Quick Answer

An ESG board presentation succeeds when it reframes sustainability as a financial risk management and regulatory compliance issue — not a values exercise. Boards respond to evidence of material financial exposure, regulatory timeline, and competitive positioning. Structure your case around the cost of inaction, not the benefit of good intentions.

Valentina had prepared for six months. The ESG strategy she was about to present to the board represented 14 months of internal analysis, three rounds of stakeholder consultation, and a £2.3 million programme of work already in flight. She opened her deck with a slide titled “Our Commitment to a Sustainable Future” and a photograph of a wind turbine.

The chairman interrupted within four minutes. “Valentina, what is the financial exposure if we don’t act on the regulatory timeline?” She hadn’t budgeted a slide for that question. She had budgeted three slides for the environmental impact section.

The board deferred. Not because they disagreed with the strategy — but because the presentation hadn’t addressed the question they were there to answer: what does this cost us if we get it wrong, and what does it cost us to get it right? Valentina came back three weeks later with a restructured case. The second presentation was approved in forty minutes.

The difference wasn’t the data. The data was the same. The difference was the frame — and for an ESG board presentation, the frame is everything.

Already preparing an ESG or strategic investment presentation?

The Executive Slide System includes slide frameworks and scenario guides designed for board-level investment cases, regulatory updates, and strategic reviews. It may save you several hours of deck-building.

Why ESG Presentations Fail at Board Level

Most ESG presentations are built by people who are deeply invested in the agenda — and that investment shows in the wrong way. The deck prioritises conviction over clarity, commitment metrics over financial consequence, and ambition over accountability. The result is a presentation that reads well internally and falls flat in the boardroom.

Board members are not opposed to ESG. Most non-executive directors have seen the regulatory direction of travel, the investor pressure, and the reputational risk clearly enough. What they are resistant to is an ESG presentation that does not speak their language. And their language is risk-adjusted return, regulatory liability, and strategic positioning — not carbon neutrality targets expressed as a percentage against a 2019 baseline.

The structural problem is one of audience mismatch. Sustainability teams build presentations for people who share their expertise and their concern. Boards need presentations built for people who are accountable for everything the organisation does — and who need to allocate capital, manage risk, and respond to regulators. These are different cognitive frames, and they require different slide structures.

There is a second, more subtle failure: the absence of a clear decision request. Many ESG board presentations are structured as updates rather than approval requests. They inform rather than ask. Boards, as a strong board presentation always demonstrates, are decision-making bodies — not audiences. When a presentation has no decision at its centre, the board has no reason to engage with it as a business matter.

The Three Questions Your Board Is Actually Asking

Before structuring a single slide, it is worth knowing what question your board is sitting with when you stand up to present. In twenty-five years of working with boards across financial services, technology, and regulated industries, I have observed that ESG presentations face three questions that are rarely stated explicitly but are always present.

Question one: What is the cost of inaction? Board members want to understand what happens to the organisation if it does nothing — or does less than the regulatory and investor environment now requires. This includes regulatory fines, loss of institutional investor support, reputational damage in key markets, and exclusion from certain procurement frameworks. This question should be answered on your second or third slide, not buried at the back.

Question two: Is the investment sized correctly? Boards are sceptical of ESG programmes that appear to have been sized to the ambition rather than to the risk. They want to see a clear relationship between the investment proposed, the regulatory requirement it addresses, and the timeline it operates within. Vague programme costs presented alongside aspirational targets trigger concern, not confidence.

Question three: Who is accountable, and how will we know if it is working? ESG programmes that lack clear governance, named accountable executives, and measurable near-term milestones read as activity plans rather than business strategies. Boards approve strategies, not activity plans. Accountability and measurement must be explicit in the presentation, not relegated to an appendix.

Building the Financial Materiality Argument

Financial materiality is the concept that determines whether an ESG issue is significant enough to affect the organisation’s financial performance, position, or prospects. It is also the concept that most ESG presentations skip — presenting sustainability as important in principle, rather than important to the numbers.

Your first task is to map each major ESG risk to a financial line. Carbon regulation exposure maps to operating cost and potential liability. Supply chain sustainability gaps map to procurement risk and contract continuity. Water and resource intensity maps to input cost and operational resilience in stressed conditions. Governance failures map to regulatory sanction, director liability, and the cost of remediation. Each of these connections should be quantified where possible — even a directional range is more useful to a board than a qualitative description.

The second task is to separate the investment request from the broader ESG ambition. Boards can find it difficult to approve a programme when they cannot distinguish the regulatory minimum from the aspirational target. Structure your investment request into clear tiers: what is required for regulatory compliance, what is required for investor and disclosure standards, and what is discretionary for competitive positioning. This tiering approach gives the board a decision framework rather than a binary yes or no to a single large number.

Building a robust capital expenditure business case follows the same logic: the financial case must stand independently of the strategic rationale. See this analysis of structuring a capital expenditure presentation for the principles that apply equally to ESG investment requests.

Build Your ESG Business Case on Slides Boards Can Approve

The Executive Slide System — £39, instant access — gives you slide templates for executive scenarios including investment approvals, regulatory updates, and strategic reviews. Each template comes with AI prompt cards to structure your financial materiality argument, and framework guides that organise complex data the way board-level decision-makers read it.

- Slide templates for executive scenarios including board investment approvals

- AI prompt cards to build financial materiality and risk arguments

- Framework guides for regulatory and governance presentations

- Scenario playbooks for strategic board-level decisions

Get the Executive Slide System →

Designed for executives who present investment cases, strategic proposals, and regulatory updates to boards and senior leadership teams.

Connecting Regulatory Risk to Business Continuity

Regulatory risk is the argument that boards respond to most reliably, because it is the argument they cannot defer. ESG regulation has moved from voluntary disclosure frameworks to mandatory reporting requirements across most major economies. In the UK, TCFD-aligned reporting is mandatory for listed companies and large private businesses. In the EU, the Corporate Sustainability Reporting Directive extends equivalent obligations across a broad range of organisations. US SEC climate disclosure rules are advancing. The regulatory window is closing.

In your ESG board presentation, the regulatory timeline should appear early — ideally as a visual timeline slide that shows which obligations are already active, which are incoming within twelve months, and which are on the horizon within three years. This is not an exercise in alarm; it is an exercise in planning. Boards respond to clarity about the regulatory environment because it transforms ESG from an aspiration into an operating requirement.

The connection to business continuity is made by demonstrating what non-compliance or inadequate disclosure costs the organisation specifically. This means identifying your major investors and understanding their stewardship codes and voting policies. It means identifying key clients and procurement frameworks that now require ESG disclosure as a condition of contract. It means naming the jurisdictions in which you operate and the specific regulatory obligations that apply. The more specific this analysis, the more persuasive it is.

Where organisations face genuine uncertainty — about regulatory interpretation or the pace of enforcement — it is better to acknowledge this explicitly and present a range of scenarios than to present a false precision that erodes board confidence when the position shifts. Handling this kind of pre-emptive objection management is covered in the approach outlined for managing objections in executive presentations.

The Executive Slide System includes framework guides specifically designed for regulatory and compliance presentations, where the challenge is translating legal complexity into a decision-ready executive summary. If you are building a regulatory exposure slide, those templates give you a starting structure that connects obligation to operational impact without requiring a legal degree to read.

The Slide Structure That Moves ESG from Discussion to Decision

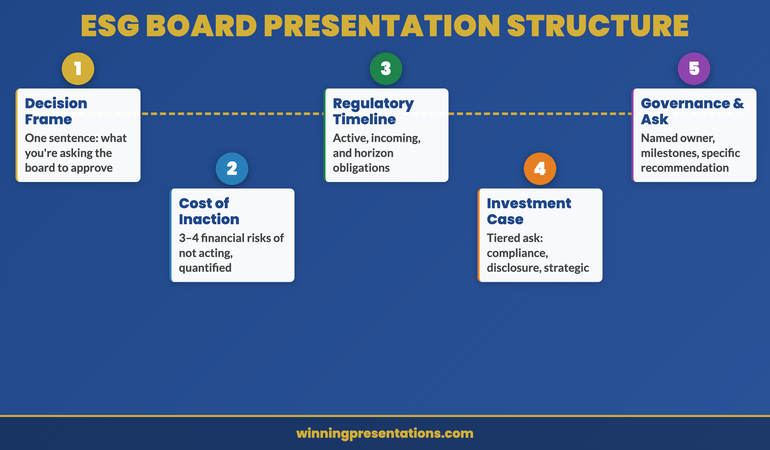

A board-ready ESG presentation follows a structure that is closer to an investment memorandum than a sustainability report. The purpose of each slide is to advance a specific part of the argument, not to demonstrate the depth of your team’s work.

Slide 1 — The decision framing: State what you are asking the board to approve, in one sentence. Not a title slide, not a contents page — an immediate framing of the decision. “We are requesting approval of a three-year ESG programme at a total investment of £X, to address our TCFD reporting obligations, manage our material ESG risk exposure, and maintain institutional investor alignment.”

Slide 2 — The cost of inaction: A clean summary of the three to four material financial risks of not acting, with approximate financial ranges where quantifiable. This slide should be sober and specific — not alarming, not vague.

Slides 3–4 — The regulatory and investor context: A timeline of obligations and a summary of investor expectations relevant to your top fifteen shareholders. Facts, not advocacy.

Slides 5–6 — The investment case: Your tiered investment request broken down by regulatory requirement, disclosure standard compliance, and strategic positioning. Include a clear statement of what is not included in this request and why.

Slide 7 — Governance and accountability: Named executive owner, board oversight mechanism, and the four to six milestones by which progress will be measured in the next twelve months.

Slide 8 — The recommendation: A one-slide summary of what you are asking the board to approve, with the specific motion or resolution if relevant. End with the ask, clearly stated.

Handling Sceptical Questions on ESG ROI

Scepticism about ESG ROI is legitimate, and your response to it should treat it as such. The most common challenge takes the form of: “Where is the financial return on this investment?” The honest answer, in most cases, is that the primary return is risk mitigation rather than revenue generation — and that is a valid financial argument if you make it clearly.

Frame ESG investment the same way you would frame insurance or compliance cost: the return is not a revenue line, it is the avoidance of a larger cost. Regulatory fines, exclusion from institutional investor portfolios, reputational damage in key markets, and supply chain disruption are all quantifiable avoided costs. A board that approves a £500,000 ESG programme to avoid a potential £4 million regulatory exposure and loss of a major institutional investor position is making a straightforward financial decision.

Where genuine revenue opportunity exists — in ESG-linked procurement contracts, in access to green financing instruments, or in the opening of sustainability-conscious consumer segments — quantify it conservatively and present it as upside, not as the primary case. Boards that see ESG ROI presented as primarily a revenue opportunity become sceptical. Boards that see it presented as primarily risk management become engaged.

A second common challenge is the “not our problem” response — a version of competitive risk assessment where the board questions whether inaction puts the organisation at a disadvantage compared to peers who are also moving slowly. Your response here is competitor benchmarking data. If two of your three main competitors have already committed to TCFD-aligned reporting, you can present your current position as a laggard position rather than a conservative one. Board members who see their organisation behind peers on a regulatory and investor expectations curve are motivated to close the gap. For a related approach to building the strategic case for difficult investments, the workforce planning framework in our companion article on workforce planning presentations applies many of the same risk-frame principles.

People also ask: How long should an ESG board presentation be? A board ESG presentation should be between eight and twelve slides, presented in twenty to thirty minutes with time allocated for questions. Longer presentations signal that the presenter has not been able to prioritise the decision-relevant information. Brevity is not about limiting the content — it is about demonstrating that you understand what the board needs to decide and have structured your case accordingly.

People also ask: Should I include ESG metrics and targets in the board presentation? Include only the metrics that are directly relevant to the investment decision, the regulatory obligation, or the investor expectation you are addressing. Three to five key metrics with clear baselines and milestones are more useful to a board than a comprehensive ESG scorecard. Full metric reporting belongs in the ESG or sustainability report, not the board approval presentation.

People also ask: How do I get board buy-in for ESG when there is scepticism? Lead with the regulatory and investor obligation, not the ethical case. Sceptical board members rarely resist ESG investment when it is framed as a compliance and risk management requirement. They resist it when it is framed as a values commitment. Present the regulatory timeline, identify the specific investors who have flagged ESG as a stewardship priority, and make the cost of inaction specific. This converts a values debate into a business decision.

Structure Your ESG Slides the Way Boards Read Investment Cases

The Executive Slide System — £39 — includes scenario playbooks and framework guides structured for strategic investment approvals, regulatory compliance cases, and board-level risk presentations. Stop rebuilding your deck from scratch each time a board deadline approaches.

Get the Executive Slide System →

Designed for executives who present to boards, audit committees, and senior leadership teams.

Frequently Asked Questions

What is the difference between an ESG report and an ESG board presentation?

An ESG report is a disclosure document — comprehensive, structured for external audiences, and designed to demonstrate performance against a range of metrics and standards. An ESG board presentation is a decision-support document — focused, structured around a specific investment request or strategic choice, and designed to enable a board to make or ratify a specific decision. The two documents have different purposes, different audiences, and different formats. Conflating them — by presenting the board with a summary of the ESG report — is a common source of board frustration.

How do I make an ESG presentation credible to financially focused board members?

Credibility with financially focused board members comes from three things: quantification, source attribution, and specificity. Quantify the financial exposure wherever possible — even directional ranges (“£1–3 million in potential regulatory exposure over five years”) are more useful than qualitative descriptions. Attribute your data to named sources: specific regulations, named investor stewardship codes, named competitor positions. And be specific about your organisation’s situation — avoid sector generalisations when you have company-specific data. Generic ESG arguments are easy to defer. Specific, quantified, sourced arguments are much harder to dismiss.

Should the CEO or the sustainability director lead the ESG board presentation?

The most effective ESG board presentations involve the CEO as sponsor and the sustainability director as the expert presenter — with the CFO present to field financial questions. When the CEO opens the presentation by framing ESG as a strategic business priority rather than a specialist programme, it changes the conversation before the first data slide appears. When the sustainability director presents the detailed case, they do so with executive sponsorship already visible. And when the CFO can confirm the financial analysis independently, board confidence in the numbers increases significantly. If this structure is not available, the presenter should at minimum have explicit CEO endorsement recorded in the board papers.

Get weekly presentation strategy in your inbox

Every Thursday, The Winning Edge delivers one actionable insight for executives who present to boards, committees, and senior leadership teams.

Free resource: Download the Executive Presentation Checklist — a one-page pre-presentation audit used by executives before high-stakes board and investment meetings.

About the Author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, regulatory approvals, and board decisions.