Fundraising Pitch for Impact Investors: How to Blend Mission and Returns Without Losing Credibility

Quick answer: The fundraising pitch for impact investors that holds up in 2026 is a structurally honest pitch that names the financial return target on the same page as the impact thesis — not in a separate appendix and not on a slide the founder hopes the committee skips. The deck has eight pages, in order: the impact-and-returns headline, the problem framed in both impact and commercial terms, the solution, the impact thesis with named outputs and measurement methodology, the commercial model with the unit economics and the return target, the team and the impact-economics fit, the risks specific to blended-return investments, and the named ask. The structural discipline is to keep both sides of the blended-return equation visible on every page where one of them appears, so the investment committee never has to choose between the impact story and the financial story.

JUMP TO:

- Why the blended pitch is harder than either side alone

- The eight pages, in order

- The measurement methodology page

- The investment committee: how blended-return funds actually decide

- Three common mistakes that lose the room

- Sector-specific calibration: climate, health, education, financial inclusion

- Frequently asked questions

Ngozi, the founder of a Nairobi-headquartered agricultural-finance company, pitched a London-based impact fund for a series-A round of seven and a half million pounds. The deck was twenty-six pages long. The first nine pages were the impact story: the smallholder farmers being served, the climate-adaptation outcomes, the gender-distribution data, the alignment with the fund’s stated impact theses. The next twelve pages were the commercial story: the unit economics, the loan-portfolio performance, the cost of capital, the path to profitability. The final five pages were the ask, the team, and the appendix. The pitch lasted ninety minutes. The investment committee thanked Ngozi at the end and said they would discuss internally. Three weeks later the partner came back with a soft no: the committee could not reconcile the impact story with the commercial story because the two stories had been told in separate halves of the deck and the committee had spent the post-meeting conversation arguing about which half to believe.

The diagnosis is not that the impact story was weak or the commercial story was weak. Both were strong. The problem is that the deck had structurally separated them, and the committee — a five-person group with two partners weighted toward impact and three partners weighted toward returns — had no integrated artefact to reach consensus around. The impact partners read the first nine pages and were ready to say yes; the returns partners read the next twelve pages and were ready to say no; the deck did not give either group a page that resolved the tension between them. In the absent-investor conversation that followed the meeting, the committee’s natural cognitive split became a structural disagreement, and the disagreement defaulted to no.

This piece walks through the fundraising pitch for impact investors that has been working for founders in 2026 across agricultural finance, climate technology, healthcare access, education technology, and financial-inclusion companies raising from blended-return funds — the funds that target both a measurable impact outcome and a market-rate or near-market-rate financial return. The piece covers what each of the eight pages has to carry, why the impact thesis and the commercial model have to share every page where one of them appears, how the investment committee actually decides in funds with mixed impact and returns mandates, and the small structural moves that prevent the committee from splitting into two camps that talk past each other.

Before the next blended-return pitch, a structural check on how the deck argues its case is worth a look.

The Pyramid Principle template is the one-page structure-first framework most senior pitch builders use to keep the recommendation and the supporting evidence in the same visible logical chain — the discipline that prevents an impact pitch from splitting into two parallel stories. Free download, no email gate.

Why the blended pitch is harder than either side alone

A pure venture pitch and a pure philanthropic pitch are both structurally easier than a blended-return pitch. The venture pitch is built around a single optimisation function: the return on invested capital. Every page either serves that argument or it does not belong. The philanthropic pitch is built around a different single function: the impact outcome per pound spent. Every page either serves that argument or it does not belong. In both cases the deck has one master variable and every other variable is in service to it.

A blended-return pitch has two master variables and they sometimes pull in different directions. A loan-portfolio company serving smallholder farmers in East Africa, for example, can deepen its impact by lending smaller amounts to more farmers (more reach, more depth), but the same move increases the operational cost per loan and depresses the net financial return. The impact partner on the investment committee reads the smaller-loan strategy as a strong impact signal; the returns partner reads the same strategy as a margin risk. Both are right. The deck has to give the committee a way to hold both readings simultaneously, rather than forcing them to choose between the two.

The structural mistake is to present the impact case and the commercial case sequentially — impact in the front of the deck, commercial in the back — and to leave the integration work to the committee’s post-meeting conversation. The committee will not do the integration work the founder did not do. The committee will either default to no (the safe outcome when two partners disagree) or it will let one partner’s view dominate (the politically unstable outcome that often falls apart when the partnership re-discusses the deal at the next meeting). The deck that holds is the deck that does the integration work on every page where either variable appears: every impact claim shows up next to its commercial implication, and every commercial claim shows up next to its impact implication.

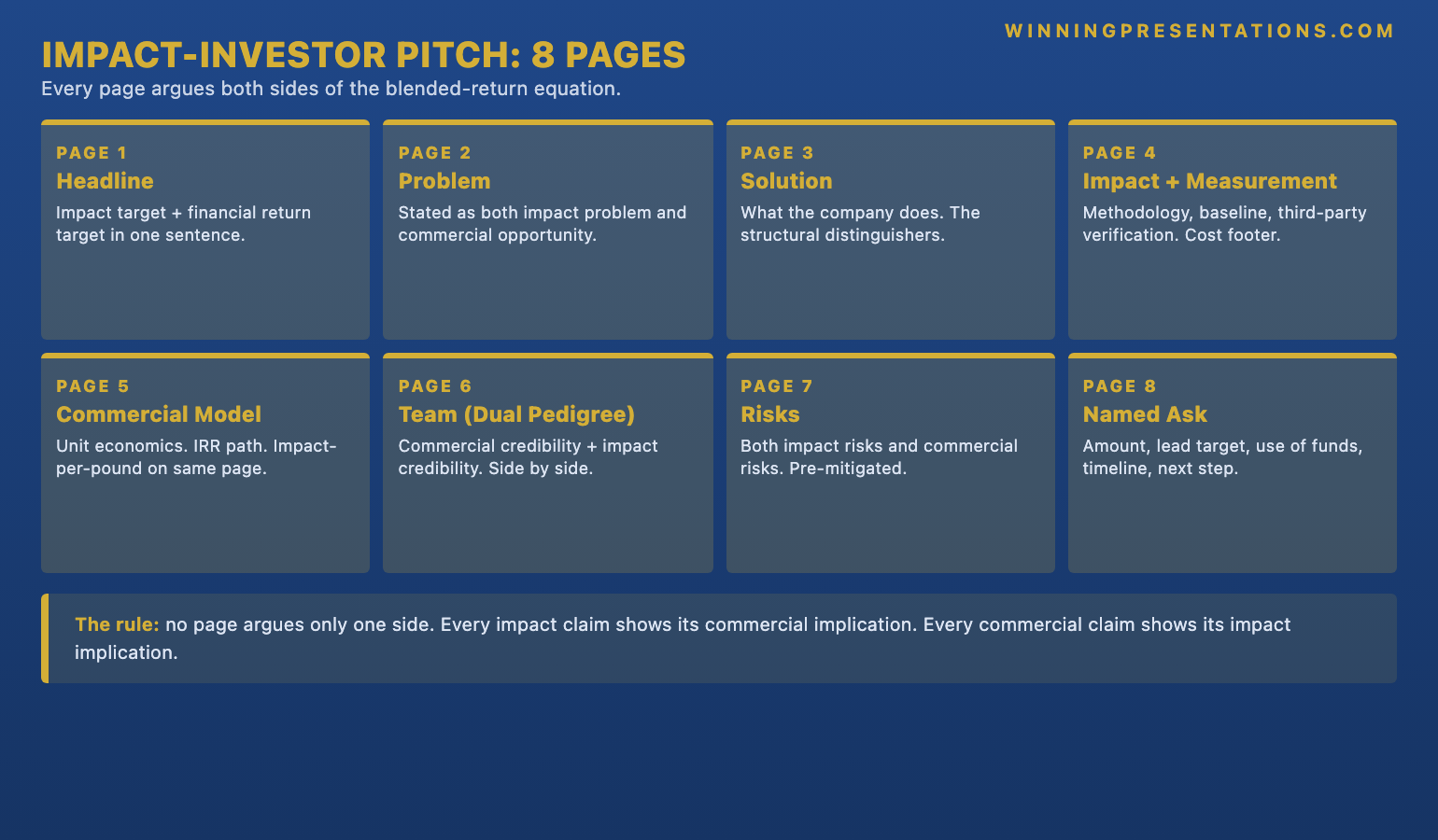

The eight pages, in order

The first page is the impact-and-returns headline. A single line near the top of the page stating, in the same sentence, the impact target and the financial return target. An example: “We are raising seven and a half million pounds to extend agricultural credit to one hundred and twenty thousand additional smallholder farmers in East Africa over four years, while delivering a twelve to fourteen percent net IRR to investors at fund close.” The headline page contains nothing else of substance. Its job is to put both variables in the committee’s mind in the first thirty seconds, so that every page that follows is read with both variables in view. The pitch that opens with a story about a single farmer — an emotional opening designed to win the impact partner’s heart — loses the returns partner before page two. The headline-with-both-numbers opens for both readers at once.

The second page is the problem. Two columns or two stacked sections. On one side, the problem stated as an impact problem: the unmet need, the population affected, the structural reasons the need has gone unmet by either pure-market or pure-philanthropic actors. On the other side, the same problem stated as a commercial opportunity: the size of the addressable market, the price elasticity of the population’s willingness to pay, the unit economics of the solution at scale. The two framings reinforce each other rather than competing. The page makes clear that the impact problem and the commercial opportunity are the same underlying market failure, not two separate pitches.

The third page is the solution. One page. What the company does, who it serves, how it is structured operationally. The page names the operating model in plain language and includes the one or two structural details that distinguish this company from adjacent solutions — the proprietary credit-scoring methodology that allows lending to under-documented farmers, for example, or the satellite-data integration that allows climate-resilience pricing. The solution page is short because the impact thesis and commercial model pages will go deeper; the solution page sets up the depth that follows.

The fourth page is the impact thesis with measurement methodology. This is the page where blended-return pitches most often fail. The page names the three to five impact outcomes the company will measure, the methodology by which it will measure them, the baseline against which it will measure them, and the third-party verification framework it will use to report them. The page also names, in a footer or sidebar, the commercial cost of the measurement work itself — the staff cost, the verification fee, the data infrastructure cost — so the returns partner can see that the measurement work is funded within the commercial model rather than being a separate ask. The impact partner reads the measurement methodology as the seriousness of the impact commitment; the returns partner reads the cost footer as the seriousness of the commercial discipline.

The fifth page is the commercial model with unit economics. This is the page where pure-venture pitches usually live, and it is the page that has to do the most translation work in a blended-return pitch. The page shows the unit economics — revenue per unit, cost per unit, gross margin, customer-acquisition cost, lifetime value — and a path to the targeted net IRR over the fund’s expected holding period. The page also includes, in the same view, the impact-per-unit-of-capital alongside the financial return. The two metrics share the page rather than living in separate sections. A returns partner can read the financial path and a impact partner can read the impact-per-pound, and both partners are reading the same page rather than separate sections that have to be reconciled later.

The sixth page is the team and the impact-economics fit. The standard team page in a venture deck shows the founders’ commercial pedigree — the previous companies, the previous exits, the relevant operating experience. The team page in an impact pitch adds the impact pedigree: the previous community work, the sector-specific impact experience, the cultural credibility in the markets the company serves. The two pedigrees sit side by side on the same page, with a short structural argument explaining why the combination is the right one for the blended-return work. The page closes any latent partner question about whether the founders are credible on both sides; the partner whose question is left unanswered will become the partner who blocks the deal.

The seventh page is the risks specific to blended-return investments. Two columns. On the left, the three or four risks the committee is most likely to raise privately after the meeting — impact-financial trade-off risk, measurement gaming risk, mission drift under commercial pressure, regulatory ambiguity in the markets served. On the right, the company’s specific mitigation for each. The risks page is the structural equivalent of the risk slide in a sales pitch, and it is more important in a blended-return pitch than in either pure venture or pure philanthropic pitches because the committee’s risk vocabulary is doubled: the committee will name both impact risks and commercial risks. Naming both in the deck pre-empts the committee’s instinct to raise them as objections. For the broader picture on how to structure quarterly board reporting once the fundraise is closed, see the investor update presentation format.

The eighth page is the named ask. Three or four lines. The specific amount being raised, the specific use of funds broken down by category, the named lead investor the company is targeting, the timeline for closing the round, and the named next step in the process. The ask page closes the deck the same way it closes a sales pitch: with a specific, dated, named request rather than a soft thank-you. The committee that has worked through seven dense pages is ready to make a decision; the named ask gives them a structured way to commit or push back.

An eight-page blended-return pitch holds because each page does its integration work — not because the pitch is shorter.

The Executive Slide System is the slide library senior fundraisers are using to build the impact-and-returns headline, the integrated unit-economics page, the impact-thesis page with measurement methodology, and the two-column risks page this pitch format depends on — without rebuilding them from scratch every fundraise. 26 templates, 93 AI prompts, 16 scenario playbooks. Lifetime access, instant download. £39.

- 26 executive slide templates — headline pages, problem-as-opportunity layouts, integrated unit-economics structures, impact-with-measurement pages, dual-pedigree team layouts, two-column risk pages, named-ask closes

- 93 AI prompts — for drafting, sharpening, and stress-testing each page before the investment committee pitch in 30 minutes rather than three hours per page

- 16 scenario playbooks — fundraising pitch, investor update, board approval, transformation update, capital request, and other high-stakes senior meetings

- Instant download — usable in tomorrow’s pitch

- Lifetime access, lifetime updates — £39

The measurement methodology page

The impact-thesis page is the page where senior impact investors test whether the founder takes the impact commitment seriously. The test is not whether the impact story is moving — almost every impact story is moving when told well — but whether the measurement methodology is rigorous enough to hold up under independent scrutiny when the fund reports to its own limited partners. Limited partners in impact funds have become structurally more demanding about impact measurement since 2024, partly driven by the European Sustainable Finance Disclosure Regulation, partly by the Operating Principles for Impact Management framework that most major impact funds now signal alignment with, and partly by the post-2022 reputational damage that loose impact claims caused across the sector. The fund’s own measurement standards are now an institutional commitment, and a pitch that does not meet those standards cannot clear the committee.

The measurement methodology page names the framework explicitly — IRIS+, the SDG indicator set, GIIRS, or the company’s own published methodology with a third-party verification partner — and shows three to five outcome indicators with the baseline, the target, and the measurement cadence. The page does not claim attribution beyond what the methodology supports. A loan-portfolio company can claim attribution for credit access; it cannot claim attribution for the subsequent change in farmer income unless it has the longitudinal study to back the claim. The discipline of naming the limits of attribution is itself a credibility signal to the impact partner, who has seen too many decks claiming impact outcomes the methodology does not support.

The commercial side of the measurement methodology page — the footer or sidebar showing the cost of measurement — is the page where the returns partner forms their view of the founder’s commercial discipline. A founder who has not thought about the cost of the measurement work, or who treats measurement as an external philanthropic add-on rather than a funded line in the operating model, signals to the returns partner that the impact commitments will erode the financial return. A founder who shows measurement as a fully funded operating cost, with the cost-per-outcome calculated and the trade-off understood, signals that the blended-return architecture is internally coherent.

The investment committee: how blended-return funds actually decide

A blended-return fund’s investment committee typically has five members: two partners weighted toward impact (the impact-side partners), three partners weighted toward returns (the returns-side partners), and the chief executive of the fund who chairs the meeting. The exact ratio varies — some funds run three-impact-and-two-returns, others run four-returns-and-one-impact — but the structural tension between the two camps is consistent. The decision is rarely made unanimously. Most blended-return investment decisions are made by a four-to-one or three-to-two vote, with the chief executive’s swing vote breaking ties when needed. The pitch has to be persuasive to enough partners on both sides to clear the voting threshold, not just to win the partners on one side.

The committee meeting itself typically runs for an hour, with the founder presenting for twenty to twenty-five minutes and the remaining time given to committee questions. The post-meeting conversation — where the actual decision is formed — runs longer, usually thirty to forty-five minutes with the founder no longer in the room. The deck has to survive that absent-founder conversation more than it has to survive the live meeting. Every page is being read twice: once with the founder present and once two days later when the deck is the only artefact in the conversation. The impact partners and the returns partners argue from the same pages, and the pages either hold the argument together or they do not.

The pages that most consistently hold are the integrated pages: the impact-and-returns headline, the impact-thesis page with the cost footer, the commercial model page with the impact-per-unit alongside the financial return, the two-column risks page that names both impact risks and commercial risks. The pages that most consistently fail are the sequential pages: the impact-only section in the front of the deck, the commercial-only section in the back, the team page that shows only one side of the dual pedigree. The structural rule is that no page in a blended-return pitch can argue only one side of the blended-return equation; every page has to do the integration work that the committee will otherwise refuse to do for the founder.

When the investment committee is going to take the deal away to a partner meeting before deciding, the deck only does half the work.

The Maven Executive Buy-In Presentation System is the self-paced programme senior founders use to walk a pitch deck through the absent-founder conversation — the structured method for mapping the committee, pre-handling the partner-by-partner objections, and designing the post-meeting tempo so the committee says yes when they meet without you. 7 modules, self-paced with monthly cohort enrolment, optional recorded Q&A calls. £499, lifetime access to materials.

Three common mistakes that lose the room

The first common mistake is leading with the emotional story. A founder opens with a single farmer’s story, told over two pages with photographs and a quote. The impact partners are moved. The returns partners read the opening as the founder signalling that the pitch is going to be impact-heavy and returns-light, and they form their reservation before the deck reaches the commercial model on page eight. The fix is to lead with the integrated headline page and to use the single-farmer story later, as a one-paragraph anchor inside the impact-thesis page, with the commercial cost-per-outcome footer visible on the same page. The story still does its emotional work, but it does it inside an integrated frame rather than as a stand-alone hook that splits the room.

The second common mistake is treating the impact thesis as a separate add-on rather than an integrated part of the commercial model. A founder presents a fully formed commercial model on pages five and six, then adds the impact section on pages seven and eight as if the impact work were a bonus the company would do alongside the commercial work. The impact partners read the structure as a signal that the impact commitments are commercially expendable; the returns partners are reassured but mildly insulted that they are being treated as the audience that does not care about impact. The fix is structural integration on every page, not a separate impact section that can be skipped or expanded depending on the audience.

The third common mistake is over-promising on impact attribution. A founder claims direct attribution for downstream outcomes the company has not measured and could not measure without a longitudinal study the company is not running — “our credit will increase smallholder farmer incomes by twenty-three percent over five years” when the company has measured credit access but not income change. The over-promise is detected immediately by the impact partner, who has read enough decks to know what attribution is supportable and what is not, and the over-promise destroys the credibility of the rest of the impact thesis. The fix is to claim only what the measurement methodology supports, to name the limits of attribution explicitly, and to commit to the longitudinal study as a planned investment in measurement infrastructure that the next funding round will pay for. The honest claim is more persuasive than the over-claim, especially to the impact partner who is the most attentive reader on the page.

Sector-specific calibration: climate, health, education, financial inclusion

The eight-page format works across most blended-return sectors, but each sector calibrates two of the pages differently. Climate-technology pitches typically need a deeper version of the impact-thesis page, because climate impact measurement has the most rigorous external standards (the carbon-accounting protocols, the science-based targets framework, the Sustainable Aviation Buyers Alliance methodology for the aviation-fuel subset) and the impact partners read climate pitches against those standards. The eighth page — the named ask — can be shorter, because climate funds typically have well-defined ticket sizes and decision processes.

Health-access pitches typically need a deeper version of the risks page, because health interventions carry regulatory, clinical, and ethical risks that the committee will probe more aggressively than in other sectors. The team page also has to do more work to establish clinical credibility — named clinical advisors, named regulatory expertise, named ethical-review processes — alongside the operating-commercial credibility that the standard team page covers.

Education-technology pitches face a particular structural problem: the impact-and-returns headline page is hardest in education, because educational outcomes are slow-attribution (the lifetime-earnings impact of a better primary-school year takes a decade to measure) and the commercial model often depends on government or institutional purchasing cycles that are themselves slow. The headline page in an education pitch typically uses a leading-indicator outcome (attendance, completion, attainment-test scores) rather than a long-term outcome, and the impact thesis page commits to the longitudinal-study infrastructure that will eventually let the company report on the deeper outcomes.

Financial-inclusion pitches — the agricultural-finance example used throughout this piece — have the most developed measurement standards (the financial-inclusion sector has been measuring the same things for fifteen years), but they have the most challenging commercial-impact trade-offs because the cost of serving the lowest-income segments often makes the unit economics tighter than mainstream lending. The commercial model page in a financial-inclusion pitch typically does more work than in other sectors to show how the impact-aligned segmentation strategy (smaller loans, longer repayment terms, broader rural distribution) is commercially defensible at scale rather than only commercially defensible with subsidy.

Frequently asked questions

Is eight pages enough for a series-A or series-B blended-return pitch?

It is, when the eight pages do their integration work and an appendix carries the deeper supporting material. The mistake is to read “eight pages” as a length constraint and assume the deck has to be thin. The eight pages each carry as much information as three or four pages in a traditional sequential deck — the headline page is the entire blended-return thesis in one sentence, the problem page is the integrated impact-and-commercial framing, the impact-thesis page is the measurement methodology with the cost footer, the commercial model page is the integrated unit economics with the impact-per-pound alongside the financial return, the team page is the dual pedigree, the risks page is the pre-handled objection map for both impact and commercial risks, and the ask is the named close. The appendix carries the longer-form impact measurement methodology, the detailed financial model, the regulatory analysis for the markets served, the team biographies, and the impact-measurement infrastructure plan. The deck is dense; the appendix is deep. The eight-page format keeps the deck cognitively manageable for the hour-long committee meeting; the appendix gives the diligence partners somewhere to go in the weeks of work that follow a positive committee vote.

What if our fund is a pure-impact fund or a pure-returns fund and not blended?

The eight-page format is calibrated for blended-return committees, but the structural principles transfer with adjustment. A pure-impact fund (a philanthropic foundation, a development finance institution making grant-equivalent investments) cares about the impact thesis and the measurement methodology above the commercial model. The eight pages stay, but the commercial model page is replaced with a sustainability page — the long-term operating viability of the company without continued philanthropic capital. A pure-returns fund (a mainstream venture fund with no impact mandate) does not need the integration work on every page, and the eight-page format can be compressed back to a more standard six- or seven-slide pitch with the impact dimension carried more lightly. The blended-return architecture matters specifically when the committee is structurally mixed; for either pure case, the standard sector-specific pitch format is the right starting point.

How long should the investment committee meeting itself be planned for?

Sixty minutes is the typical schedule, with twenty to twenty-five minutes for the founder’s deck walk and the remaining time for committee questions. The deck walk should aim to land at minute twenty-two so there are twenty-five to thirty-five minutes for committee discussion. The discipline is to walk the deck at three minutes per page on the headline, problem, and solution pages, two and a half minutes per page on the impact thesis and commercial model pages (the depth pages), two minutes on the team and risks pages, and one minute on the named ask. The named ask deserves the shortest time because the committee can read it instantly; the page exists to give the meeting a clean closing point and to give the chief executive a structured way to ask the committee what the next step is.

How is this different from a B-Corp pitch or a social-enterprise pitch?

B-Corp certification is a corporate-form classification, not a fundraising structure. A B-Corp company raising from a pure-venture fund pitches as a standard venture pitch with B-Corp status noted in the team or company-context section. A B-Corp company raising from a blended-return fund uses the eight-page format with the B-Corp certification referenced in the impact-thesis page as a supporting credibility signal. Social-enterprise pitches typically address either a pure-impact funder (where the philanthropic-pitch structure applies) or a blended-return funder (where the eight-page format applies). What this format adds beyond the standard sector frameworks is the structural integration discipline — the requirement that every page argue both sides of the blended-return equation rather than leaving the integration work to the committee’s post-meeting conversation. The corporate form (B-Corp, social enterprise, conventional company) is a separate question from the deck structure; the deck structure depends on the audience’s mandate.

What is the right financial return target to put on the headline page?

The right target is whatever the fund’s own mandate names — blended-return funds publish their target return range in their fund prospectus and the founder should pitch within that range rather than against it. A fund targeting eight to ten percent net IRR will not invest in a deal pitched at sixteen percent (it sounds aggressive and triggers diligence on whether the impact thesis is being sacrificed for return), and a fund targeting fifteen to eighteen percent will not invest in a deal pitched at six percent (it sounds insufficient and triggers diligence on whether the founder understands the asset class). The pitch’s job is to argue that the company can deliver inside the fund’s stated range; the discipline is to know the fund’s range before writing the headline page. The standard pre-pitch homework is to read the fund’s most recent annual impact report and most recent fundraising prospectus, both of which name the target return range explicitly.

The Winning Edge — weekly newsletter

The Winning Edge is a weekly (Thursday) newsletter for senior professionals who present at the executive level. One short email a week, focused on the structural moves that separate pitches investment committees back from pitches they defer. Subscribe to The Winning Edge →

For the broader picture across slides, storytelling, confidence, and delivery, the Complete Presenter bundle is the seven-product set most senior founders find useful as a single library — £99 for everything, lifetime access.

About the author

Mary Beth Hazeldine is Owner & Managing Director of Winning Presentations Ltd. With 24 years of corporate banking experience at JPMorgan Chase, PwC, Royal Bank of Scotland, and Commerzbank, she advises executives across financial services, healthcare, technology, and government on structuring presentations for high-stakes funding rounds, board approvals, and strategic decisions.