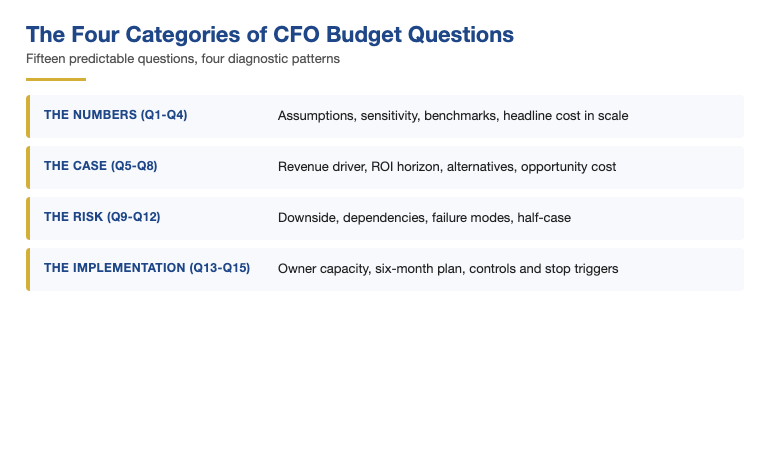

Quick answer: CFOs ask the same fifteen questions in budget presentations. They cluster into four categories: the numbers (assumptions, sensitivity, comparable benchmarks, headline cost), the case (revenue, ROI, alternatives, opportunity cost), the risk (downside, dependencies, what triggers a stop), and the implementation (owner, timeline, controls, exit). The questions are predictable. The answers are not. A prepared answer pattern moves the meeting toward sign-off. An improvised one signals that the proposal has not been stress-tested.

Jump to:

Toby had answered the financial questions for thirty minutes. Sensitivity, scenario, NPV, payback, comparable benchmarks. He had answered each one cleanly. Then the CFO asked the question that ended the meeting: “If this delivers half what you are projecting, what happens?” Toby did not have an answer. Not because the answer was unknown, but because he had never been asked the question in that form. He had prepared for the upside. He had not prepared for the half-case.

CFO budget questions follow a pattern. They cluster into four categories, and within each category the same five or six questions appear in different forms. A senior leader who has prepared for the categories — not just for the specific phrasing — handles the meeting calmly. The questions stop being a stress test and start being a conversation about the case. A senior leader who has prepared only for the obvious questions runs into the same wall Toby did.

The fifteen questions below are the working set most senior presenters need to be able to answer in a budget conversation. Not memorised answers — pattern answers. Each one has a structural response that holds up under follow-up, signals that the proposal has been thought through, and moves the discussion toward the sign-off rather than away from it.

If your last CFO Q&A surfaced a question you had not prepared for

The Executive Q&A Handling System covers the answer structures senior presenters use under finance committee pressure. Decision-safe answers under sharp questioning, the patterns that stop a hostile follow-up, and the recovery technique when an answer has not landed. Instant download.

Why CFO questions follow a pattern

CFOs ask the same questions because the questions reflect the structural job of the role. A CFO is responsible for protecting the financial integrity of the organisation against decisions that look attractive on the front page of the deck but break under stress. The questions are diagnostics. They surface whether the proposal owner has thought through what the deck does not show.

Within most budget conversations, the question pattern is consistent. The first questions test the numbers — are the underlying assumptions defensible. The next questions test the case — does the proposal earn the spend. Then come the risk questions — what could go wrong and what protects against it. Finally come the implementation questions — who is doing the work and how the CFO will know it is going to plan.

The presenter who has prepared by category rather than by specific question handles unfamiliar phrasing without losing composure. A new question is rarely actually new — it is usually a familiar question dressed differently. Recognising the category lets the presenter route the answer through a prepared structure rather than improvising a fresh one. Improvised answers under finance pressure tend to overshoot, undershoot, or invent commitments. Structured answers do not.

Category one: The numbers (Q1–Q4)

Q1 — “What are the three biggest assumptions in this number?” Pattern: name three specific assumptions, the basis for each, and which one is the most sensitive. Not five, not nine — three. CFOs are testing whether the proposal owner has interrogated their own model. A diffuse answer signals the model has not been pressure-tested.

Q2 — “What does the sensitivity look like if assumption X moves by 20%?” Pattern: state the impact on the headline outcome, name the threshold at which the case stops working, and identify what would have to be done in response. Sensitivity questions test how cleanly the model has been built and whether the owner can speak to it without referring to a spreadsheet.

Q3 — “What is this benchmarked against?” Pattern: name the comparable, name the source, name the limitation. CFOs do not expect perfect benchmarks — they expect the presenter to know which comparable was used and why, and where it does not apply. An answer that names the comparable and acknowledges its limits scores higher than one that claims a perfect benchmark.

Q4 — “What is the headline cost in plain terms?” Pattern: total cost over the funding horizon, expressed both in absolute terms and as a percentage of an obvious denominator (annual operating budget, capital programme size, divisional P&L). CFOs need the cost in scale terms quickly. A multi-clause answer signals the presenter has not yet thought about how the spend looks at the level the CFO is sitting at.

Category two: The case (Q5–Q8)

Q5 — “What is the revenue or value driver, and how confident are you in it?” Pattern: name the driver, state the confidence band, name what would increase the confidence over the next quarter. Revenue questions are tests of how grounded the case is in operational reality. Confidence bands without a path to tightening them sound speculative.

Q6 — “What is the ROI, and over what horizon?” Pattern: state the ROI, state the horizon, state the year of breakeven. CFOs read ROI in time-to-payback terms more than as a single percentage. An ROI that does not specify the horizon is read as a number searching for an interpretation.

Q7 — “Why this and not the alternatives?” Pattern: name two or three alternatives explicitly, state the criterion that distinguishes this proposal from each, and anchor that criterion to a strategic priority the room has already endorsed. Comparative questions are about whether the comparison work has been done. A vague answer here loses sign-off more often than any other single response.

Q8 — “What is the opportunity cost of saying yes?” Pattern: name what the same capital would otherwise fund, state why this is the higher priority, acknowledge what is being deferred. Opportunity cost questions test whether the presenter sees the proposal in portfolio terms. CFOs sit on the portfolio. Presenters who answer in portfolio terms speak the CFO’s language.

For senior professionals presenting financial proposals under sharp scrutiny

The Executive Q&A Handling System — answer the hard finance questions calmly

Stop losing control in Q&A. The Executive Q&A Handling System gives you decision-safe answer patterns for tough questions in 45 seconds — designed for senior presenters facing CFO and finance committee scrutiny. Includes the structures behind every answer pattern in this article. Instant download.

- Decision-safe answer patterns for the hardest finance questions

- The 45-second answer structure senior presenters use under pressure

- Recovery techniques for when an answer has not landed

- Pattern library for hostile, comparative, and trap questions

£39 · Instant download · Lifetime access · 30-day refund if it doesn’t fit your next presentation

Category three: The risk (Q9–Q12)

Q9 — “What is the downside case?” Pattern: state the downside outcome explicitly, state what triggers the downside, state what the proposal still delivers in that case. CFOs accept downside cases that are honest. They reject downside cases that are minimised. The right answer names the worse outcome and shows that the proposal still earns its place in the portfolio under that scenario.

Q10 — “What dependencies are outside your control?” Pattern: list two or three external dependencies, name the most consequential, name what compensating control sits behind it. CFOs are wary of proposals that ignore external dependencies. They are reassured by proposals that name the dependencies and have thought about what happens if they do not hold.

Q11 — “What would have to be true for this to fail?” Pattern: name the two or three conditions that would cause material failure, state which is most likely, state the early warning that would surface it. This is the question that separates rehearsed answers from prepared ones. The presenter who can describe the failure mode without flinching gains credibility. The presenter who cannot describe it loses the room.

Q12 — “If this delivers half what you are projecting, what happens?” Pattern: state the half-case outcome, state whether the proposal still meets its strategic objective, state what would change in the implementation under the half-case. The half-case question is one of the most predictive questions a CFO can ask. A proposal that cannot survive a half-case is a proposal that is over-engineered for the upside.

Category four: The implementation (Q13–Q15)

Q13 — “Who is going to lead this, and what else are they responsible for?” Pattern: name the owner, name their current portfolio, name what is being deprioritised to make room. CFOs ask leadership questions because they have seen many cases die on capacity rather than on capability. An owner with a packed portfolio is a risk indicator. An owner with explicit deprioritisation is a credibility signal.

Q14 — “What does the first six months look like, in concrete terms?” Pattern: name the milestones, name the decision points, name the spend profile in the first six months. CFOs are sceptical of cases where the first six months are vague. The deck and the answers should be most precise about the period nearest to sign-off — that is the period the CFO can hold the team to.

Q15 — “How will I know if this is working, and what triggers a stop?” Pattern: name the leading indicator, name the lagging indicator, name the threshold at which a formal review or stop would be triggered. Q15 is the controls question, and it is the single highest-leverage answer in the meeting. A presenter who can answer it cleanly removes most of the residual concern in the room. A presenter who cannot answer it cleanly often does not get sign-off in the meeting.

Preparing the answers in advance

The fifteen questions are predictable, which means the answers are preparable. Senior presenters who walk into a CFO meeting with prepared answers — written down, spoken aloud once or twice, structured in three or four sentences — handle the actual meeting with substantially more composure than presenters who rely on the deck and improvise the rest.

A working preparation routine is to write a one-paragraph answer to each of the fifteen questions, in advance, on a single page. The page is not for the meeting. The page is for the rehearsal. The act of writing the answer surfaces the gaps that improvisation would not. By the time the meeting happens, the answers are not memorised — they are familiar. Familiar answers under pressure are calm answers.

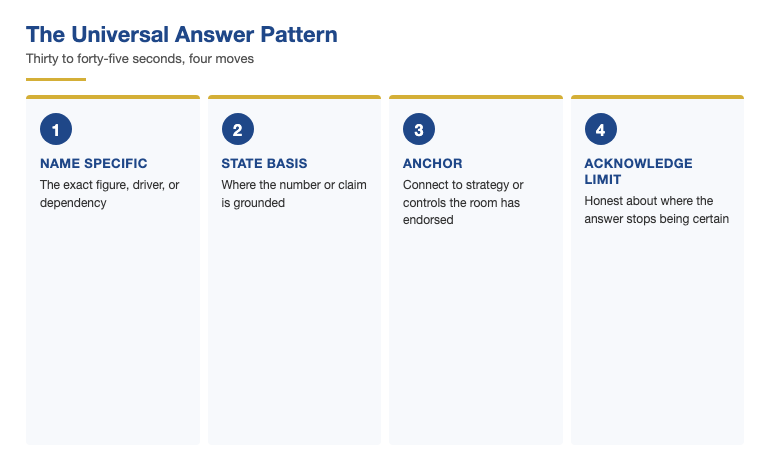

The answer pattern is the same across categories: name the specific, state the basis, anchor to strategy or controls, acknowledge the limit honestly. Within thirty to forty seconds, the answer has given the CFO what they need to commit, conceded what cannot be promised, and signalled that the case has been pressure-tested. CFOs sign off on cases that have been tested. They defer cases that have not.

For the broader pattern of presenting financial proposals at senior level, see the related discussion of why-believe-your-numbers as the most consequential single question — the test that sits behind every other CFO question.

Slide structures behind the answers

The Executive Slide System — finance-ready slide templates that anticipate the CFO questions

The strongest answers are the ones that the deck has already pre-empted. The Executive Slide System covers 26 templates and 16 scenario playbooks — including the comparative options slide, the risk-mitigation structure, and the controls slide that pre-empt eleven of the fifteen CFO questions. £39, instant download. Explore the slide system →

Frequently asked questions

What if the CFO asks a question that does not fit one of the fifteen?

Most off-pattern questions are still in-pattern in disguise. A “what does this mean for the team?” question is usually an implementation question (Q13). A “what does the chair think?” question is usually a stakeholder question that maps to the case category. The first move under an unexpected question is to identify which category it belongs to, then route the answer through that category’s pattern. True off-pattern questions are rare, and they usually call for a calm acknowledgement and an offer to follow up with a fuller answer rather than improvisation.

Should I prepare written answers or just bullet points?

Write paragraphs first, then compress to bullets. Writing the full paragraph is what surfaces the gaps. Compressing to bullets is what makes the answer deliverable in the meeting. Senior presenters who skip the paragraph stage tend to discover gaps in the actual meeting. Presenters who write the paragraph but bring only the bullets to the meeting tend to handle the questions more calmly. The compression is not optional. The writing is.

How long should each answer take?

Plan thirty to forty-five seconds for most answers. Longer than a minute and the answer starts to read as defensive. Shorter than twenty seconds and it reads as evasive. The answer pattern — name the specific, state the basis, anchor, acknowledge the limit — fits comfortably into thirty to forty-five seconds when written down. Practice it in a calendar slot before the meeting if possible. The answer that lands in the meeting is the answer that has been said aloud at least once before.

What if I genuinely do not know the answer?

Then say so directly, name what you would need to know to answer well, and commit to a follow-up by a specific time. CFOs respect “I don’t have that figure with me — I will send it by close of business” far more than a fabricated estimate. The risk is not in not knowing. The risk is in pretending. A composed admission combined with a precise follow-up commitment usually leaves the room with no damage. A guess that turns out wrong damages the relationship for years.

For senior presenters who get questioned by finance committees

Walk into the next CFO meeting with prepared answers, not improvisation

The Executive Q&A Handling System covers the answer patterns senior presenters use under finance committee pressure — including the structures behind every category in this article. £39, instant download.

£39 · Instant download · Lifetime access

The Winning Edge — weekly

One short note each Thursday on board-level presentation patterns, structural shortcuts, and the behaviours senior presenters use under scrutiny. Written for professionals who do not have time for newsletters that read like newsletters.

Want a structural starting point? The free Executive Presentation Checklist covers the structural fundamentals senior presenters use before designing the deck.

For the audience considerations behind the question patterns, see the related piece on the CFO presentation checklist — what to verify in the deck before the questions begin.

Next step: Take the next budget proposal you are working on. Write a one-paragraph answer to each of the fifteen questions on a single page. Read each answer aloud once. The gaps you find in the writing are the gaps the CFO would have surfaced in the meeting. Close them on paper now, and the meeting becomes a conversation about the case rather than a stress test on the model.

Mary Beth Hazeldine is the Owner & Managing Director of Winning Presentations. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises senior professionals across financial services, healthcare, technology, and government on structuring presentations for high-stakes board meetings, investment committees, and executive sessions. She speaks German and works extensively with the German-speaking financial markets.