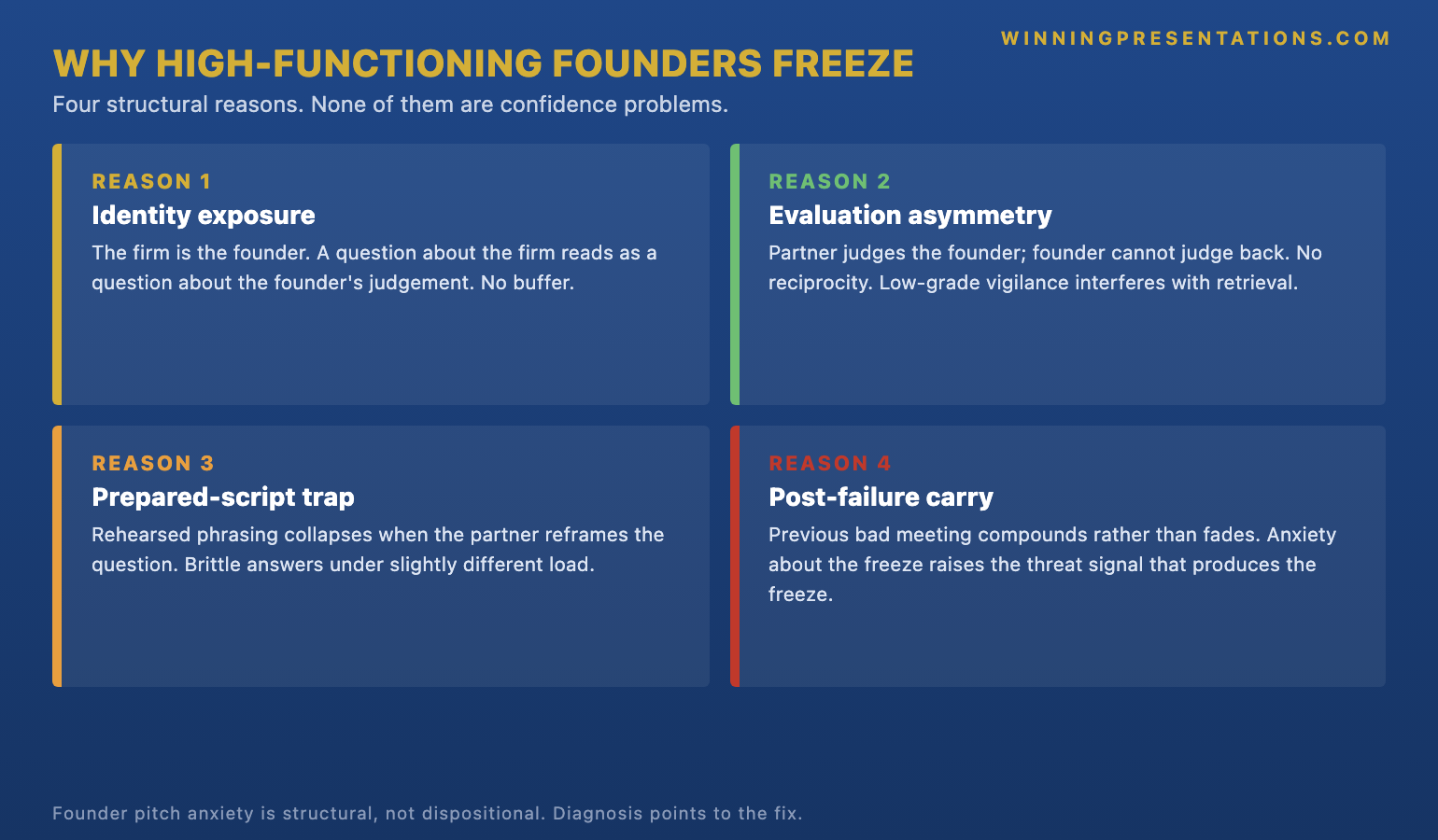

Identity exposure: the firm is the founder

The first of the four reasons is identity exposure. In a Series A pitch, the firm and the founder are not yet structurally separated. The team is small, the strategy is the founder’s, the moat is the founder’s bet, and the investor is funding the founder’s judgement as much as the firm’s product. A question about whether the firm has the right go-to-market motion is a question about the founder’s commercial instinct. A question about whether the unit economics work is a question about the founder’s analytical rigour. A question about whether the moat is defensible is a question about whether the founder has read the platform shift correctly. The founder cannot put the firm in front of them as a buffer the way an executive at a public company can.

The freeze pattern that traces back to identity exposure has a specific signature: the founder hears a question, recognises it as a fair question, knows the answer, and finds the answer dissolving as they reach for it. The cognitive system that retrieves the answer is being interrupted by the threat-detection system that is reading the question as a personal evaluation. Both systems are running on the same neural real estate; whichever one wins, the other goes quiet. Founders who are operating in public-company settings have decades of practice at letting the retrieval system win because the threat-detection signal is weaker. In a partner meeting, the threat-detection signal is louder and the founder has not yet built the practice to override it.

The structural fix is to externalise the firm before the meeting. Not by pretending the firm is separate from the founder — that pretence collapses under the first hard question — but by writing down, the day before the meeting, the three things about the firm that are true regardless of how the meeting goes. The customer cohort with retention numbers above 110 per cent. The integration backlog with seven enterprise pilots already in flight. The proprietary data set with named volume. Those facts exist independent of the partner’s evaluation. Walking into the meeting with those facts mentally pinned reduces the identity-exposure load because the firm now has substance the founder is reporting on, not embodying. For a closely connected discipline on holding poise in high-stakes settings, see the VC pitch deck template for 2026.

Evaluation asymmetry and the prepared-script trap

The second reason is evaluation asymmetry. The partner is judging the founder; the founder cannot judge back, at least not in any way that affects the meeting. In every other meeting the founder runs, there is reciprocity: the customer can be judged on whether they are a good fit for the product, the board member can be judged on whether their advice is sound, the press interviewer can be judged on whether they have done their reading. The partner meeting removes that reciprocity. The founder is being scored on a rubric they cannot see, by a partner whose own performance is invisible to them, with consequences that fall entirely on the founder’s side. That asymmetry produces a low-grade vigilance state that interferes with the natural rhythm of presenting.

The third reason — the prepared-script trap — compounds the second. Founders who have experienced the freeze once tend to over-prepare for the next meeting, rehearsing exact phrasing for each anticipated question. That preparation produces brittle answers that depend on the partner asking the question in the form the founder rehearsed. Partners rarely ask questions in the form the founder rehearsed. They reframe, they compress, they pivot to a related question the founder did not anticipate. A founder who has rehearsed exact phrasing finds the rehearsed answer dissolving as they reach for it because the question that was asked is not the question they prepared for. The freeze that follows looks like the freeze caused by identity exposure but has a different mechanism: it is the brittle script collapsing under a slightly different load.

The fix is to prepare for the question rather than the answer. Before the meeting, list the twelve to fifteen questions the partner is likely to ask. For each question, write three or four bullet points of substance the answer needs to cover — not the exact phrasing, just the load-bearing facts. The founder walks into the meeting with the facts at the front of mind and the phrasing forming in real time. The phrasing that emerges in the room is almost always tighter and more credible than rehearsed phrasing because it is being constructed in response to the actual question asked, not the question the founder anticipated. This is a different rehearsal discipline from the one most founders default to; it is also the one that holds when the question reframes.

Stop rehearsing exact phrasing. Start preparing for the question, not the answer.

Conquer Your Fear of Public Speaking is the structured programme for senior professionals who have presented for years and now find a freeze pattern they cannot reason their way out of. Cognitive and physiological techniques that work specifically for high-functioning founders and operators.

- Diagnostic framework for identifying the structural cause of the freeze

- The cognitive techniques that work for analytical, high-functioning professionals

- Physiological reset patterns for the 90 seconds before the meeting starts

- Mock-pitch protocols and recovery routines after a meeting that did not land

The four-move rebuilding pattern

The fourth reason is the post-failure carry. A founder who froze in a previous meeting often arrives at the next meeting carrying that earlier event as fresh emotional weight. The carry compounds: the founder is now anxious about the freeze recurring, that anxiety raises the threat-detection signal, the higher signal makes the freeze more likely, and the founder ends up confirming the very pattern they were trying to avoid. The carry can stretch across weeks and across multiple meetings, and it does not respond to the same toolkit that resolves identity exposure or evaluation asymmetry. It responds to a separate set of moves designed for cumulative anxiety.

The four-move rebuilding pattern addresses all four reasons in sequence. Move one: name the firm in three concrete facts the day before the meeting, separating the firm from the founder. Move two: list the twelve to fifteen likely questions and prepare bullet-point substance for each, replacing rehearsed phrasing with substantive scaffolding. Move three: run a mock pitch with someone who has done partner-side diligence — not a friendly board member, not a fellow founder, but an operator who has sat on the partner side of a partner meeting at least once. Move four: in the 90 seconds before the meeting starts, run a physiological reset — slow exhales, a posture reset, and three sentences of internal monologue that name the firm’s facts rather than the founder’s anxiety.

The mock-pitch move is the one founders most often skip. Mock pitches with partners or with operators who have sat partner-side run differently from mock pitches with co-founders or board members because the questions are sharper and the silences are longer. Both elements expose the brittle phrasing and the identity-exposure freeze in advance, where they can be addressed. A founder who has run two well-designed mock pitches in the week before the meeting walks in calibrated to the rhythm; a founder who has run six rehearsals with their co-founder walks in calibrated to a friendly rhythm and has to recalibrate in real time when the meeting opens. For more on the slide structure that supports a credible pitch, see our piece on the 10-minute investor pitch format.

The 90-second reset before the meeting starts

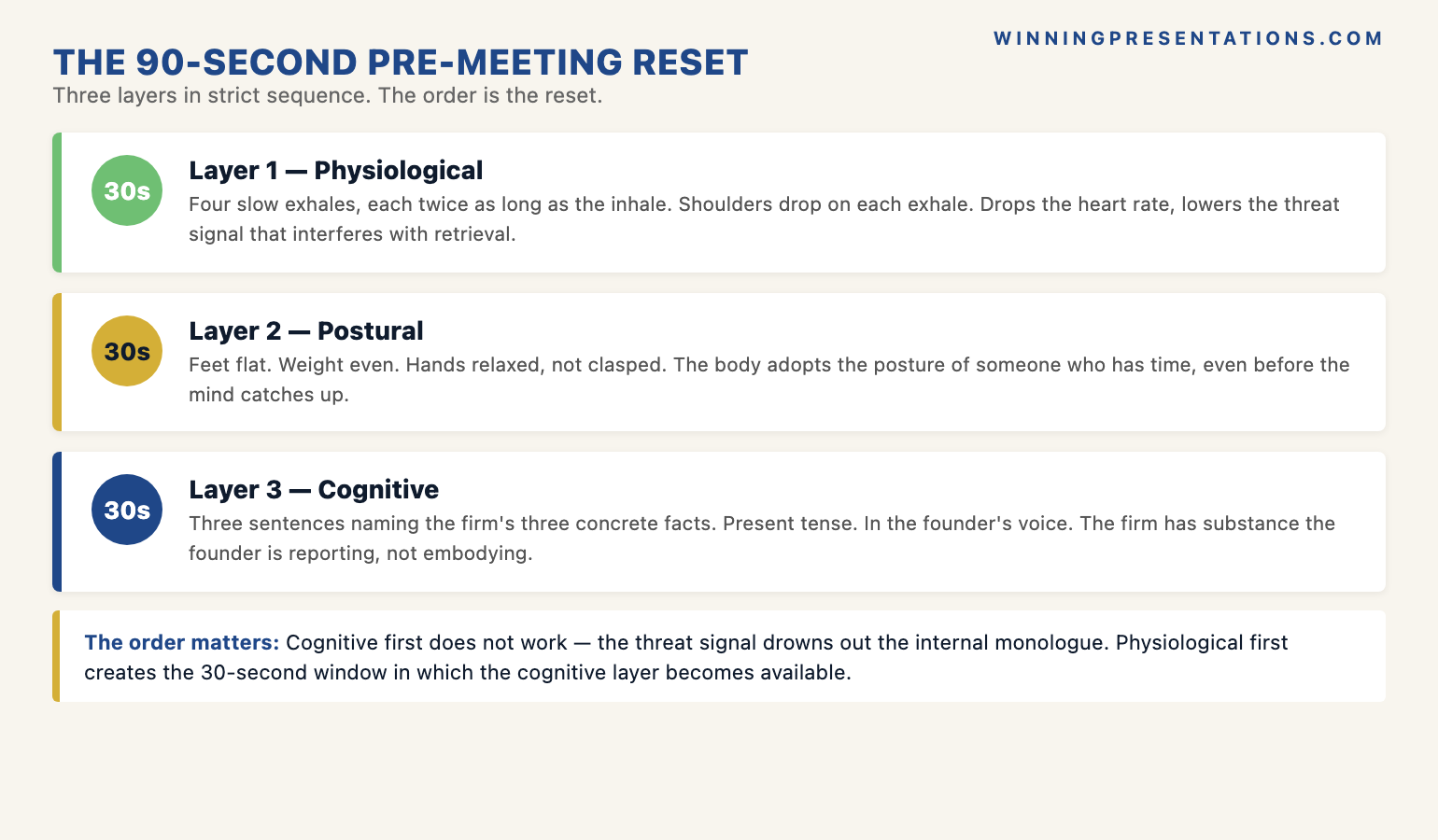

The reset that works in the 90 seconds before the meeting has three layers. The first is physiological: four slow exhales, each twice as long as the inhale, with the shoulders dropping on each one. The exhale-dominant breath drops the heart rate and lowers the threat-detection signal that interferes with the retrieval system. The second is postural: feet flat on the floor, weight distributed evenly, hands relaxed rather than clasped. The body adopts the posture of someone who has time, even if the mind has not yet caught up. The third is cognitive: three sentences of internal monologue that name the firm’s three facts — “Customer cohort retention above 110 per cent. Seven enterprise pilots in flight. Proprietary data set covering eighteen months.” — repeated in the founder’s own voice, in present tense, before the door opens.

The order of the three layers matters. Founders who try to start with the cognitive layer find that the threat-detection signal drowns out the internal monologue — the firm’s facts do not land because the body is still in vigilance state. Founders who lead with the physiological layer find that the breath and posture work creates a 30-second window in which the cognitive layer becomes available. The physiological reset has to come first; the postural reset reinforces it; the cognitive reset closes it. Trying to reverse this order produces a reset that feels like work and rarely lands. The 90 seconds is enough if the layers run in the right sequence.

For founders who need a tighter pre-meeting reset and in-meeting recovery toolkit:

Calm Under Pressure is a focused programme on the physiological and cognitive techniques that work in the moments before and during high-stakes presentations — covering the 90-second reset, in-meeting recovery moves, and the post-meeting decompression that prevents the freeze from compounding into the next meeting. £19.99, instant download.

The reset also has to survive a meeting that runs late. Partner meetings often start ten or fifteen minutes after the scheduled time; the founder who has timed the reset to the scheduled minute finds themselves running it twice and arriving at the meeting with the second reset already fading. A more robust pattern: run a longer reset 15 minutes before the scheduled time, then a shorter version — two slow exhales and the three-sentence internal monologue — in the 60 seconds before the door actually opens. That two-stage reset holds up to the variability of partner meeting timing in a way the single 90-second pre-meeting reset does not. For more on the underlying anxiety dynamics, see our companion piece on handling the “what’s your moat” question.

Frequently asked questions

Why does pitch anxiety hit experienced founders harder than first-time founders?

The structural reasons are sharper. A first-time founder has lower expectations of themselves and lower internal stakes — failure in a first meeting is anticipated and absorbed. An experienced founder, especially one with a previous successful exit, has internalised a self-image as someone who closes meetings. A freeze in front of a Series A partner is a violation of that self-image, and the violation produces additional cognitive load that compounds the freeze. First-time founders feel the room; experienced founders feel the room and feel themselves not feeling it the way they should, which is a heavier load. Naming this asymmetry is part of the rebuilding pattern.

Should I tell the partner I am nervous?

No. Disclosure of anxiety in a partner meeting is read as a credibility signal in the wrong direction; it tells the partner that the founder is fragile under pressure, which is the question the partner is silently asking. The founder who acknowledges nerves and continues at pace lands worse than the founder who quietly absorbs the nerves and continues. The exception: if the founder freezes visibly for more than three or four seconds, a brief recovery line — “let me come back to that” or “give me a moment to phrase that properly” — is better than continuing to push through the freeze. That recovery line is not a disclosure of anxiety; it is a competent management of the moment, and partners read it as such.

How long does it take to rebuild after a meeting that froze?

For most founders, two to three meetings of disciplined preparation plus the four-move rebuilding pattern. The carry from a single bad meeting fades over the next two pitches if those pitches are run with a different preparation discipline. Founders who continue to over-rehearse phrasing rather than substance often find the freeze recurring in the next meeting because the underlying mechanism has not changed. The rebuilding is not a function of how many meetings the founder runs; it is a function of how the next two meetings are prepared. With the right preparation, the carry usually clears within a fortnight. Without it, the carry can persist across the entire round.

Is it normal to feel this only in investor meetings and not in board meetings?

Yes, and the asymmetry is diagnostic. Board meetings have a relational buffer — the board is invested, the relationship has history, the room is on the founder’s side even when challenging the founder. Investor meetings have no such buffer at the partner-meeting stage. The freeze that surfaces only in investor meetings is structural rather than dispositional; the founder is not lacking in confidence generally, they are responding to a specific structural difference between the two meeting types. That diagnosis is good news, because it points the rebuilding pattern at the structural drivers rather than at general confidence work, which would be the wrong intervention.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate decks committees back from decks they defer. Subscribe to The Winning Edge →

Not ready for the full Conquer Your Fear of Public Speaking programme? Start here instead: download the free Investor Pitch Deck Checklist — a one-page reference for the slide structure investors expect.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.