Quick answer: The H1 business review presentation pages a CFO reads first are the cash-and-capital page, the cost-recovery page, and the H2-guidance page — in that order, before the meeting starts, often in the printed pre-read on the train in. The CFO scans the three pages to answer three questions: is the H1 cash position consistent with the operating story, are the costs recovering against the H1 plan in the direction the previous board paper committed to, and is the H2 guidance the leadership team is now putting forward defensible against the H1 trajectory. If all three pages answer cleanly, the CFO arrives at the meeting prepared to engage with the rest of the deck. If any of the three reads as evasion, hedging, or analytical thinness, the CFO arrives with a list of pre-meeting questions and the rest of the deck gets read in that light. Knowing which three pages decide the CFO’s frame is the difference between a half year business review presentation the CFO supports and one the CFO probes.

JUMP TO:

- Page one: cash and capital, before the operating story

- Page two: cost recovery against the H1 plan

- Page three: the H2 guidance, with the leader’s name against it

- The pre-read ritual: how CFOs actually read the deck

- The CFO-first diagnostic for the day before the review

- One thing to do before the next H1 review

- Frequently asked questions

In mid-2007 I was preparing a senior client — an operating-line head at one of the European universal banks — for an H1 business review at the group executive committee. We sat together on a Wednesday morning two days before the committee, going through her 28-slide deck slide by slide. She walked me through the analytical journey she had built: market context on slide three, the H1 revenue bridge on slides eight through eleven, the channel deep-dive on slides twelve through fifteen, the cost slides on sixteen and seventeen, the cash and capital position on slide twenty-three. I asked her one question. “What does the group CFO read first when he gets this on the train tomorrow morning.” She paused, then said “the cover, then probably the bridge.” I asked her to call the CFO’s chief of staff and put the question to him directly. The chief of staff laughed and said: the CFO turns to the cash and capital page first, then the cost recovery page, then the H2 guidance, in that order, before he reads anything else. By the time the meeting starts, those are the three pages he has already formed a view on. Everything else is read against that view. My client moved the cash and capital page from slide twenty-three to slide five, restructured the cost-recovery slide as a recovery-against-plan view rather than a year-on-year comparison, and rewrote the H2 guidance into one explicit recommendation rather than three options. The CFO opened the deck on the train, read the three pages in order, called her at seven that evening, and told her the deck was ready to take to the committee.

(This article was created with AI assistance; all stories and insights are based on 35 years of real client work.)

This piece walks through the three pages a CFO reads first in an H1 business review presentation, in the order they get read, and the reason that reading order — not the deck’s authored sequence — is the order that decides whether the CFO arrives at the meeting supporting the leadership team or probing it. The pattern is one I have watched across about a dozen senior banks, insurers, and consulting firms over fifteen years of coaching operating-line heads through H1 reviews. CFOs do not read the deck cover-to-cover. They scan three pages in a specific order on the way in, form a view, and then read the rest of the deck against that view. The pages and the order are the same across the firms I have watched. Knowing them changes how the deck gets built.

The ten questions every CFO asks, with sample scripts, are the next-best companion to this article.

The 10 Questions Every CFO Asks (+ Scripts) is the free reference covering the recurring questions CFOs put to operating-line heads on H1 reviews — cash, costs, channel mix, capital allocation. Free download, no email gate.

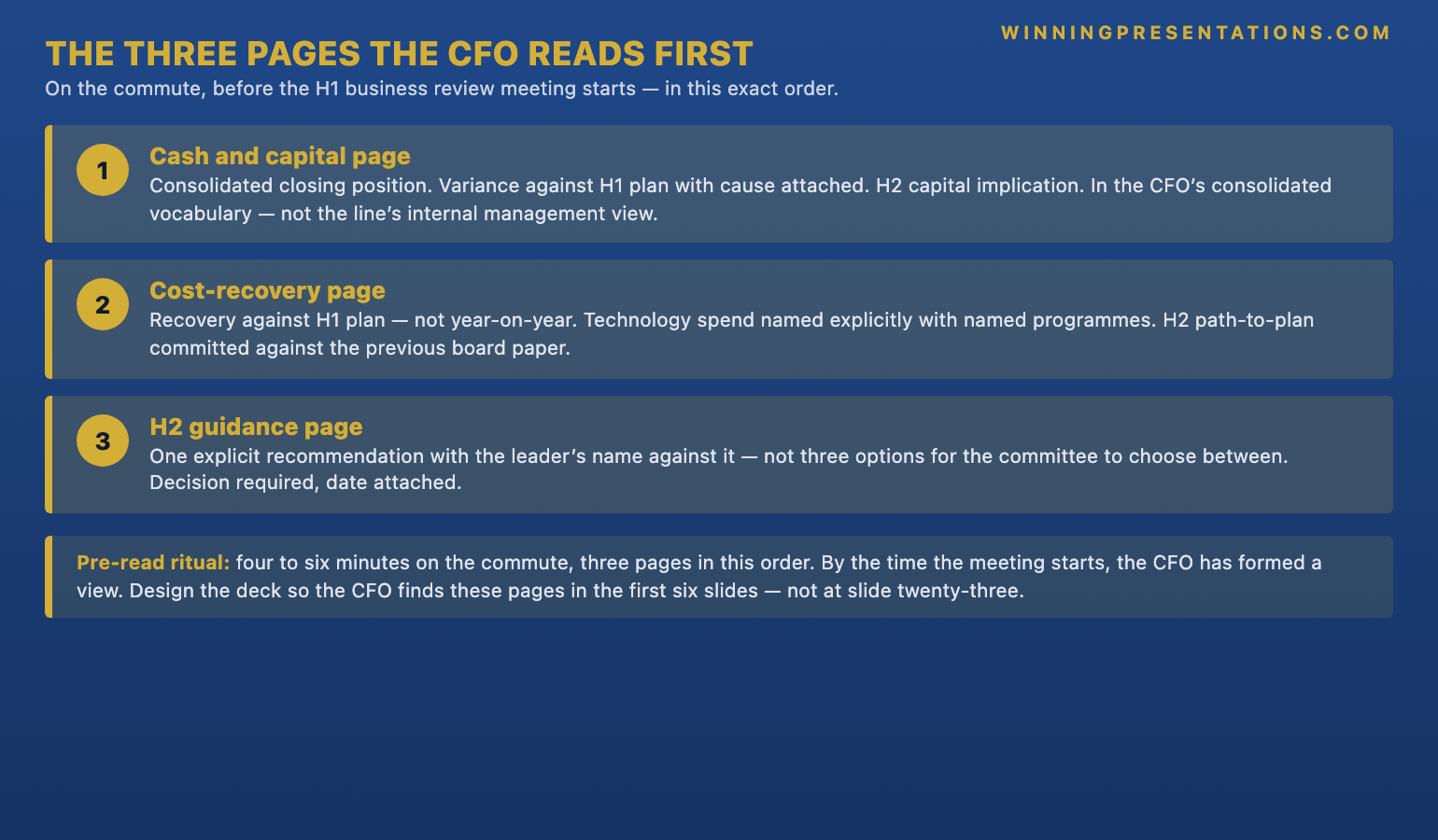

Page one: cash and capital, before the operating story

The CFO reads the cash and capital page first, before the revenue bridge, before the channel deep-dive, and before any of the market-context pages most line heads put at the front of the deck. The reason is structural rather than personal. The CFO carries the firm-wide responsibility for the consolidated cash and capital position; the H1 business review is one of perhaps eight or ten such reviews the CFO will read in the same week, and the consolidated picture is what the CFO has to be able to explain to the group CEO, the audit committee, the rating agencies, and the prudential regulator. A line-level H1 deck where the cash and capital page sits on slide twenty-three signals, to the CFO, that the line head has built the deck around the operating story and treated the cash position as a downstream consequence. The CFO reads that ordering as a leadership tell, even before reading the content of the page itself. Line heads who move the cash and capital page forward to slide four or five signal, by the move alone, that they understand how the CFO actually reads the deck.

The cash and capital page itself needs three things on it for the CFO to engage cleanly. The first is the H1 closing position in the consolidated terms the CFO uses elsewhere — not just the line’s own internal management view, but the view that will appear in the group’s external reporting. The second is the variance against the H1 plan, with the cause attached at one level of granularity. Capital consumption was £X above plan, of which £Y was driven by the higher-than-expected risk-weighted-asset growth in the broker channel, identified during Q2 and now reflected in the H2 distribution allocation is a defensible line. Capital consumption was slightly above plan due to portfolio mix is not. The third thing the page needs is the implication for H2 — whether the line is requesting any change to the capital envelope it was granted for H2, and if so, what change and on what basis. CFOs read those three elements in about forty seconds. Lines that have them ready get the engagement; lines that do not get the pre-meeting query.

The discipline of the cash and capital page is the discipline of writing in the CFO’s consolidated vocabulary rather than the line’s own management vocabulary. Most line heads run their internal cash and capital reporting on a different set of measures from the group consolidated view; the H1 deck instinctively reaches for the internal management measures. The CFO is reading for the consolidated measures. The translation between the two takes thirty minutes with a senior partner from the line’s finance team, in the week before the committee, and it is the single highest-leverage thirty minutes in the H1 review preparation. The 3Ps framework rehearsal cadence covers the upstream discipline where the vocabulary translation happens before the deck goes to print.

Page two: cost recovery against the H1 plan, in the direction committed

The CFO reads the cost-recovery page second. The page is not a generic costs slide; it is the page that answers one specific question the CFO is carrying into the meeting on every line review: are the costs in this line recovering against the H1 plan in the direction the previous board paper committed to, or have they drifted. The question matters because the CFO often spent capital and reputational credit at the previous board cycle defending the line’s cost-trajectory commitments to the audit committee or the remuneration committee or the chair. If the H1 line review reads, six months later, as though the cost commitments are slipping, the CFO has a problem with the same audit and remuneration committees that has nothing to do with this line’s individual performance and everything to do with the CFO’s credibility as the guarantor of the firm’s cost discipline. The CFO needs to know, from the cost-recovery page, whether they are about to face that conversation or not.

What the cost-recovery page therefore needs is not a year-on-year cost comparison, which is the natural framing for most line heads. It needs a recovery-against-plan view, with the H1 plan number, the H1 actual, the variance, and the H2 path-to-plan. If the H1 actual is above the H1 plan, the page needs the operational reason and the H2 corrective. If the H1 actual is on or below plan, the page needs the same structure with the H2 sustainability claim. The CFO is not reading for the headline number; the CFO is reading for whether the leader has built the recovery trajectory into a coherent picture that holds against the previous board commitment. A page that compares H1 2026 to H1 2025 is doing the wrong comparison. A page that compares H1 2026 to the H1 2026 plan is doing the comparison the CFO needs to make their own commitment work.

The other element the cost-recovery page needs is the line’s own view on cost mix — what proportion of the variance is people, what is technology, what is third-party spend — framed in the same categories the firm uses externally rather than the categories the line uses internally. CFOs in this generation of senior finance roles are particularly attentive to the technology-spend line because of the AI and platform investments that have absorbed unusual amounts of cost discipline conversation over the last eighteen months; a cost-recovery page that hides technology spend inside a generic “other” bucket reads as evasive, and the CFO will probe it pre-meeting. A page that names technology spend explicitly, attributes it to a small number of named programmes, and ties each programme to a return-of-investment commitment the line head will be measured against in H2, reads as transparent. Transparency on the cost-recovery page earns the CFO’s support for the line in front of the rest of the committee.

CFOs read three pages first. Building those three pages well is faster when the slide structure is already built.

The Executive Slide System is the slide library senior professionals use to build the cash-and-capital page, the cost-recovery page, the H2-guidance page, and the supporting structure CFOs and committees actually engage with — without rebuilding the structure from scratch every review cycle. Built on 24 years in corporate banking and 16 years coaching senior professionals across financial services, insurance, consulting, and technology.

- 26 Executive Templates — including cash-and-capital, cost-recovery-against-plan, and H2-guidance formats CFOs engage with cleanly

- 93 AI Prompts — rewrite the cash-and-capital sentence, the cost-recovery variance, and the H2-guidance recommendation in the firm’s consolidated vocabulary

- 16 Scenario Playbooks — including the H1 review, the board paper, the audit-committee update, and the H2-budget request

- 7 Checklists — the CFO-first diagnostic, the cost-recovery pressure test, and the H2-guidance defensibility check

- Instant download, lifetime access — usable across every review cycle, not just the one in front of you now — £39

Page three: the H2 guidance, with the leader’s name against it

The third page the CFO reads is the H2 guidance — the page that names what the line head is now putting forward for the second half of the year, given what H1 actually did. The CFO reads this page for two things. The first is whether the H2 guidance is consistent with the H1 trajectory shown in the cash-and-capital and cost-recovery pages, or whether the guidance assumes a non-trivial change in the trajectory that the line head has not yet justified. The second is whether the H2 guidance has the line head’s name against it as a personal commitment, or whether it is framed as a range of options for the committee to choose between. Guidance that is consistent with the H1 trajectory and named as a personal commitment passes both tests; the CFO arrives at the meeting prepared to support it. Guidance that hedges on either reads as evasion, and the CFO arrives with the pre-meeting question already written.

The H2 guidance page should contain four elements. The H2 revenue and profit envelope the line is now committing to, with the variance against the original H2 plan and the cause. The H2 cost envelope, with the recovery trajectory. The H2 capital allocation the line is requesting, with any change against what was previously granted. And the H2 leadership commitments — the three or four hard commitments the line head will be measured against at the year-end. Four elements, one page, no analytical content competing for attention. The CFO reads it in ninety seconds and either supports it or queries it. The hedged version of this page, which is the more common version, splits the envelope into two or three scenarios, presents the cost recovery as a range, and lists the capital request as “subject to the committee’s direction”. The CFO reads the hedged version as a leader who has not yet made up their mind, and the rest of the meeting unfolds accordingly.

The reason the H2 guidance page is so often hedged is that the line leadership team has not landed on a single H2 recommendation before the committee. Three options are still in play because the line head wants to test them with the committee. The committee declines that invitation, the CFO declines it most reliably of all, and the H2 guidance gets deferred to a follow-up session two weeks later. The H1 review ends without an H2 decision. The line loses three or four weeks of H2 momentum on whatever option they would have ended up recommending anyway. The fix is mechanical: the line head writes the H2 recommendation in one sentence two days before the committee, reads it to the line’s own CFO partner the same afternoon, takes the pressure-test, and walks into the committee with one recommendation rather than three options. The executive buy-in framework that walks H2 plans through committees covers the upstream discipline where the recommendation gets to one.

If H1 includes the AI and platform investments the CFO is now examining hardest, the secondary structure matters.

AI-Enhanced Presentation Mastery is the self-paced programme for senior professionals using AI (including Copilot) to structure the H1 review, the cost-recovery narrative around AI spend, and the H2 commitments on the AI programmes the CFO is most exposed on. 8 modules, 83 lessons, no deadlines, no mandatory session attendance. 2 optional live coaching sessions, fully recorded. Self-paced with monthly cohort enrolment. Lifetime access to materials. £499.

The pre-read ritual: how CFOs actually read the deck

The CFOs I have watched read H1 decks over the years follow a recognisable ritual that line heads almost never see and almost never design the deck for. The deck arrives in the CFO’s inbox the day before the committee, often at 5pm or 6pm. The CFO does not open it then. The CFO opens it on the commute the next morning, frequently on a printed copy because the page-flipping is faster than the screen scroll. The CFO reads the cover, turns directly to the cash-and-capital page wherever it sits in the deck, then to the cost-recovery page, then to the H2 guidance, in that order. The whole pre-read takes between four and six minutes. The CFO arrives at the committee with a view formed, three or four specific questions written in the margin of one of the three pages, and a sense of whether they are going to support the line head’s narrative or probe it.

The implication for the line head is that the deck’s authored sequence — cover, agenda, market context, revenue bridge, channel deep-dive, costs, cash, H2 — is the wrong reading order for the most senior reader in the room. The CFO will not encounter the deck in that order. The line head should design the deck so the CFO’s actual reading path lands on three well-built pages early in the sequence, even if the analytical journey then doubles back to a more traditional structure for the rest of the committee. Cash and capital on slide four. Cost recovery on slide five. H2 guidance on slide six. The remaining slides build the analytical journey for committee members who will read the deck more sequentially. The cost of the front-loaded structure is that the line head’s preferred storytelling arc is interrupted. The benefit is that the CFO’s pre-meeting view is formed on three pages the line head has consciously designed for them, rather than on three pages the CFO happens to find by flipping through the deck looking for them.

The same ritual generally applies, with small variations, to the chief operating officer, the chief risk officer, and the chief strategy officer — each scans the deck for the two or three pages they personally carry the firm-wide responsibility for, before reading the rest. The CFO’s three pages are the most uniformly observed and the most consequential, because the CFO sets the financial frame the rest of the committee operates within. Line heads who design for the CFO’s reading order find the CRO and COO frames adjust around it; line heads who design for their own authored sequence find each senior reader landing in a different place and the meeting starting fragmented. The structure boards engage with on update-and-decide sessions covers the equivalent reader-first design discipline at board level.

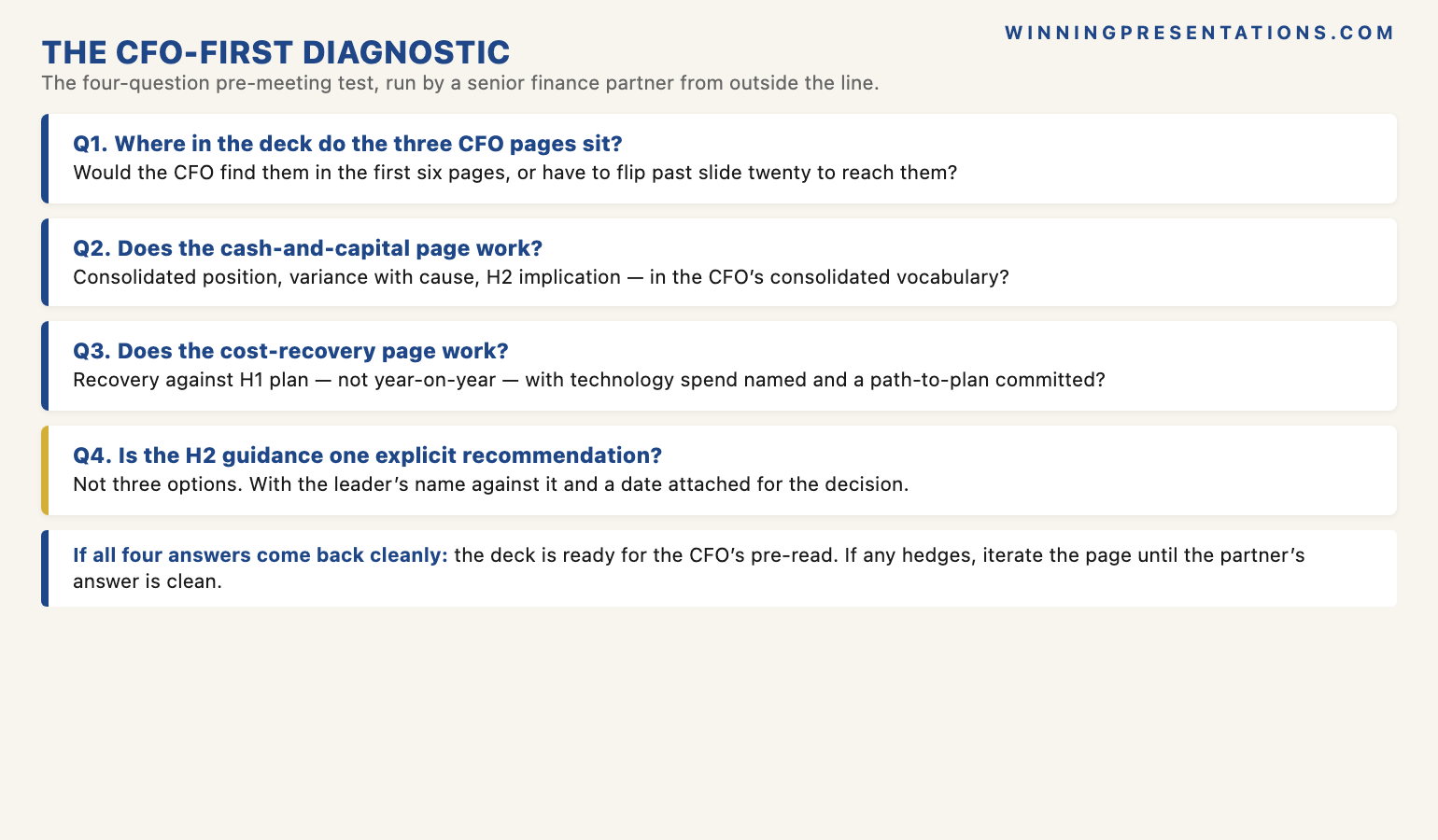

The CFO-first diagnostic for the day before the review

The diagnostic to run the day before an H1 review is mechanical. Print the cash-and-capital page, the cost-recovery page, and the H2-guidance page in the order they appear in the deck. Hand them to a colleague from outside the line — ideally a senior finance partner from a different business line or from group finance. Ask them four questions, in order. Where in the deck do these three pages sit, and would the CFO find them in the first six pages or have to flip past slide twenty to reach them. Does the cash-and-capital page show the consolidated position, the variance with cause, and the H2 implication. Does the cost-recovery page show recovery-against-plan with technology spend named. Is the H2 guidance one explicit recommendation, with the leader’s name against it, or a hedged set of options. If the colleague answers all four cleanly, the deck is ready for the CFO’s pre-read. If any answer is hedged or unclear, the corresponding page needs another iteration before the deck goes to the committee.

The diagnostic is mechanical because the line head is too close to the analytical work to read the three pages as the CFO will read them. The line head has spent three weeks inside the channel data and the bridge analysis; the CFO will spend four to six minutes on the commute. The colleague’s four-question pass is the closest available proxy for the CFO’s pre-read. Ninety minutes of iteration in the day before the committee is the difference between a CFO who supports the line head in the room and a CFO who probes the line head in the room. Both reactions are professional. The first is a great deal more useful for the line head’s H2 momentum.

One thing to do before the next H1 review

Two days before the committee, take the current draft of the H1 deck and move three pages to the front: cash and capital to slide four, cost recovery to slide five, H2 guidance to slide six. Do not rewrite the rest of the deck yet. Run the four-question diagnostic on the three pages with a senior finance partner from outside the line. Iterate the three pages until the partner can answer all four questions cleanly. Then, and only then, look at the rest of the deck and decide what genuinely supports the three front-loaded pages and what is decorative. The deck will get shorter. The H1 review will end with the committee engaging with the H2 ask rather than absorbing it. The CFO will read the three pages on the train in, form a view consistent with what the line head intended, and the meeting will start with the CFO in support rather than in probe.

Frequently asked questions

Won’t putting the cash and capital page on slide four disrupt the storytelling arc the rest of the committee expects?

The storytelling arc is a line-head construct, not a committee expectation. Most senior committees are not reading the deck in sequence either; the CFO leads a behaviour the COO, CRO, and chief strategy officer follow at slightly different page numbers. Line heads who optimise for an authored sequence are optimising for an audience that does not exist in senior committees. The committee’s actual expectation is that the most decision-relevant pages are visible early, and the analytical journey supports them. A cash-and-capital page on slide four signals exactly that. The committee almost never queries the structural choice; the line head’s own director or deal-team consultant is the one who tends to push back. The committee’s response, when the structure is right, is engagement.

What if the cash and capital position is in good shape and the line head wants to lead with the operating story instead?

The CFO still reads the cash and capital page first regardless of how strong the position is, and the reason is firm-wide context rather than line-level emphasis. The CFO needs to know quickly that this line is not introducing risk to the consolidated picture before they engage with the operating story. A clean cash-and-capital page on slide four releases the CFO to read the operating story; an absent or buried cash-and-capital page forces the CFO to look for the answer before they will engage with anything else. The leader who wants the operating story to land therefore needs the cash and capital page to be visible and clean first, precisely because that is what unlocks the room’s attention for the operating story afterwards. The two goals are not in tension; one enables the other.

How do I handle the H2 guidance page when the leadership team genuinely has not landed on a single recommendation?

You do not walk into the H1 review yet. The H2 guidance page with three options is a deferral request in disguise. The committee will return the request reliably, the H2 decision will be pushed to a follow-up session in two weeks, and the line will lose three or four weeks of momentum. The disciplined response is to postpone the H1 review slot by one week, take that week to land the recommendation inside the leadership team, and walk into the committee the following week with one H2 ask. A one-week postponement, with a clean recommendation, costs the line head less than a deferral with three options. The committee tolerates the postponement and respects the discipline. The deferral with options costs both the H2 momentum and the line head’s credibility on the next H2 cycle.

Does this pattern apply outside financial services — in technology, healthcare, or industrials?

The cash-and-capital ordering varies by sector. In financial services and insurance, the CFO scan is cash, capital, costs, H2 guidance. In a technology business where capital is less constrained, the CFO scan is closer to revenue trajectory, gross-margin trajectory, customer-acquisition cost recovery, and H2 guidance. In industrials, the scan typically prioritises working capital, operating cash flow, fixed-cost recovery, and the H2 capex plan. The pattern of three early pages plus an explicit H2 ask is sector-agnostic; the specific pages adapt to the sector’s capital structure. The line head’s job is to learn from the firm’s own chief of staff to the CFO which three pages the CFO actually opens first, and design the deck accordingly. The information is available within the firm; it just takes a thirty-minute conversation to surface.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly (Thursday) newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate the H1 reviews CFOs support from the ones they probe. Subscribe to The Winning Edge →

For the broader picture across slides, storytelling, confidence, and delivery, the seven-product Complete Presenter library is the bundle most senior professionals find useful as a single resource — £99 for everything, lifetime access.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises senior professionals across financial services, insurance, consulting, and technology on the structure of H1 business reviews, CFO-engaged board papers, and the H2-decision sessions that hinge on them.