Quick answer: A CFO presentation that secures budget sign-off uses an 8-slide structure: recommendation, financial ask, business case, comparative options, risk and mitigation, implementation plan, controls and reporting, and decision. Each slide does one job. The order matters because finance audiences read top-down — the recommendation appears first, the evidence supports it, and the controls answer the question every CFO is silently asking. Eight slides is the working ceiling. Fewer slides skip evidence the CFO needs. More slides usually mean the case is not yet sharp enough.

Jump to:

Adaeze had been refining the deck for two weeks. Twenty-three slides. Detailed financial modelling on slides 6 through 11. The strategic context up front. A long appendix. Her CFO listened politely for nine minutes, flicked to the slide showing the financial ask, then asked the question she had not prepared for: “What is the recommendation, and what would I be approving if I said yes today?” She had not put a recommendation on slide one. She had built up to it. The deck never recovered.

Two weeks later, with the same proposal, the same numbers, and a deck of eight slides, she got the sign-off. Nothing about the proposal had changed. The structure had. The CFO read the deck the way CFOs read decks — top-down, recommendation first, evidence second, controls third — and the deck answered her in that order rather than asking her to wait.

A CFO presentation template is not a design exercise. It is a structural decision about what gets answered first. The 8-slide format is the working ceiling for most budget sign-off conversations. Below eight slides and there is usually a missing piece of evidence the CFO needs to commit. Above eight slides and the deck is usually carrying weight that should sit in an appendix or a separate working document. Eight is where the deck and the audience meet.

If your last CFO presentation got pushed back for “more detail”

The Executive Buy-In Presentation System covers the structures senior professionals use when budget sign-off depends on a single conversation. 7 self-paced modules including stakeholder analysis, case construction, and the slide structures finance committees can approve. Monthly cohort enrolment, optional recorded Q&A.

Why eight slides — and why finance audiences punish more

CFOs and finance committees read decks differently from operational audiences. They do not need the journey. They need the conclusion, the evidence, and the controls — in that order. A deck that delays the recommendation is read as a deck that is hiding something or has not yet decided what it is asking for. Either reading damages credibility before the case is on the table.

Eight slides is not a magic number. It is the practical floor for an audience that needs the recommendation, the ask, the case, the alternatives, the risks, the implementation, the controls, and the decision. Each is a separate slide because each is a separate question the CFO has to answer in order to commit. Combine any two and the slide carries more weight than it can render legibly. Skip any one and the conversation in the room stalls on whatever was skipped.

Going beyond eight is the more common error. Twenty-slide decks for budget sign-off are usually three things stacked together: a recommendation deck, a working spreadsheet, and an internal context briefing. The CFO does not want them stacked. The deck loses focus, the discussion fragments, and the recommendation gets buried under the working. The fix is not editing. The fix is moving the working into an appendix or a separate document and letting the eight slides do their job.

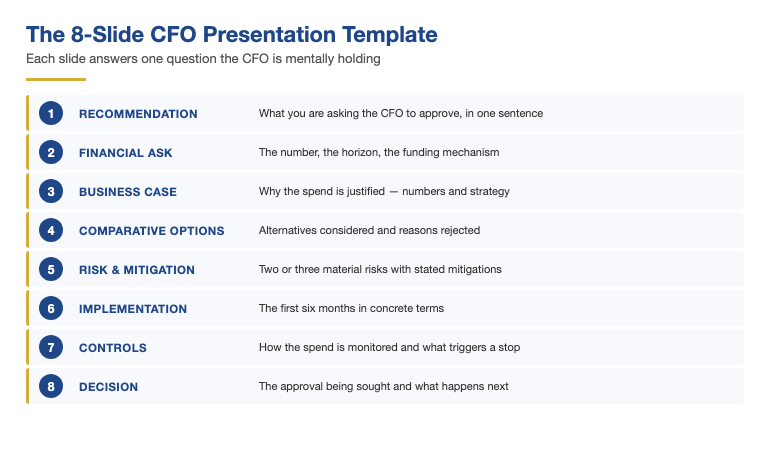

The 8-slide structure, slide by slide

Each slide answers a specific question the CFO is mentally holding. The structure is sequential because the answers depend on each other — the case only makes sense in light of the recommendation, the implementation only matters if the case is sound, and the controls only become relevant once the implementation is credible.

Slide 1 — The recommendation. One sentence. What you are asking the CFO to approve. No build-up, no context, no preamble. The CFO reads the recommendation first, decides what level of scrutiny to apply, and reads the rest of the deck through that lens. A recommendation that hides on slide nine is a recommendation that loses the room before the case appears.

Slide 2 — The financial ask. The number, the time horizon, and the funding mechanism. Capital or operating, single-year or multi-year, internal funding or external, recurring or one-off. The CFO needs the ask in commitment terms before the case is read. A vague ask — “approximately £X over the medium term” — signals that the proposal is not yet sharp enough for sign-off.

Slide 3 — The business case. Why the spend is justified, in numbers and in strategy. Revenue, cost saving, risk reduction, regulatory compliance — whatever the value driver is, name it and quantify it. The case is the substance the CFO will challenge in Q&A. The slide must hold up to challenge in its own right, not lean on the appendix.

Slide 4 — Comparative options. What other ways the same outcome could be reached, and why this is the right one. CFOs ask “why this over X” almost universally. Pre-empting the question on the deck signals that the comparison work has been done. Two or three alternatives, each with a brief reason for non-selection. This is where many sign-offs are won — or refused — for good reason.

Slide 5 — Risk and mitigation. The two or three material risks, each with a stated mitigation. Not a comprehensive risk register. The CFO needs to see that the largest risks have been thought through and have specific responses. A risk slide that lists eighteen risks signals that the proposal owner has not yet decided which risks actually matter.

For senior professionals whose budget sign-off depends on a single deck

The Executive Buy-In Presentation System — build the case the CFO can approve in one meeting

Walk into the budget conversation with the structure that surfaces the answers the CFO needs in the order they need them. The Executive Buy-In Presentation System is a self-paced framework — 7 modules covering stakeholder analysis, case construction, and the slide structures that hold up under finance committee scrutiny. Monthly cohort enrolment.

- 7 self-paced modules covering stakeholder analysis, case construction, and the structures that earn senior approval

- Optional live Q&A / coaching calls — fully recorded, watch back at your own pace

- No deadlines, no mandatory live attendance, lifetime access to materials

- Monthly cohort enrolment — enrol any time, start with the next cohort

£499 · Self-paced · Lifetime access to materials · Next cohort enrolment opens monthly

Slide 6 — Implementation plan. The first six months in concrete terms. Owner, milestones, dependencies, decision points. Implementation is where most cases lose plausibility — the strategy makes sense, the financials make sense, but the path from here to delivery is vague. A specific six-month plan signals that the proposal is execution-ready, not just argumentation-ready.

Slide 7 — Controls and reporting. How the spend will be monitored, what the CFO will see and when, and what triggers a review. This slide is often skipped, and it is the most consequential single slide for a CFO. The case answers “is this worth doing?” — but the controls slide answers “how will I know if this goes wrong?” Without that answer, sign-off is structurally harder. With it, the conversation moves quickly toward yes.

Slide 8 — The decision. What you are asking the CFO to approve, by when, and what will move forward immediately on approval. The decision slide is not a redundancy with slide one — it is the conversation closer. Slide one says “here is what I am asking”. Slide eight says “here is what happens when you say yes, and here is what I need from you next”. Many decks lose the close by ending on a question slide instead of a decision slide.

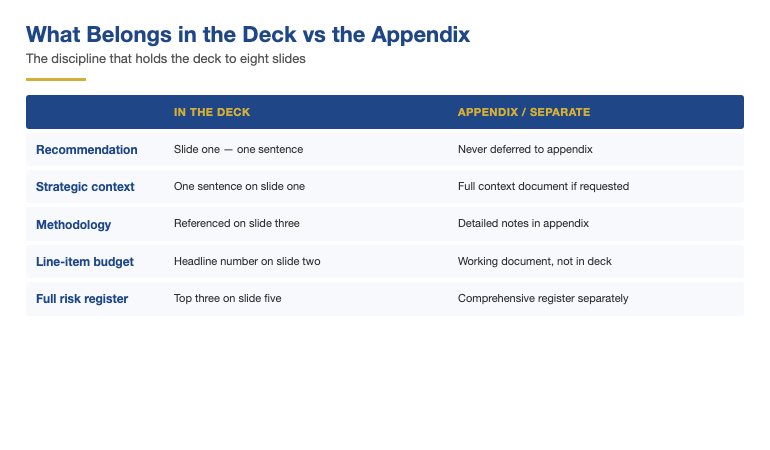

What stays out of the deck (and why)

A CFO deck that goes beyond eight slides is usually carrying material that does not belong on the front. The discipline of an 8-slide structure forces a series of decisions about what the CFO needs to see in the conversation versus what they can read separately if they want to. Most often, the cut goes to one of four places.

Strategic context. The “why this matters” framing belongs on the recommendation slide as a single sentence — not on a dedicated context slide that delays the ask by two minutes. CFOs who need more context will ask. Most do not. A context slide is rarely the difference between a yes and a no, but it routinely costs minutes that the case slides need.

Methodology notes. The methodology behind the financial model is appendix material. Reference it on the business case slide (“based on bottom-up analysis, validated against benchmark X”) but do not walk the room through it. CFOs assume methodology has been done. They will challenge specific outputs, not the method.

Line-item budget. Detailed budget breakdown belongs in a separate working document, not in the deck. The CFO needs the headline number on slide two and confidence that the working stands behind it. The line items are for the conversation that happens after sign-off, not for the conversation that produces sign-off.

For deeper structural alignment between deck and audience, the related discussion of budget presentation templates a CFO will actually approve covers the variations by sector and by case size.

Companion templates for the 8-slide CFO format

The Executive Slide System — board-ready slide templates for the 8-slide structure

Once the structure is fixed, the slides themselves still need to render the case cleanly. The Executive Slide System covers 26 templates, 93 AI prompts, and 16 scenario playbooks — including recommendation slides, comparative options layouts, and risk-mitigation structures designed for finance audiences. £39, instant download. Explore the slide system →

Assembling the deck in the right order

Most teams build CFO decks in slide-one-to-slide-eight order, which is the wrong order. The order the audience reads is not the order the deck is built in. Senior presenters tend to assemble from the inside out — the case first, then the controls, then the recommendation, then the close.

Build the case before the recommendation. A recommendation that has not been derived from a case is a recommendation that does not survive Q&A. Write slide three first — the business case in its strongest form, with the actual numbers and the actual evidence. The recommendation on slide one is then a one-sentence summary of slide three, not an instinct that needs to be defended.

Build the controls before the implementation. The CFO will accept an implementation plan that has minor weaknesses if the controls are strong. The reverse is rarely true. Strong controls are what makes a CFO comfortable with operational uncertainty. Build slide seven before slide six — what the CFO will see and when — and the implementation plan will be sharper for it.

Pre-empt the comparative question. Slide four exists because the question is going to come whether or not the slide is in the deck. Building the comparative slide forces a confrontation with the alternatives — and that confrontation usually sharpens the case. Many proposals strengthen materially when the team is forced to write down why each alternative was rejected.

Close on the decision, not on a question. Many decks end on “Questions?” or “Discussion” or a thank-you slide. None of those close the meeting. A decision slide — what is being approved, what happens on Monday morning, what is needed from the CFO — closes the meeting in a way the room can act on. The decision slide is the difference between sign-off in the meeting and sign-off in a follow-up email that may or may not arrive.

Five mistakes that lose CFO sign-off

Mistake one — burying the recommendation. The most common error. The deck builds for nine slides, the recommendation appears on slide ten, and the CFO has read the room as “they are not yet ready to commit”. By the time the recommendation appears, the meeting has already drifted toward “let’s revisit next quarter”.

Mistake two — vague financial ask. “Investment of approximately £X over the medium term, subject to refinement”. CFOs read this as a proposal that is not yet ready for sign-off. The fix is to commit to a specific number, a specific horizon, and a specific funding mechanism. If those are still uncertain, the meeting is not the right meeting.

Mistake three — no comparative slide. Without slide four, the question “why this over X” is asked in Q&A and the presenter is improvising. The improvisation rarely lands as well as a prepared answer. Pre-empt the comparison and the conversation moves on. Skip it and the meeting often ends on the comparative question rather than on the decision.

Mistake four — risk slide as a register. A risk slide that lists fifteen risks signals that the team has not yet decided which risks matter. CFOs want to see the two or three material risks named, with mitigations attached. Comprehensive risk registers belong in the appendix or in a separate document. The deck’s job is to surface what could break the case, not to prove that all possible risks have been catalogued.

Mistake five — closing on a thank-you slide. The deck ends on “Thank you” or “Questions?” and the CFO closes the meeting with “let me think about it”. The decision slide closes the meeting actively — names the approval being sought, names the timing, names the next action. A meeting that closes on a decision slide produces sign-off about three times more often than a meeting that closes on a question slide.

Frequently asked questions

Can the 8-slide structure be used for a finance committee, not just a single CFO?

Yes. The structure works for any audience that needs to commit to a financial decision. Finance committees, investment committees, and audit committees all read decks the same way: recommendation first, evidence second, controls third. The only adjustment is around stakeholder dynamics — when the room is multiple people rather than one CFO, slide four (comparative options) and slide five (risk) carry more weight, because different members of the committee will challenge different aspects of the case.

What if the proposal needs more than eight slides to be properly explained?

Then the deck and the appendix should be separated. The deck stays at eight slides — the structural minimum for a budget sign-off conversation — and the appendix carries the supporting detail the CFO can request if needed. The discipline of holding to eight forces clarity about what the deck has to do versus what can be made available on demand. Most cases that feel like they need fifteen slides actually need eight clean slides plus a strong appendix.

How long should each slide take to present?

Plan three to four minutes per slide for an audience that will engage. That is roughly twenty-five to thirty minutes for the deck itself, leaving time for Q&A and decision discussion within a typical hour-long slot. Slides one and eight should take less time — they are summary slides. Slides three, six, and seven typically take more, because they hold more substantive content. Time per slide is a working estimate, not a rule.

Should the deck be sent in advance or presented live?

Both. Send the deck twenty-four to forty-eight hours in advance to allow the CFO and the committee to read it before the meeting. Then walk through it live, more briefly than if it were the first reading. Pre-read drives a substantially higher sign-off rate because the meeting becomes a conversation about specific concerns rather than a first encounter with the case. The 8-slide structure is designed to read well both ways — short enough to be readable in advance, structured enough to be presented live.

Maven cohort enrolment — open this month

The system senior leaders use to secure board and CFO sign-off — without going to twenty slides

The Executive Buy-In Presentation System covers the case construction, stakeholder dynamics, and slide structures that produce sign-off from finance committees and CFOs. 7 self-paced modules. Monthly cohort enrolment.

£499 · Self-paced · Lifetime access · Optional recorded Q&A calls

The Winning Edge — weekly

One short note each Thursday on board-level presentation patterns, structural shortcuts, and the behaviours senior presenters use under scrutiny. Written for professionals who do not have time for newsletters that read like newsletters.

Want a structural starting point first? The free Executive Presentation Checklist covers the structural fundamentals senior presenters use before designing the deck.

For the broader pattern of presenting financial proposals to senior decision-makers, see the related piece on how to present to a CFO — the audience considerations the 8-slide structure is designed to serve.

Next step: Pick the next budget proposal you are working on. Build slide three first — the business case in its strongest form. Then build slide seven — the controls. Then write slide one as a one-sentence summary of three. The rest of the deck assembles around those anchors. The deck you build that way will read like a deck designed for the CFO, not a deck the CFO has to translate.

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises senior professionals across financial services, healthcare, technology, and government on structuring presentations for high-stakes board meetings, investment committees, and executive sessions. She speaks German and works extensively with the German-speaking financial markets.