Quick answer: The honest answer to “how did you arrive at that valuation?” is a three-part structure that names the market-comparable benchmark, the company-specific premium or discount to that benchmark, and the round-mechanics reason the number landed where it did. The answer does not start with a discounted cash flow model and it does not start with a defence of the number. It starts with the comparable: “The series-A round in our sector is currently pricing between six and nine times forward revenue. We are pricing at seven and a half times, which is the median for our sub-segment.” Then the company-specific premium: “We are slightly above the median because the net revenue retention is one hundred and twenty-two percent and the gross margin is sixty-three percent — both above the segment average.” Then the round-mechanics: “The lead-investor process produced a term sheet at this level, and the existing investors have all signed on at the same price.” The structure is honest because it names what the partner already knows, names what the company adds to it, and names the process that closed the price. The instinct to defend the number is the instinct that loses the round.

JUMP TO:

- Why the question is asked, and what the partner is testing

- Four wrong answers and why each one loses the round

- The three-part honest answer, in order

- The follow-up questions to expect, and how to answer each

- When the partner thinks the valuation is too high

- Preparation: the homework that has to happen before the pitch

- Frequently asked questions

Kenji, a founder of a Tokyo-headquartered enterprise-AI company, was pitching a New York growth fund’s investment committee for a series-B round at a sixty-five million dollar pre-money valuation. Thirty-two minutes into the meeting, the lead partner — a senior partner who had led the fund’s three previous AI investments — asked the question every founder dreads: “How did you arrive at that valuation?” Kenji had prepared for the question. He had a twelve-slide appendix on the discounted cash flow model behind the number, a peer-comparable analysis using ten public-market and private-market comparables, and a memorised three-paragraph justification of the premium to the comparables. He started with the discounted cash flow model. The partner interrupted at the second slide of the appendix: “Stop. I am not asking for the model. I am asking you what you actually think the number means.”

The partner was telling Kenji something specific. The discounted cash flow model is not what senior growth investors use to evaluate series-B valuations. They use comparable transactions in the same sub-segment, adjusted for the specific company. The cash flow model is a defence; the comparable-plus-premium answer is a conversation. The partner had asked the conversational question and Kenji had answered the defensive question, and the gap between the two had read to the partner as either inexperience or evasion. Kenji recovered the meeting by pausing, re-starting the answer with the comparable benchmark, and then walking the premium and the round-mechanics — but the recovery cost him five minutes and the lead partner’s quiet attention shifted to the second partner for the rest of the meeting. The fund passed two weeks later.

The valuation question is the single most consistently mishandled question in series-A through series-C investor pitches, and it is mishandled almost always in the same way: the founder defends the number rather than situating it. The defence triggers the partner’s pattern-match for inexperience; the situation triggers the partner’s pattern-match for a senior founder who has done the homework. This piece walks through why the question is asked, what the partner is actually testing, the four wrong answers that lose the round, the three-part honest answer that holds up, the follow-up questions to expect, the harder case of when the partner thinks the number is too high, and the structural homework that has to happen before the pitch.

Before the next investor pitch, a one-page reference of the questions senior partners ask is worth keeping close.

The 10 Questions Every CFO Asks reference walks through the ten objection-class questions senior finance audiences raise in pitches and board meetings — the valuation question, the unit-economics challenge, the runway question, the customer-concentration question — with the structural answer pattern for each. Free download, no email gate.

Why the question is asked, and what the partner is testing

The partner who asks “how did you arrive at that valuation?” is usually not asking because they want to negotiate the price down. The price-negotiation conversation happens later, in the term-sheet discussion, and it is handled by the partner’s investment-committee colleagues and the fund’s general counsel rather than in the pitch meeting. The pitch-meeting question is a different question. The partner is testing three things at once: whether the founder knows the market comparable, whether the founder can articulate the premium or discount to the comparable, and whether the founder has been through a real round-mechanics process or has set the number aspirationally without market validation.

The first test — whether the founder knows the comparable — is the most basic. A founder who cannot name the range that series-A or series-B rounds are currently pricing at in their sub-segment, within twenty percent, is signalling that they have not done the homework. The partner has done the homework: their internal data team produces sub-segment comparable analyses every quarter, and the partner reads the latest one before the pitch. The founder who walks into the room without the same data is at a structural disadvantage from the first question. The founder who names the comparable in the first sentence of their answer is signalling that they have done the same work the partner has done.

The second test — whether the founder can articulate the premium or discount — is the harder test. Every company prices either above or below the comparable median, and the reasons for the deviation are what the partner is most interested in. A founder who says “we are at the median” is rarely accurate; the partner knows the comparable median and knows whether the company sits above or below it. A founder who claims median when the deal is twenty percent above the median is signalling either ignorance of the data or unwillingness to engage with it. A founder who names the premium honestly — “we are pricing at fifteen percent above the median, and the reason is the net revenue retention” — is signalling the kind of structural honesty that senior partners value above almost any other founder attribute.

The third test — whether the round-mechanics produced the number — is the test that matters most to the investment committee in the post-meeting conversation. A valuation that came out of a real lead-investor process, with a term sheet from a credible lead and existing-investor support at the same price, is a valuation the committee can join at. A valuation that the founder set aspirationally and is now shopping to find a lead at is a valuation the committee will discount. The phrasing matters: “the lead-investor process produced a term sheet at this level” is a structural signal that the price is real; “we are targeting this valuation” is a structural signal that the price is not yet real.

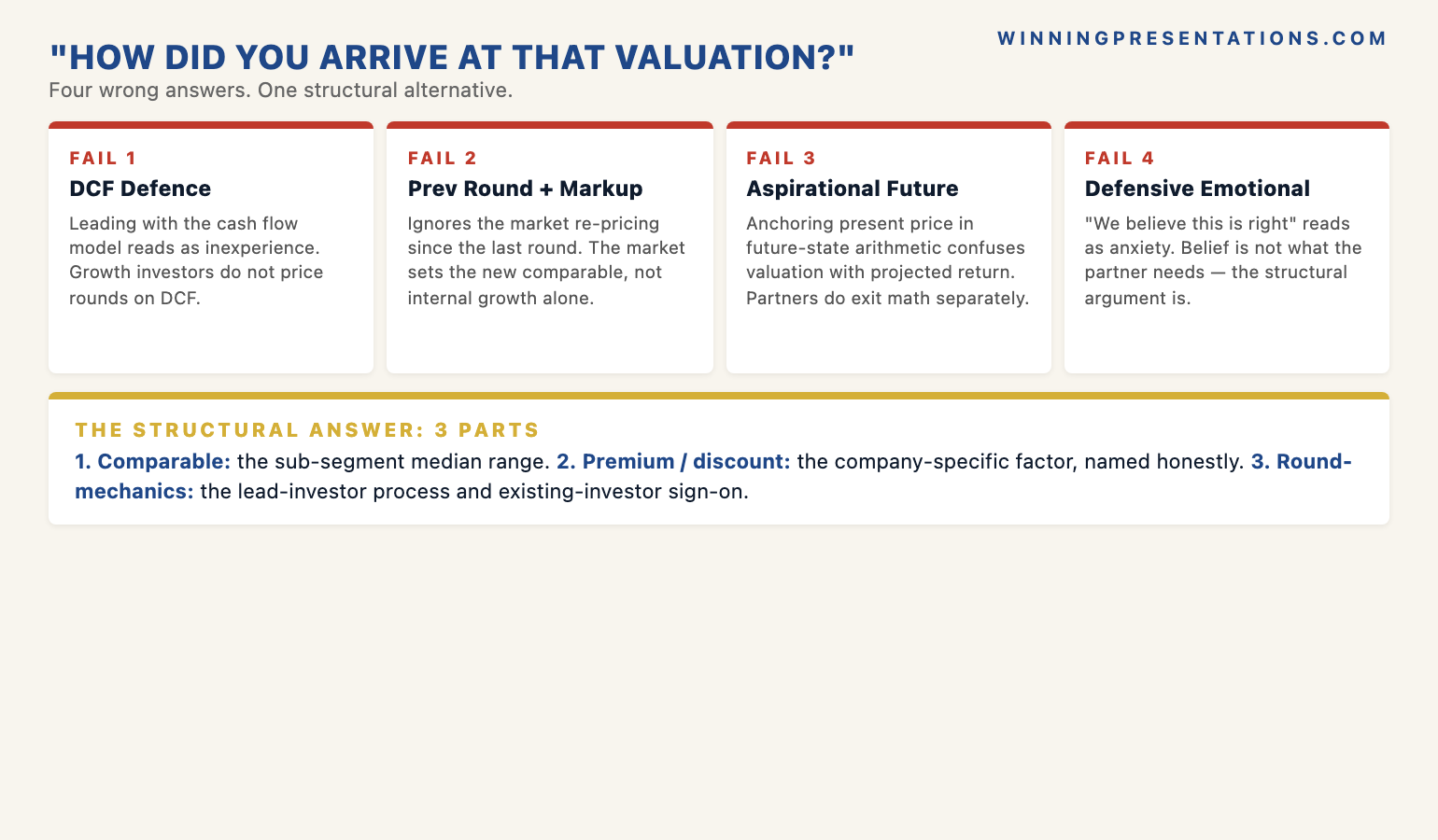

Four wrong answers and why each one loses the round

The first wrong answer is the discounted cash flow defence. The founder opens the answer with the cash flow model behind the valuation, walks the assumptions slide by slide, and arrives at the valuation as the output of the model. The partner reads this answer as inexperience. Discounted cash flow models are not what growth-stage investors price rounds on; they are what late-stage acquirers and public-market analysts use to model the company’s eventual exit value. A series-A or series-B valuation is priced on comparables, not on the founder’s discounted cash flow model. The founder who leads with the model is signalling that they have learned valuation theory from a textbook rather than from the market they are pitching into.

The second wrong answer is the previous-round-plus-multiplier answer. The founder says “we last raised at thirty million pre-money two years ago, and we have grown three times since, so sixty-five million is the right number.” The arithmetic is wrong about the market. Series-A-to-series-B markups are not a function of internal company growth alone; they are a function of where the comparable market is pricing rounds at the time of the new raise. A company that grew three times in a market where comparable multiples have compressed by half is priced at the new lower comparable, not at the previous-round price plus a growth multiplier. The founder who uses the markup framing is signalling that they have not absorbed the market move since their last round.

The third wrong answer is the aspirational future-state answer. The founder says “we are pricing at sixty-five million today because in three years we will be a four-hundred-million-dollar revenue company at a four-to-five-times revenue multiple, which is two billion, and a twelve-and-a-half percent dilution today gets you to two-fifty million on exit.” The future-state arithmetic is irrelevant to the present-round price. Growth investors price the present round on present-state comparables, with a structured premium for the trajectory if the trajectory is exceptional. A founder who anchors the present-round answer in the future-state arithmetic is signalling that they do not understand the difference between valuation (the present-round price) and projected return (the partner’s exit math). The partner is doing the projected-return math on their own; the founder’s job in the meeting is to ground the present-round price in the present-state comparables.

The fourth wrong answer is the defensive emotional answer. The founder says “look, we know this is a premium price, but we have done a lot of work to earn it, and this is the number we believe is right for the company.” The emotional framing reads as anxiety about the price. A senior partner does not need the founder’s belief in the price; the partner needs the structural argument for the price. The defensive answer signals that the founder is bracing for a no, which makes the no easier for the committee to give. The structurally confident answer — the comparable, the premium, the round-mechanics — signals that the founder is operating from market data rather than from belief, and the committee finds it harder to argue with market data than with founder conviction.

The three-part honest answer, in order

The first part is the comparable benchmark. The founder opens the answer with a single sentence naming the range that comparable rounds are currently pricing at in the company’s sub-segment. “The series-B round in our sub-segment — enterprise vertical SaaS in financial services — is currently pricing between six and nine times forward revenue, with the median at seven and a half.” The sentence does three things at once: it signals that the founder has done the comparable analysis, it gives the partner a shared market frame to anchor the rest of the answer, and it concedes the market reality before the partner has to remind the founder of it. The concession is the move. A founder who concedes the market frame in the first sentence has structural authority for the rest of the answer; a founder who waits for the partner to introduce the market frame has structural disadvantage.

The second part is the company-specific premium or discount, with the reason. “We are pricing at seven and a half times forward revenue, which is the median. The reason we are not above the median, despite the net revenue retention being one hundred and twenty-two percent (above the segment median of one hundred and fifteen), is that the gross margin at sixty-three percent is slightly below the segment median of sixty-six. The two effects roughly cancel, which lands us at the median.” The honesty about both the favourable factor and the unfavourable factor is the structural signal. A founder who names only the favourable factor — “we are above the median because of the net revenue retention” — is signalling cherry-picking, and the partner will mentally adjust the valuation downward for the unnamed factor. A founder who names both factors and lets the partner see the trade-off is signalling honesty, and the partner accepts the trade-off as fair.

The third part is the round-mechanics. “The lead-investor process produced a term sheet at this level eight days ago. The lead is [named fund]. Two of the three existing investors have signed on at the same price; the third is still in committee but has indicated support at the partner level.” The round-mechanics naming is the part that converts the valuation from a number the founder is asking for into a number the market has validated. A partner who is hearing the comparable-plus-premium answer is partway to a yes; a partner who is then hearing that a credible lead has already signed at the price is most of the way there. The structural pattern is to give the committee a number that another credible committee has already accepted, with a clear path for them to join at the same price.

The valuation question is one of roughly ten objection-class questions senior partners ask in every pitch. The structural answer for each one is learnable.

The Executive Q&A Handling System is the slide-and-script library senior pitch presenters use to prepare for the objection-class questions that decide investor meetings — the valuation question, the unit-economics challenge, the runway question, the customer-concentration risk, the competitive-differentiation question. Each question has a pre-built three-part answer structure and a practice script. Lifetime access, instant download. £39.

- A library of structured answer patterns — one per objection-class question — for the ten to fifteen questions that senior partners and committees ask in every pitch

- Practice scripts — the exact phrasing that converts a defensive answer into a structurally honest one, drilled in low-stakes practice runs

- The bridge-statement library — the short verbal moves that buy thinking time, redirect the question, and recover when the question lands harder than expected

- The red-lines guide — the questions the presenter should not answer in the room and the structural moves to defer them to follow-up materials

- Instant download — usable in tomorrow’s pitch

- Lifetime access, lifetime updates — £39

The follow-up questions to expect, and how to answer each

The honest three-part answer typically triggers one of three follow-up questions, and the founder should have a prepared structural answer for each. The first follow-up is the comparable challenge: “How are you defining your sub-segment for the comparable?” The partner is asking because the comparable median moves significantly depending on how narrowly the sub-segment is defined. A founder who has defined the sub-segment narrowly to land on a higher median is signalling cherry-picking. The structurally honest answer names the definition explicitly and offers the wider comparable as a sense-check: “Our primary comparable set is vertical SaaS in financial services with more than ten million in ARR. If you widen the set to all enterprise vertical SaaS, the median drops from seven and a half to six and a half — we land slightly above the wider median, which is consistent with the financial-services sub-segment premium our investor research shows.”

The second follow-up is the metric challenge: “Where are you getting the net revenue retention number?” The partner is asking because some companies report net revenue retention on a basis that flatters the number — including only the customers who renewed, for example, rather than including the churned customers in the denominator. The structurally honest answer names the methodology explicitly: “We report net revenue retention as the trailing-twelve-month revenue from the customer cohort that existed at the start of the period, including churned customers in the denominator, as a percentage of the same cohort’s revenue at the start of the period. The number is one hundred and twenty-two percent on that basis. The looser version of the metric — including only retained customers — would be one hundred and thirty-one percent. I am giving you the tighter version because that is the version the comparable analysis uses.” The methodology disclosure is the structural signal.

The third follow-up is the lead-investor probe: “Who is the lead, and have they signed?” The partner is asking because the credibility of the lead matters as much as the existence of the lead. A term sheet from a credible growth investor at the company’s stage is a strong signal; a term sheet from a fund that does not normally invest at this stage or sector is a weaker signal. The structurally honest answer names the lead, names the stage and sector fit, and offers the lead partner’s contact for direct reference: “The lead is [named fund]. [Named partner] is leading the round for them; he has invested in three other companies in our sub-segment in the past four years. I am happy to share his contact with you for a direct conversation; he has indicated he is available for committee questions from co-investors. The term sheet was signed eight days ago.” The willingness to make the lead partner available is the strongest possible signal that the round-mechanics are real.

When the partner thinks the valuation is too high

The harder version of the question is the one the partner asks when they think the valuation is too high relative to the comparable they have in mind. The signals are the same as the room going cold — the note-taking stopping, the cross-partner eye contact, the senior partner falling silent — but in this case the trigger is the specific number rather than the broader pitch. The partner’s internal frame is “the comparable median in our sub-segment is six times forward revenue, and the founder is pitching at seven and a half. The premium is not justified by what I am hearing about the company.” The founder’s structural challenge is to either find new information that justifies the premium, or to signal openness to a price discussion without dropping the price in the room.

The wrong response is to drop the price in the meeting. A founder who hears the partner’s discomfort and offers “we could come down to seven times” is signalling that the price was not real, and the committee will discount the price further in their post-meeting conversation. The structurally honest response is to name the discomfort, ask what specifically is driving it, and offer to follow up with the additional information that addresses it: “I can see the price is sitting higher than where you are calibrating. Can you tell me which comparable you are anchoring to and which company-specific factor is not coming through in the deck? I will send a follow-up note tomorrow with the specific data on whichever factor matters most to you, and we can re-discuss the price after you have had time to read it.” The response defers the price conversation to a structured follow-up rather than letting it become an in-meeting negotiation.

The partner’s response to the deferral will usually tell the founder whether the round is recoverable. A partner who engages with the question — who names the comparable and the company-specific factor that is bothering them — is a partner who is still in the deal and who can be moved by the follow-up information. A partner who deflects the question — “we will discuss internally and come back to you” — is a partner who has effectively decided to pass and is using the price as the reason. Both responses are useful to the founder. The engaged partner is worth the follow-up work; the deflecting partner is a signal to move attention to other parts of the round and to invest the recovery time in the next investor on the list. For the broader frame on how to read the room when the partner is shifting, see when you can see investors losing interest in real time.

Preparation: the homework that has to happen before the pitch

The structural answer to the valuation question depends on three pieces of homework, and the homework has to be done before the pitch starts. The first piece is the comparable analysis. The founder needs to know the median, the range, and the spread of comparable rounds in the relevant sub-segment over the trailing twelve to eighteen months. The data is available from several sources: the fund’s own published research where the fund publishes (some growth funds publish quarterly comparable reports), the major venture databases (Pitchbook, Crunchbase, CB Insights), the industry-specific reports from sector banks and analysts, and the founder’s network of recent fundraisers in adjacent companies. The analysis takes one focused day and is updated quarterly.

The second piece is the company-specific premium analysis. For each of the three to five metrics that drive valuation in the sub-segment — net revenue retention, gross margin, customer-acquisition cost payback, gross dollar retention, ARR growth rate — the founder needs to know where the company sits relative to the segment median, and have a one-sentence explanation for the position. The analysis is not a defence of the position; it is a structural understanding of the position, including the metrics where the company is below the median. The founder who understands both the favourable and unfavourable metrics, and has a coherent explanation for the overall position, can give the structurally honest answer in the meeting without rehearsing.

The third piece is the round-mechanics work. The founder needs to have actually run a lead-investor process, with a credible lead-investor candidate evaluating the deal and ideally signing a term sheet, before walking into the meetings with the co-investors who will follow the lead. The order matters. A founder who walks into the co-investor meetings without a signed lead is asking the co-investors to act as the lead, which most growth-stage co-investors will not do. A founder who walks in with a signed lead term sheet is offering the co-investors a price that another credible committee has already accepted, which is the easiest possible decision for the co-investors to make. The lead-investor process typically takes six to ten weeks; the co-investor process typically takes two to four weeks once the lead is signed. The founder who collapses the two processes into one is structurally disadvantaged in both. For the framing of the broader investor relationship once the round closes, see the investor update presentation format.

Frequently asked questions

What if we have not run a lead-investor process yet and we are pitching co-investors first?

The honest answer to the question changes. The founder cannot claim a lead-investor process that has not happened, and the attempt to do so will be detected by experienced partners who know the lead-investor landscape. The honest structural answer is to name the round-mechanics state truthfully and to frame the pitch as exploring the lead role rather than co-investor placement: “We are at the stage of identifying the lead. The pre-money we are anchoring the conversation on is sixty-five million, which lands at the median for the sub-segment. We are pitching three or four funds for the lead role; if your fund is interested in leading, the price is open to the lead’s diligence. If your fund is more naturally a co-investor at this stage, I want to flag that the price will be set by whichever lead signs the term sheet, and I would value your indication of co-investor interest at the median range.” The honesty about the round state is the structural signal; the attempt to bluff the round state is the structural failure.

What if we genuinely do not know what the comparable median is in our sub-segment?

The pitch is not ready yet. A founder who walks into a series-B pitch without knowing the comparable median is the structural equivalent of a sales presenter walking into a pitch without knowing the buyer’s industry. The diligence partners will detect the gap in the first five minutes. The structural response is to defer the meeting by two or three weeks, do the comparable analysis, and come back when the data is in hand. A short delay to do the homework is far less costly than a meeting that goes badly because the homework was not done. The partners will respect the delay; they will not respect the unprepared meeting.

How specific should the comparable analysis be in the deck itself, versus saved for the question?

One slide in the appendix is the right level of detail. The slide shows the comparable set (named companies or named transactions where the data is public, anonymised where it is not), the median, the range, and the company’s position. The slide is not walked in the main deck walk — it sits in the appendix and is navigated to when the question is asked. Walking the comparable slide pre-emptively in the main deck signals defensiveness about the valuation. Holding the slide in the appendix and navigating to it when the question is asked signals preparedness without pre-emption. The structural pattern is to have the slide ready but not to volunteer it; let the partner ask, then walk the slide as the answer to their question.

What if the partner challenges the comparable median itself — says our median is wrong?

This is one of the most useful questions a partner can ask, because it tells the founder exactly where the partner’s frame differs from the founder’s. The structural response is to ask the partner what comparable set they are using, and to be willing to revise the founder’s analysis based on what the partner says. “Can you tell me which comparable set you are anchoring to? Our analysis is based on [named set]; if you are working from a different set, I would value understanding it so I can reconcile the difference for the follow-up conversation.” The partner who answers the question is giving the founder the gold of the meeting: the specific data set the partner is using to evaluate the deal. The founder who absorbs that data set, reconciles it against their own, and comes back in the follow-up with a structured reconciliation is the founder who often closes a deal that initially looked like it would not close. The defensive response — “no, our comparable set is right” — is the response that ends the conversation.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly (Thursday) newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural answers that hold up to senior committee scrutiny. Subscribe to The Winning Edge →

For the broader picture across slides, storytelling, confidence, and delivery, the Complete Presenter bundle is the seven-product set most senior fundraisers find useful as a single library — £99 for everything, lifetime access.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.