The Finance Deck CFOs Read First: Which 3 Slides Determine Whether the Rest Gets Attention

Quick answer: CFOs reviewing a finance deck before a meeting almost always read three slides before deciding whether the rest of the deck deserves attention. The first is the executive summary slide — they want to know whether the deck has been framed as a decision aid or as a working paper. The second is the variance or movement slide — they want to see whether the change has been named cleanly or hidden in a category breakdown. The third is the assumptions slide — they want to test whether the numbers rest on plausible inputs. If those three slides pass, the rest of the deck gets a fair reading. If any of the three fails, the CFO either skims the rest or sends the deck back for rework. The discipline is to write the three slides as if they were the entire deck.

JUMP TO:

Astrid, an FP&A director at a mid-size insurance firm in Zurich, sent her quarterly finance deck to the new group CFO three days before the review meeting. The deck was 31 slides and had been used at the previous quarter’s review with the outgoing CFO without comment. The new CFO scheduled a 15-minute slot rather than the standard 45 and opened the meeting with a single sentence: “I read your first three slides. Walk me through whether the variance on slide two is a one-off or a structural shift, then we can talk about the rest.” Astrid had not made the variance the focus of slide two. She had used slide two for an organisational overview. The next 15 minutes were spent recovering ground that should have been on the slide; the broader strategic discussion she had planned never happened.

The diagnosis was structural. The new CFO read decks the way most CFOs in 2026 read decks — first three slides, then a decision about whether to read the rest. The previous CFO had read every page; the new one did not. The deck that worked at 45 minutes with a slide-by-slide reader did not survive a 15-minute window with a triage reader. The same content, in the same order, produced two completely different meetings — and only the second was the one that mattered for the next year.

This piece walks through the three slides CFOs read first when triaging a finance deck — what each slide has to carry, the structural test each one has to pass, and the discipline that separates decks that earn the rest of the meeting from decks that get sent back. The principles apply to quarterly reviews, budget reviews, capital expenditure submissions, and any other finance presentation where a CFO will see the deck before the meeting. The shape of the deck is the same; the rigour of the first three slides decides what gets read after.

Want a one-page reference of the questions a CFO will ask after reading your first three slides?

The 10 Questions Every CFO Asks (+ Scripts) is a free one-page cheatsheet of the questions finance leaders most often ask in deck reviews — and the answer structure that survives each one. Free download.

How CFOs actually read a finance deck

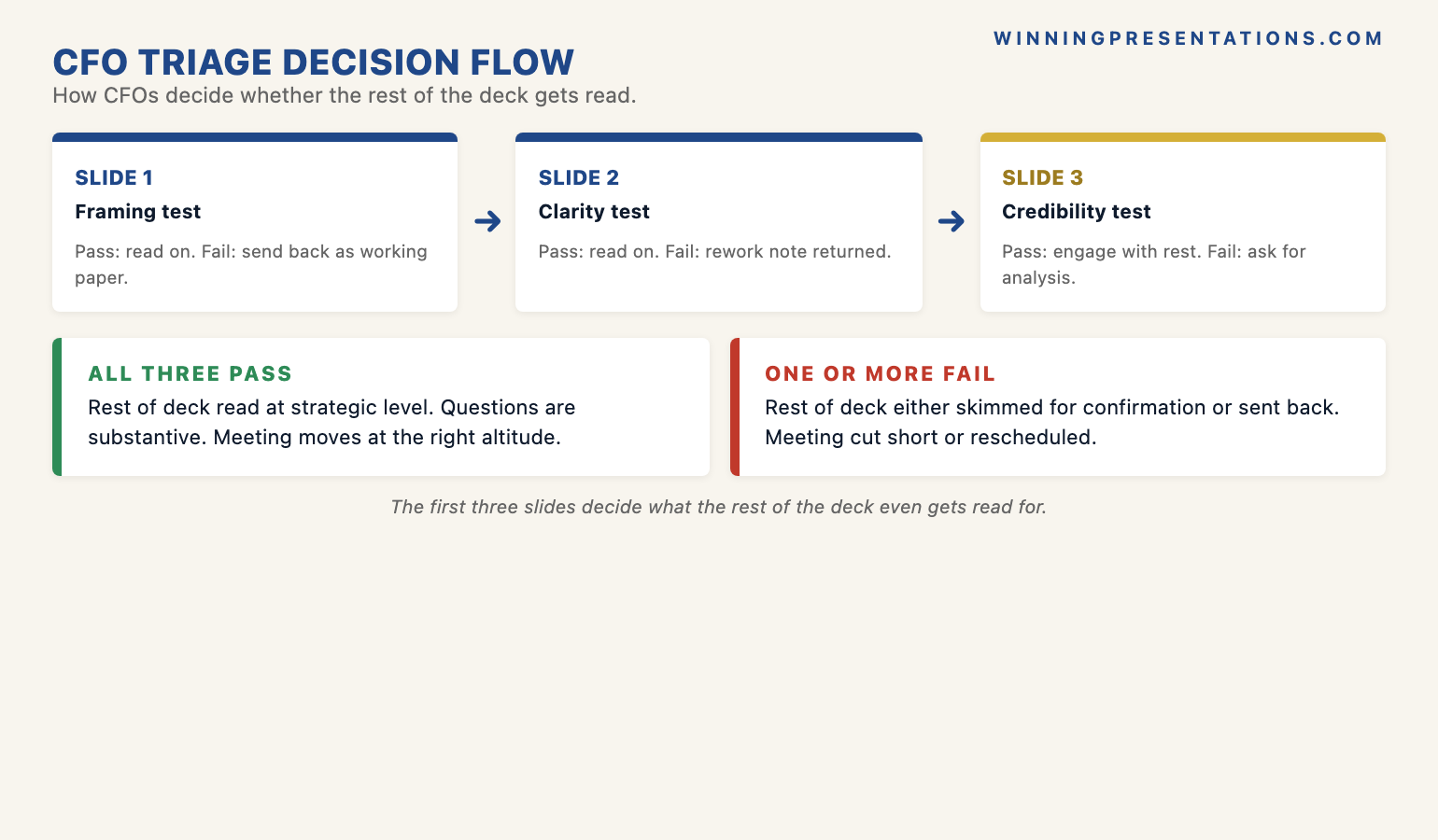

CFOs in 2026 do not read finance decks linearly. They triage. The first three slides decide whether the deck is a decision aid worth engaging with or a working paper that needs to be sent back. A CFO who has eight decks in their inbox before Friday’s meeting cannot read every page of every deck; they read the first three slides of each, form a judgement about how the deck is framed, and then either engage with the substance or skim and send back. The triage is not lazy reading. It is informed sampling — the first three slides correlate strongly with the rigour of the rest of the deck, because authors who frame the first three slides cleanly almost always carry the discipline through.

The triage is a specific shift from a decade ago, when CFOs of mid-cap firms typically had time to read every page of every deck and discuss it slide by slide in the review meeting. Two changes have driven the shift. First, the volume of submissions has grown — finance functions have moved from quarterly to monthly and in some cases continuous reporting cycles, and the CFO’s review queue has grown with it. Second, the analytical work has moved upstream — much of the line-item analysis is now done in the model rather than on the slide, so the slide is expected to summarise rather than walk through. The CFO who reads the first three slides and decides is responding to both changes simultaneously.

The implication for the presenter is that the first three slides have to carry disproportionate weight. Not because they are more important than the analysis underneath; they are the same importance. But because they are the slides that decide whether the analysis underneath gets read at all. A presenter who treats the first three slides as warmup — agenda, context, organisation chart — has effectively decided to lose the meeting before the substantive slides are reached. The deck that lands has its three best slides at the front, in the order the CFO will read them. For the structural discipline behind a finance deck that anticipates this triage, see our CFO presentation checklist piece.

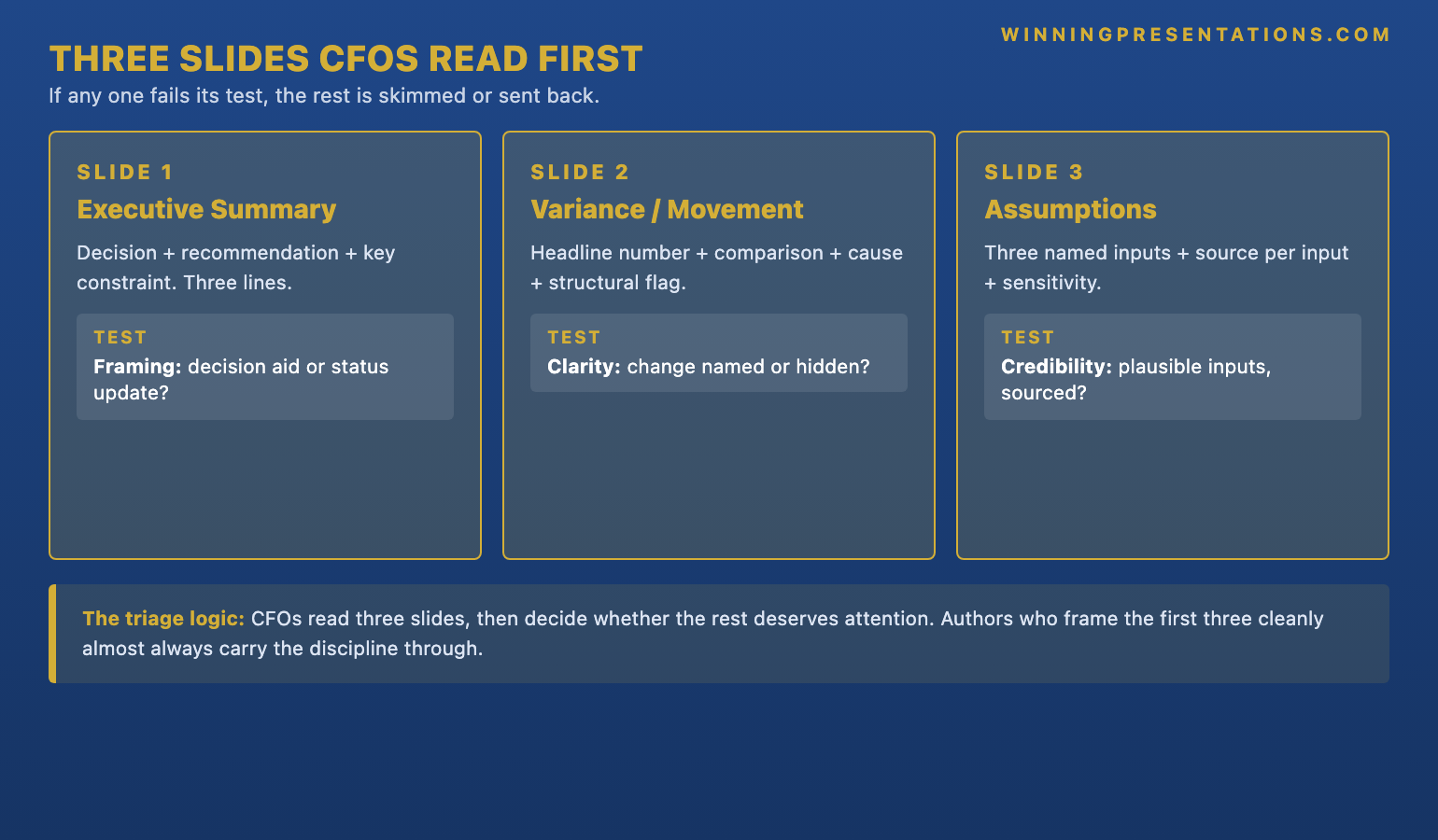

The executive summary slide: the framing test

The first slide a CFO reads is the executive summary slide, and the test it has to pass is the framing test. A CFO reading the executive summary is asking one question: has this deck been framed as a decision aid or as a status update? The answer is visible in the structure of the slide. A decision-aid summary names the decision the deck supports, the recommendation being made, and the key number the recommendation rests on. A status-update summary names the period covered, the team that produced the analysis, and a list of topics. The first reads as a board paper; the second reads as a working report.

The format that works has three lines. Line one names the decision: “Approval of Q2 capital expenditure plan, £4.2m, 12-month horizon.” Line two names the recommendation: “Recommend approval at the requested level, with monthly reporting against the milestone schedule on slide eight.” Line three names the key constraint or assumption: “Recommendation rests on the foreign exchange assumption set out on slide four; sensitivity to a 5 per cent shift is £180,000.” That is the slide. No table, no logo block taking up the top quarter, no agenda preview. The CFO who reads those three lines knows what the deck is asking for, what it recommends, and where the assumption risk sits.

The slide is not a marketing summary. It is an analytical summary in the form a CFO can act on. The discipline is to write it last, not first — the executive summary is the synthesis of the analysis underneath, and it cannot be drafted credibly until that analysis is complete. Authors who write the executive summary first tend to use it for framing language that does not survive contact with the numbers; authors who write it last tend to use it as the precise statement the rest of the deck supports. The order of writing is the inverse of the order of reading, and that inversion is the discipline.

The variance slide: the clarity test

The second slide a CFO reads is the variance or movement slide, and the test is the clarity test. A CFO is asking: has the change been named cleanly or hidden in a breakdown? The slide that passes the test names the variance in a single number at the top, with the period it covers, and a one-line statement of the cause. A weak variance slide buries the change inside a category-by-category table; a strong variance slide names the change in plain text and lets the supporting breakdown sit in the appendix.

The format that works has four elements. The headline number — the variance, expressed as both an absolute amount and a percentage. The comparison — what the period is being compared to (prior year actual, prior year budget, current year forecast). The cause — one sentence naming the dominant driver, in plain language. The flag — a single line saying whether the variance is structural (continues into next period) or one-off (does not continue). Those four elements take the top half of the slide. The bottom half can carry a small supporting chart if needed, but the chart is optional; the four elements are mandatory.

The discipline is in choosing the cause sentence. Most variances have multiple drivers, and the temptation is to name them all. The slide that works names the dominant driver — the one that explains the largest single share of the movement — and lets the rest sit in the supporting analysis. A CFO can hold one cause in their head while reading the rest of the deck; a CFO presented with five causes on the slide tends to ask which one matters most, which is the question the slide should have answered already. The strongest cause sentence is also specific: not “operational changes” but “completion of the Munich integration ahead of schedule, which lowered transition spend by £340,000”. For the deeper discipline behind drafting variance language a CFO will accept, see our how to present to a CFO piece.

Build the first three slides every CFO reads first — on a structured slide system rather than from scratch.

The Executive Slide System is a structured library of templates, AI prompts, and scenario playbooks for senior-level slide work — including the executive-summary, variance, and assumption-set slide structures CFOs read first in a finance deck. Designed for finance leaders, FP&A directors, and senior professionals who present to a CFO routinely.

- 26 Executive Templates — including the three CFO-first slide structures used in this article

- 93 AI Prompts for drafting decision-aid summaries, variance language, and assumption framing

- 16 Scenario Playbooks — CFO review, audit committee, board finance committee, exec sponsor

- 7 Checklists — the pre-meeting structural review CFOs use themselves

- £39, instant download, lifetime updates

The assumptions slide: the credibility test

The third slide a CFO reads is the assumptions slide, and the test is the credibility test. A CFO is asking: do the numbers rest on plausible inputs, named explicitly, with the source visible? The slide that passes names three assumptions, in plain language, each with the input value, the source, and the sensitivity if the assumption proves wrong. Three is the right number — five reads as defensive, ten reads as obfuscation, and two reads as having missed something. Three is what a finance committee can hold in mind during the rest of the meeting.

The choice of which three is where the analytical work sits. The assumptions that belong on the slide are the ones whose failure would change the deck materially. A volume assumption that affects 3 per cent of the total is not a top-three assumption; an FX assumption that drives a £400,000 swing on a £4.2m request is. A revenue mix assumption that changes the gross margin number visibly is. An interest rate assumption that affects the financing cost of a multi-year capex programme is. The selection is not arbitrary — it is the answer to the question: if I am wrong about the budget, which three things am I most likely to be wrong about?

The slide is also where the source matters. Naming an assumption without a source reduces it to an opinion; naming the source converts it to an analytical position. “FX assumption: 1.16 EUR/GBP, source: group treasury 12-month forward curve” reads as an analytically grounded number; “FX assumption: 1.16 EUR/GBP” alone reads as a guess. The source line is short, but its presence shifts how the CFO reads the rest of the deck. Decks that include the source line on every assumption tend to get engaged readings; decks that do not tend to get follow-up emails asking where the numbers came from. The follow-up email is a sign the slide has not done its job.

What the rest of the deck does once the three slides pass

Once the first three slides pass the CFO’s triage, the rest of the deck functions as the analytical evidence base. The remaining slides — typically eight to twelve — answer the questions the first three slides have raised. The drivers of the variance get a slide. The capital structure or cash flow implications get a slide. The risks and mitigations get a slide. The milestone schedule or implementation timeline gets a slide. The request itself gets a slide, even though it has already been named in the executive summary, because the request slide is what the chair calls a vote on. None of these slides earns the right to be read unless the first three have done their work first.

The asymmetry is significant. A deck whose first three slides pass the triage tests gets the rest of its slides read with the assumption that the analysis is sound; questions tend to be substantive and constructive. A deck whose first three slides fail tends to get the rest of its slides read with suspicion, if at all; questions tend to be probing and defensive. The same analytical work, presented behind two different sets of opening slides, produces two entirely different review meetings. The disproportion is not fair to the work, but it is consistent and predictable, which means it can be planned for.

If the CFO’s questions on the first three slides are what derail the meeting, prepare for them deliberately:

The Executive Q&A Handling System is a structured framework for the high-stakes Q&A that follows a finance deck — handling tough questions on variances, assumptions, and capital structure with calm authority and decision-safe answers. £39, instant download.

The implication for how the deck is built is to invert the usual order. Most decks are built front-to-back: cover, agenda, context, then the analysis. The deck that survives CFO triage is built back-to-front: the analysis is completed first; the executive summary is written from the analysis as a synthesis; the variance and assumption slides are then drafted as the second and third reads of that synthesis. The cover and agenda slides — if they exist at all — are added last and trimmed aggressively. Authors who build front-to-back tend to use the first three slides as warmup; authors who build back-to-front tend to use the first three slides as the synthesis. The build order is the discipline. For more on the structural discipline behind a board-ready budget request that anticipates the same triage, see our companion article on the board budget presentation 6-slide format.

Frequently asked questions

Should the executive summary slide go before or after the agenda slide?

Before. In most finance decks the agenda slide adds little value — the deck order is implicit in the structure and the section headers do the same job inside the deck. The agenda slide takes up the position the executive summary should occupy as the first read, which is a structural waste. A finance deck that opens with the executive summary signals immediately that the deck is a decision aid; one that opens with an agenda signals that the deck is a working paper. If an agenda slide is required by house style, it can sit on slide two or move into the appendix; the executive summary should always be slide one.

How long should the variance slide be?

One slide. Multi-slide variance analyses belong in the appendix. The on-deck variance slide names the headline number, the comparison basis, the dominant cause, and the structural flag — that is enough for the CFO to understand the shape of the change. If a multi-slide variance breakdown is genuinely needed for the substance of the meeting, the deck has misjudged the audience: that level of detail belongs in the supporting board paper or in the analytical model, not in the live deck. Keeping the variance to one clean slide is not under-presenting; it is matching the slide format to the way the slide will actually be read.

Do CFOs really skip the rest of the deck if the first three slides fail?

Most do, in some form. The triage is rarely literal — a CFO will not visibly stop reading at slide three — but the engagement they bring to the rest of the deck shifts materially based on what the first three slides showed. A deck whose opening slides passed the triage gets read with constructive scepticism; a deck whose opening slides failed gets read for confirmation that it should be sent back. The presenter typically experiences the difference as the depth of the questions in the meeting. Substantive questions on assumptions, sensitivities, and timing signal the deck passed; surface questions about formatting, dates, and definitions signal it did not.

What if the deck is being seen by the full board, not just the CFO?

The CFO is still the first reader. In most boards, the CFO reviews the finance deck before the meeting and either signals approval to the chair or flags concerns. That review happens against the same triage tests described above. The full-board reading happens later and at a higher level — boards rely on the CFO’s signal to weigh how much scrutiny to apply themselves. A deck that has passed the CFO’s triage tends to get a constructive board reception even if the chair has not personally read every page; a deck that has failed it tends to get probing questions even from non-finance directors who have picked up the chair’s caution.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate decks committees back from decks they defer. Subscribe to The Winning Edge →

Not ready for the full Executive Slide System? Start here instead: download the free 10 Questions Every CFO Asks (+ Scripts) — a one-page reference of the questions every CFO will probe in a finance deck review, with the answer structure that holds up.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 25 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.