Quick answer: The investor update presentation format that holds board attention in 2026 is a seven-section quarterly deck designed for a board that has already seen the numbers before the meeting starts. The seven sections, in order, are: a one-sentence headline of the quarter, the three to five operating metrics the board has signed up to watch, the variance to plan stated as a decision rather than a defence, the strategic narrative connecting this quarter to the next, the two or three asks of the board for the period ahead, the risks the board would otherwise raise themselves, and the calendar for the months between this meeting and the next. The deck is dense, short, and consciously written for an absent audience — the board members who will re-read it three days later when they have to brief their own partners and committees.

JUMP TO:

Astrid, a founder and chief executive of a Berlin-headquartered climate-tech series-B company, sent her board the Q1 2026 update deck on a Sunday afternoon, three days before the quarterly board meeting. The deck was thirty-eight pages long. It opened with a six-page company-context section, moved into a fourteen-page operating-metrics walk-through, then closed with a twelve-page strategic-narrative block and a final six-page asks-and-risks summary. The lead investor — a partner at a London growth fund — replied on Monday morning with a single line: “Could you send a one-page summary by tonight? I will not have read this before Wednesday.” Astrid spent Monday rebuilding the deck into a seven-page format. The board meeting on Wednesday ran fifty-five minutes instead of the scheduled ninety. The lead investor opened the meeting with a sharp, specific question about the customer-acquisition-cost trend on page three of the new deck; the rest of the board followed his lead. The meeting was the most useful Astrid had run all year.

The diagnosis is not that the long deck was bad. The metrics were correct, the strategic narrative was thoughtful, the asks were specific. The problem is that the board — five partners with full portfolios, parallel commitments to other companies’ boards, and a two-hour window to read whatever Astrid sent before walking into the meeting — was not in the room to be educated. They were there to make decisions about the next quarter. The thirty-eight-page format asked them to do reading first and deciding second; the seven-page format asked them to do the opposite. By the time the long deck got to the asks on page thirty-two, the board had already absorbed thirty-one pages of context; the short deck arrived at the asks on page five, with the board’s attention still intact.

This piece walks through the investor update presentation format that has been working for senior founders in 2026 across climate-tech, deep-tech, financial-services SaaS, and consumer-health series-A through series-C companies, what each of the seven sections has to carry, why the board has already done most of the reading before the meeting, how the deck has to survive the absent-reader test that the long format does not, and the small structural moves that hold board attention together when the numbers underneath the deck are mixed.

Before the next quarterly board update, a one-page structural check is worth a look.

The Investor Pitch Deck Checklist walks through the structure that holds up in front of senior boards — the headline section, the variance page, the asks section, and the risks-the-board-would-otherwise-raise page. Free download, no email gate.

Why seven sections and what changed

The seven-section number is not arbitrary. It is roughly the number of distinct decision-relevant pages a senior investor can hold in working memory across a sixty- to ninety-minute board meeting while also asking questions, comparing the company against other portfolio companies, and processing whatever the chief executive said in the pre-read circulated three days earlier. Push the count above twelve and the board’s mental model of the company starts to fragment; below five and the deck starts to feel like it is hiding something. Seven is the structural sweet spot, with the proviso that each section is built to carry a discrete piece of the conversation, not to demonstrate effort or rehearse what the board already knows.

What has changed since 2024, and changed sharply since the start of 2026, is the amount of preparation the board brings into the meeting. A growth-fund partner with five active board seats will routinely have used a portfolio dashboard, a notes-to-self summary written by their associate, and a sector benchmark from their internal data team to read the company’s metrics before opening the chief executive’s deck. The associate has often produced a one-page brief on what changed since the last quarter; the partner reads the brief, scans the headline numbers in the deck, and arrives at the meeting with two or three specific questions already prepared. The first fifteen minutes of a 2024 board update — context, market overview, team changes, headline-number narration — is now mostly redundant. The board already knows. The deck that recognises this and skips the redundant material reads as senior; the deck that re-walks ground the board has already covered reads as junior, regardless of the founder’s tenure.

The seven-section template is built around that change. The company-context section has been compressed into the one-sentence headline. The headline-number walk-through has been replaced with a single page of three to five operating metrics — the ones the board signed up to watch — and a variance comment underneath each. The strategic-narrative block has been compressed from twelve pages into one. What used to take twenty pages now takes three or four. The space that opens up is given to the sections the board cannot pre-produce from the dashboard: the asks for the period ahead, the risks the board would otherwise raise themselves, and the calendar for the months between this meeting and the next. Those three sections are where the seven-section deck earns its time in the meeting.

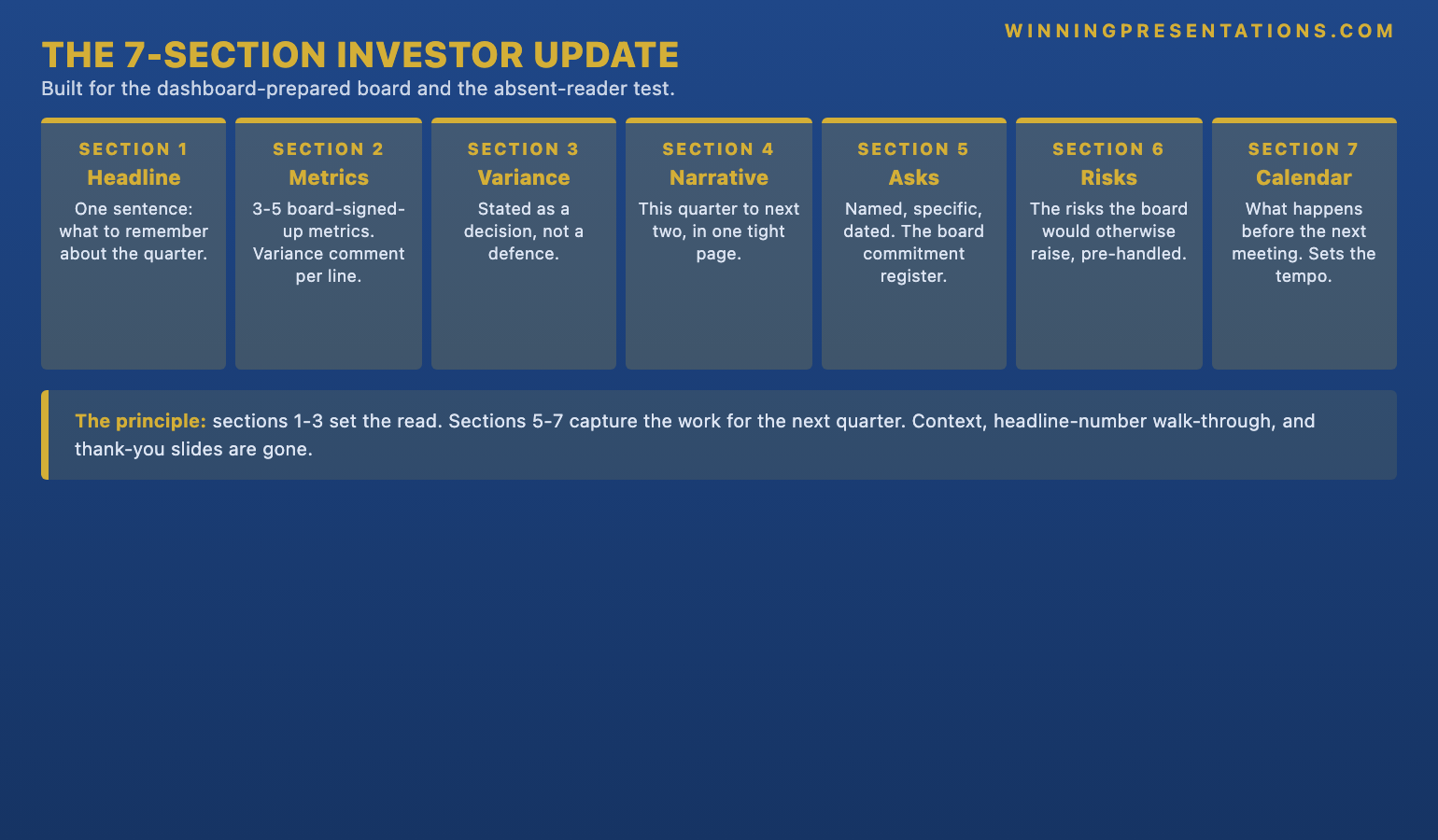

The seven sections, in order

The first section is the headline. A single sentence at the top of an otherwise nearly empty page, stating in plain English the most important thing the board needs to remember about the quarter. Not the topic, not the agenda, not the company name — the headline. An example: “Q1 2026 was the first quarter we held gross margin above sixty-two percent at scale, paid for by reducing the sales team by eleven percent.” The headline section is in the deck for one reason: it removes ambiguity about what the meeting is for. Senior boards waste a disproportionate amount of their attention in the first ten minutes trying to work out what the chief executive thinks happened; the headline gives them the answer in three seconds and frees the rest of the meeting to do the work.

The second section is the operating metrics page. Three to five metrics, the ones the board signed up to watch at the last fundraise — the customer-acquisition cost, the net revenue retention, the gross margin, the cash runway, and one company-specific metric that the chief executive watches as the leading indicator. Each metric is shown with the current quarter’s number, the plan number, the variance, and a one-line comment underneath explaining what drove the variance. The page does not include every metric the company tracks internally; it includes the metrics the board has agreed are the operating signal. The discipline is to keep the list short and to keep the comments honest — “missed the plan by twelve percent because the December enterprise renewal slipped into Q1” is more useful than “tracking broadly in line with plan.”

The third section is the variance to plan, stated as a decision rather than a defence. Two or three sentences. “We will hold the plan for FY26 in customer-acquisition cost. We will revise the headline gross-margin target down from sixty-five to sixty-two percent for the next two quarters, then re-test in Q4.” The variance section goes third, not last, for a specific reason: the board is reading the rest of the deck through the lens of whatever the chief executive thinks should change. If the variance is held back until page twenty, the board spends the first nineteen pages guessing what the chief executive’s read is, and arrives at page twenty either ahead of the founder or behind. Stating the variance as a decision collapses that gap and turns the rest of the deck into evidence rather than build-up. For the conversation that surrounds variance reporting when the board reaction is going to be hostile, see how to present to a board of directors.

The fourth section is the strategic narrative. One page. Three or four short paragraphs, or a clean three-block structure, connecting this quarter to the next two. The narrative is not the long-form thinking the founding team has been doing all quarter; it is the version of that thinking compressed to the point that the board can re-read it in ninety seconds and brief their own partners from it. The board’s partners — the people who did not attend the meeting but who will hear about it in the partner meeting on Monday — will form their entire view of the company’s direction from this single page. Writing for them, not for the meeting, is the discipline.

The fifth section is the asks of the board. Two or three specific requests for the period between this meeting and the next. Each ask is named: the specific introduction the chief executive wants the board to make, the specific commercial decision the board needs to ratify before the next quarter, the specific senior hire the board needs to weigh in on. The asks section is the single most under-used section in 2026 investor update decks and the one that most consistently separates a productive board relationship from a passive one. The board will offer help whether the asks section is in the deck or not. Putting the asks in the deck — specific, named, dated — transfers the help from a vague offer to a tracked commitment.

The sixth section is the risks the board would otherwise raise. Two columns. On the left, the three or four risks the chief executive expects the board to ask about — competitive threat, key-person dependency, customer concentration, a regulatory shift — surfaced explicitly. On the right, the chief executive’s specific mitigation for each. The risks page is the structural equivalent of the risk slide in a sales pitch: the board will discuss the risks whether the page is in the deck or not, and putting them in the deck transfers control of the risk conversation from the board to the chief executive. A risks page that lists only competitor noise and generic execution risk reads as box-ticking and the board discounts the entire page; a risks page that names the customer concentration concern the lead investor has been worrying about for two quarters reads as senior.

The seventh section is the calendar. Three or four lines. What specifically happens in the period between this meeting and the next — the planned fundraise milestones, the named senior hire interviews the board needs to be available for, the board sub-committee meetings, the off-cycle calls the chief executive plans to schedule. The calendar section is the section most often missing from quarterly decks, and it is the one that most consistently shapes whether the board feels managed or merely reported to. The chief executive who closes the deck with a calendar of what happens next is the chief executive who sets the tempo of the board relationship; the chief executive who closes with a thank-you slide is the chief executive who lets the board set it.

A seven-section investor update holds together because the underlying slides are built right — not because the deck is shorter.

The Executive Slide System is the slide library senior founders are using to build the headline slide, the operating-metrics page, the variance-as-decision page, and the asks-and-risks structure this quarterly format depends on — without rebuilding them from scratch every quarter. 26 templates, 93 AI prompts, 16 scenario playbooks. Lifetime access, instant download. £39.

- 26 executive slide templates — headline slides, operating-metrics layouts, variance-as-decision pages, three-block strategic narratives, asks-of-the-board structures, two-column risk-and-mitigation pages, calendar closes

- 93 AI prompts — for drafting, sharpening, and stress-testing each section in 30 minutes rather than three hours per board meeting

- 16 scenario playbooks — quarterly investor update, board approval, capital request, fundraising pitch, transformation update, and other high-stakes senior meetings

- Instant download — usable in the next quarterly cycle

- Lifetime access, lifetime updates — £39

The absent-reader test: what each section has to survive

A senior board update in 2026 is almost never read only by the people who attend the meeting. The five partners in the room are typically the lead investor (the partner who led the most recent round), one or two earlier-stage investors who stayed on the board, an independent non-executive director, and the company chair. Each of those five will brief at least one other person — an associate on the lead investor’s team, the earlier-stage fund’s monitoring analyst, the chair’s executive assistant who manages portfolio reporting — and the deck is the artefact those briefings are built from. The deck has to survive the absent-reader test. Every page is being read twice: once with the chief executive in the room, and once two or three days later by someone the chief executive will never meet.

The headline section has to survive the question “what was the most important thing about this quarter?” A single sentence at the top of an empty page makes that question easy to answer in the absent-reader briefing. The operating-metrics page has to survive the question “did the company hit plan?” Three to five metrics with a variance comment underneath each give the absent reader the answer without needing the chief executive’s narration. The variance page has to survive the question “what is the chief executive doing about it?” Stated as a decision in two or three sentences, the answer is unambiguous; left as a soft observation, it dissolves in the absent-reader brief.

The strategic-narrative page has to survive the question “where is this company heading and is the chief executive right about it?” A compressed three-block structure holds; a twelve-page narrative blur dissolves in absent-reader recall. The asks page has to survive the question “what does the chief executive want from us?” If the asks are named and dated, the partner can act on them between meetings; if they are vague, they evaporate. The risks page has to survive the question “what are the things that could go wrong, and is the chief executive thinking about them?” If the page is in the deck, the partner can point at it in the partner meeting on Monday; if it is not, the partner has to raise the risks themselves and the conversation goes against the chief executive. The calendar has to survive the question “when is the next thing we need to be ready for?” If the calendar is in the deck, the board has a structured way to commit time; if it is not, the next thing arrives unannounced.

What to cut from the old quarterly deck

The company-context section — the four-to-six page block that re-introduces the market opportunity, the product, the team structure, and the funding history at the start of every quarterly deck — is the single biggest casualty of the modern board-reporting environment. The board partner’s pre-read brief has covered all of it. Walking that material in 2026 is the structural equivalent of opening a board meeting in 2018 by reading the company’s mission statement aloud — it tells the room nothing new and it costs the chief executive eight to twelve minutes of the available attention. The context material has not gone away; it lives in the company’s data room and in the partner’s notes, and it is referenced where it adds evidence. The standalone context section has not survived.

The headline-number walk-through is the second casualty. In 2024 it was useful for the chief executive to walk the board through ARR growth, customer count, headcount, and cash burn slide by slide. In 2026 the partner has either read those numbers in the dashboard before the meeting or, more often, has the variance summary in the associate’s brief alongside the company’s deck, and the time spent walking the numbers reads as the chief executive filling time rather than making the case. The numbers belong on the operating-metrics page — three to five lines, with the variance comment, in one page total.

The thank-you slide and the team-photo slide are the third casualty. The five-slide closing block that thanks the board, summarises the company values, and shows the team off-site photo is now compressed into a one-line closing inside the calendar section: “Next board meeting: 18 September. Off-cycle leadership update call: 12 August.” The board appreciation is implicit in the chief executive’s continued investment in the relationship; the team photo, if needed for portfolio marketing, lives in the company’s quarterly newsletter rather than in the board update. Closing the deck with a calendar rather than a thank-you signals the chief executive is running the relationship as work, not as performance.

When the quarterly update is the moment the board makes a real decision — a follow-on, a senior hire ratification, a strategic pivot — the deck only does half the work.

The Maven Executive Buy-In Presentation System is the self-paced programme senior founders use to walk a board through the absent-reader conversation — the structured method for pre-handling the partner meeting on Monday, mapping the investment committee, and designing the post-meeting tempo so the board signs off when they meet without you. 7 modules, self-paced with monthly cohort enrolment, optional recorded Q&A calls. £499, lifetime access to materials.

Reporting a bad quarter without padding it

The seven-section format is at its most useful when the quarter has gone badly. The instinct of an inexperienced chief executive in a bad quarter is to write a longer deck. More context to explain the miss, more narrative to soften it, more strategic ambition for the next quarter to compensate. The board reads the longer deck as anxiety, and the anxiety is more damaging to the board relationship than the miss itself. The seven-section format does the opposite: a bad quarter compresses to a shorter, sharper deck, because the strategic narrative section has more to say in fewer words and the asks section is more specific.

The discipline in a bad quarter is in the headline section and the variance section. The headline names the bad number on the first page — “Q1 2026 missed the revenue plan by sixteen percent” — rather than burying it on page twelve where the board will find it anyway and resent the burial. The variance section states what the chief executive will do about it as a decision, not as a hope — “we will pause the planned September European launch and reallocate the budget into pipeline-acceleration with existing accounts for the next two quarters” — rather than describing the miss as a learning moment. The strategic narrative section then connects the decision to the longer plan, the asks section names the specific board support needed to execute the decision, and the risks page names the second-order risks the decision creates. The whole deck is three to five pages longer than a good-quarter deck, because the decisions and risks need more space; the headline section, operating-metrics page, and calendar section are unchanged.

The board’s read of a bad-quarter seven-section deck is consistently more favourable than the read of a long, defensive deck reporting the same numbers. The board has worked with chief executives who hit and missed plans across many quarters and many companies; the chief executives whose long-term board relationships hold are the ones who report bad quarters with the same structural discipline as good quarters, not the ones who pad the bad quarters with extra context.

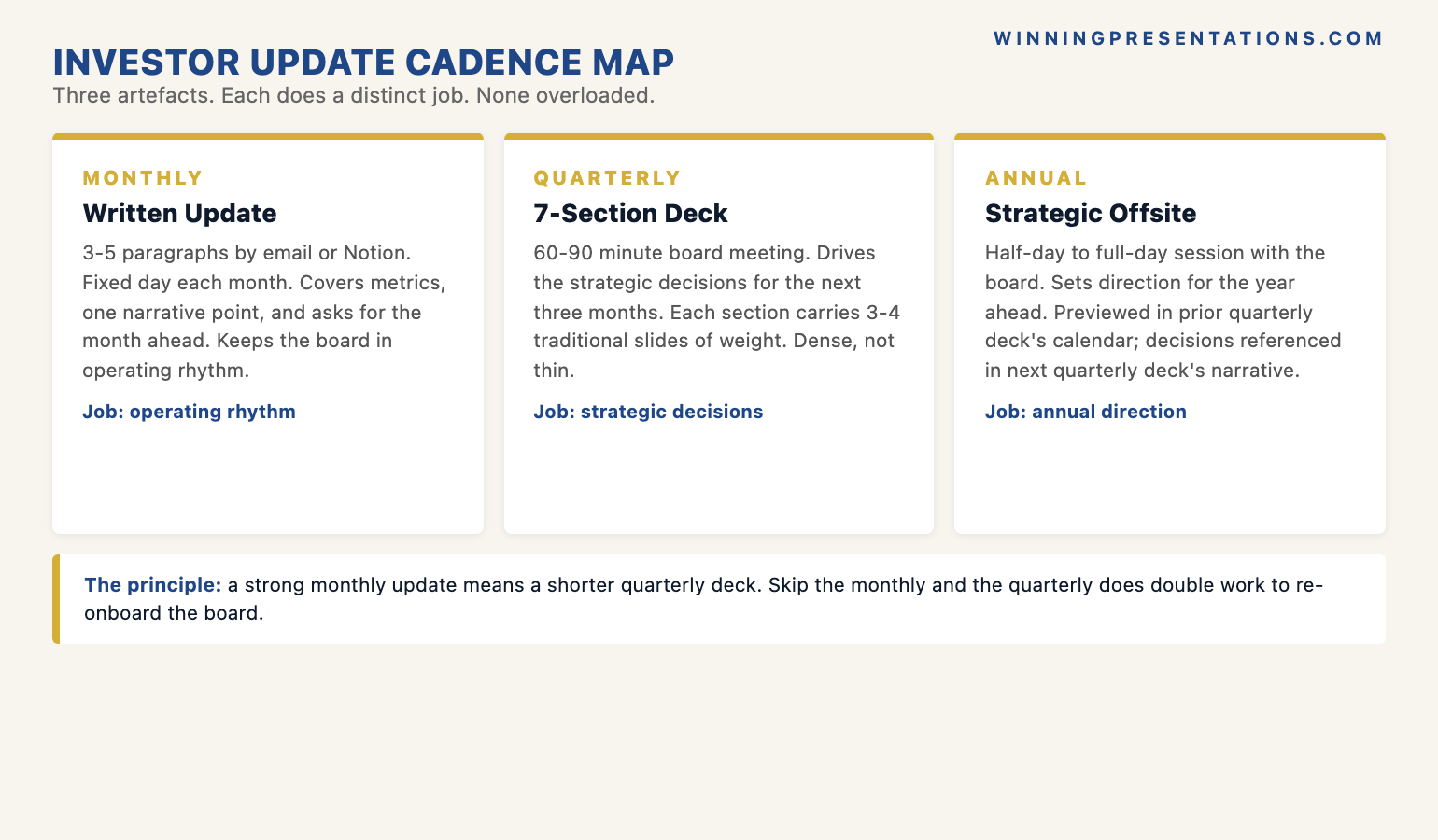

Cadence: how the quarterly update sits next to the monthly

The seven-section quarterly deck does not replace the monthly investor update. The two artefacts do different work. The monthly update is a written email or short Notion document — three to five paragraphs, sent on a fixed day each month, covering the operating metrics, one short narrative point, and the asks for the month ahead. The monthly update keeps the board in the operating rhythm and removes the need for the quarterly deck to re-narrate basic operating context. The quarterly deck is the longer, structured artefact that drives a sixty- to ninety-minute board meeting and sets the tempo for the next three months. The chief executive who writes a strong monthly update can write a shorter quarterly deck; the chief executive who skips the monthly update has to do twice the work in the quarterly meeting to bring the board back up to speed.

The annual strategic offsite is the third artefact in the cadence. Once a year, the board sits with the chief executive for half a day to a full day to work through the strategic plan for the year ahead. The quarterly deck for the meeting before the offsite includes a one-page preview of the offsite agenda in the calendar section; the deck for the meeting after the offsite includes a one-page reference to the offsite decisions in the strategic-narrative section. The three artefacts — monthly written update, quarterly seven-section deck, annual offsite — together cover the whole work of board reporting without overloading any one of them. The chief executive who treats each artefact as having a distinct job, and does not try to make any one of them do the work of the other two, runs the board relationship that holds across the four-to-six-year arc of a typical venture-backed company.

Frequently asked questions

Is seven sections really enough for a series-B-plus board with five investors and an independent chair?

It is, when the seven sections are built to carry the decisions rather than to demonstrate effort. The mistake is to read “seven sections” as a length constraint and assume the deck has to be thin. The seven sections in this format each carry as much information as three or four pages in a traditional long-form board deck — the headline is a one-sentence read of the quarter, the operating-metrics page compresses what used to be a five-to-eight slide walk-through, the variance section is a board-ready decision, the strategic narrative compresses what used to be a twelve-page narrative block into one tight page, the asks page is a named-and-dated commitment register, the risks page is a pre-handled objection map, and the calendar is a tempo plan. The deck is dense, not thin. The seven-section count keeps it cognitively manageable for a sixty- to ninety-minute board meeting; the depth inside each section is what makes it sufficient.

What if the lead investor asks for the long-form thinking behind the strategic narrative section?

It lives in an appendix the chief executive does not walk by default. The appendix typically contains the longer-form strategy document, the detailed competitive analysis, the customer cohort breakdown, the senior team’s operating plan, and the model build with all underlying assumptions. When a board member asks “can you show us more on the rationale for the European launch pause?”, the chief executive navigates to the relevant appendix section, walks the page, then returns to the main deck. The appendix is the chief executive’s safety net; it is not a path through the meeting. The discipline is to keep the appendix in the file but never to volunteer it. The board members who want to read the long-form thinking will ask for it, and the appendix gives them somewhere to go without forcing the rest of the board to sit through it.

Does the seven-section format work for an early-stage seed company with two angels and no formal board?

Not in the same shape, but the structural principles transfer. A seed-stage company with informal investor reporting does not need a seven-section quarterly deck; it needs a strong monthly written update and an annual half-day strategic conversation. The seven-section format becomes useful when the board has three or more investors with formal governance rights, when the meetings are scheduled and minuted, and when the chief executive is presenting to people who did not sit in the day-to-day operating conversation in the weeks leading up to the meeting. For seed-stage chief executives, the discipline to learn now is the headline-first habit and the variance-as-decision habit; the seven-section format becomes the natural shape once the board grows past three formal investors.

How is this different from the standard YC update template or the SaaStr quarterly format?

It is a board-meeting deck rather than an email or written update format, and it is compatible with both. The YC update template’s “asks, lowlights, highlights, key metrics” structure can sit inside the monthly written update that feeds this quarterly deck; the SaaStr quarterly metrics breakdown can be the source data for the operating-metrics page in section two. What this format adds, and what most named templates have not yet adjusted to, is the compression of the headline-number walk-through that the dashboard-prepared board now makes redundant, the elevation of the variance-as-decision page from a closing summary to a structural third section, and the elevation of the asks-and-risks pages from afterthoughts to the structural fifth and sixth sections. The template underneath the deck is the chief executive’s choice; the structural shape has to fit the way 2026 boards actually read and decide.

What happens when the board disagrees with the variance-as-decision section?

The disagreement happens in the meeting, which is the right place for it. The board challenges the variance decision, the chief executive walks the reasoning, the board pushes back on one or two elements, and the meeting reaches one of three outcomes: the board accepts the decision, the board modifies it together with the chief executive, or the board parks it for a follow-up sub-committee call. All three outcomes are productive. The structural alternative — burying the variance in a soft narrative and hoping the board does not notice — is what produces the bad board relationship over time. Boards remember the chief executives who brought variance decisions into the room as decisions; they remember the chief executives who hid variance even more clearly, and the memory shapes the next funding decision.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly (Thursday) newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate decks boards back from decks they defer. Subscribe to The Winning Edge →

For the broader picture across slides, storytelling, confidence, and delivery, the Complete Presenter bundle is the seven-product set most senior founders find useful as a single library — £99 for everything, lifetime access.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.